Comparative Advantage. A country has a comparative advantage if it can produce a good at a lower opportunity cost than another country. A lower opportunity cost means it has to forego less of other goods in order to produce it.

Example of Output of two goods

Textiles | Books | |

UK | 1 | 4 |

India | 2 | 3 |

Total | 3 | 7 |

- In this example two countries, UK and India produce textiles and books

- For the UK to produce 1 unit of textiles, it has an opportunity cost of 4 books.

- For India to produce 1 unit of textiles it has an opportunity cost of 1.5 books

- Therefore India has a comparative advantage in producing textiles because it has a lower opportunity cost in textiles.

Opportunity cost of producing books

- If the UK produces a book, the opportunity cost is 1/4 (0.25)

- If India produces a book, the opportunity cost is 2/3 (0.66)

- Therefore the UK has a comparative advantage in producing books (because it has a lower opportunity cost of (0.25 compared to India’s 0.66)

The theory of comparative advantage

- If each country now specializes in one producing good then assuming constant returns to scale, the output will double.

Output after specialisation

Textiles | Books | |

UK | 0 | 8 |

India | 4 | 0 |

TOTAL | 4 | 8 |

- Therefore the output of both goods has increased illustrating the gains from comparative advantage.

- The total output is now 4(T) and 8(B), which is higher than the previous totals of 3(T) and 7(B).

- Therefore, specialising in the good where there is a comparative advantage has led to an increase in economic welfare.

Difference between absolute advantage and comparative advantage

- Absolute advantage means an economy can produce more of a good in the same time period. It means they can produce at a lower absolute cost.

- It is possible for a country to have an absolute advantage in all goods.

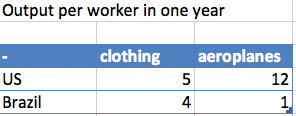

In this example, the US has an absolute advantage in producing clothing (5>4) and also aeroplanes. (12>1) Brazil does not have an absolute advantage in anything. However, that doesn’t mean the US should be the only producer. We should look at comparative advantage.

In the above example, the US has a comparative advantage in producing aeroplanes

- If the US produces clothing, the opportunity cost is 12/5 = 2.4 aeroplanes foregone.

- If Brazil produces clothing, the opportunity cost is 1/5 = 0.25 aeroplanes foregone.

- Therefore, Brazil should specialise in producing clothing (even though it doesn’t have an absolute advantage)

- The US should specialise in producing aeroplanes.

Other issues about trade

- Economies of scale. In the real world, other issues may come into play. If India specialises in textiles, there may be economies of scale, which enable even bigger output.

- Costs of trade. The costs of trade can diminish the benefits of comparative advantage. For countries like Iceland or land-locked countries in Sub-Saharan Africa, this transport costs could be quite significant. There will be some costs of trade. But containerisation has helped reduce the cost of trade.

- New trade theory. New trade theory states that in the real world, comparative advantage is less important than the economies of scale from specialisation.

- Gravity theory. This is another theory of trade which states countries gravitate towards trading with similar countries with close geographical proximity. For example, European countries are more likely to trade with similar European countries because of lower transport costs – but also similar cultural backgrounds

- Competition. Free trade can also increase competitive pressures which also help to reduce monopoly power and reduce prices for consumers.

- Examples. There are many examples of comparative advantage in the real world e.g. Saudi Arabia and Oil, New Zealand and butter, USA and Soya beans, Japan and cars e.t.c

Limitation of the theory of comparative advantage

- Transport costs may outweigh any comparative advantage

- Increased specialisation may lead to diseconomies of scale

- Governments may restrict trade

- Comparative advantage measures static advantage but not any dynamic advantage for example in the future India could become good at producing books if it made the necessary investment

Related pages