In September, the Pound plunged to its lowest level on record reaching a low of 1.03 during a day’s trading. The markets were spooked by the government’s unfunded tax cuts and likely £190 bn budget deficit. Investors viewed the Kwarteng/Truss budget as the shortest suicide note in history. Investors sold Sterling and UK bonds, creating a mini-crisis. Fortunately, intervention from the Bank of England, U-turns from the government and a new Prime Minister have calmed Sterling, but is the crisis over? Is Sterling now undervalued or will its long-steady decline of recent decades continue?

Is The Sterling Crisis Over? Or is the Pound Set to Continue to Slide?

Recession risk

Recently the Bank increased interest rates by 0.75% – which should in theory strengthen the Pound. However, the Bank also hinted that because of the depth of the recession interest rates may rise less than market expectations. The Bank feel interest rates could peak lower than US and Eurozone. This is because the bank is worried about recession – for good reason.

The UK economy is being hit by a combination of

Higher inflation – over 10%

Falling real wages

Rising mortgage costs

Fiscal austerity of government

Collapse in consumer confidence

Therefore, the Bank don’t want to add to the depth of the recession. This means interest rates could rise less than expected. What the bank are hinting at is that they would prefer to see a fall in the Pound than create a deeper recession.

By contrast the Fed were more hawkish arguing underlying inflation in US still problem – because US economy has had more stimulus than say UK or European economies. This still points to dollar strength over the Pound.

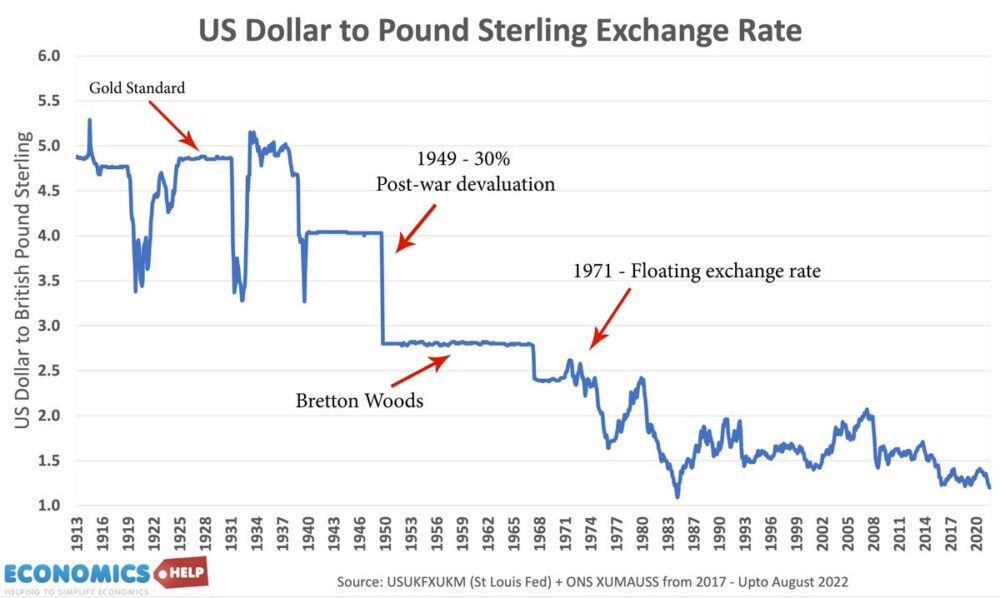

Past 100 years of US dollar to Pound Sterling

If we look at the value of the Pound since 1913, we can see the general downward trend. In fact, the average is a 1% decline per year. Before 1971, the value was often fixed. But, since 1971, we have had a floating exchange rate.

It is not just weakness against the dollar. This graph shows the dismal performances of Sterling against a basket of currencies in the past 15 years. The Sterling exchange rate shows Sterling against a basket of currencies.

The 30% fall in 2009 was due to the UK’s economy’s reliance on financial services which were hit by the credit crunch.

The 2016 Brexit vote also hit expectations of the UK economy because of the all costs associated with leaving the single market and customs union – and this is reflected in recent poor export volumes and decline in foreign investment. Ongoing issues around Brexit weaken the Sterling in the long-term because it makes the UK less attractive for capital flows and is damaging some export volumes.

Current account deficit

Another weakness for Sterling is the size of the current account deficit. It doesn’t get much headlines these days, but is important. The current account deficit reached a record 8% of GDP deficit earlier in the year, before recovering a little to 5% deficit. However, this winter, high gas and oil prices will cause a surge in the value of energy imports, causing a bigger deficit and further deterioration in Sterling. For example, the price of gas futures suggests the value of gas imports will rise from £1.8 bn in July to £8 billion by the end of the year,

Another concern is that the current account deficit is despite the fall in Sterling. Because a fall in sterling should in theory make exports cheaper and improve current account. But We are getting fall in Sterling and a large deficit.

When you have a current account deficit it needs financing from capital inflows, e.g. foreign investment people saving in UK banks, but these capital flows are less certain because of global slowdown and uncertainties around Brexit and the performance of the UK economy.

Purchasing Power Parity

A more optimistic note for Sterling can be viewed when looking at long-term purchasing power parity. This looks at the value of an exchange rate compared to the purchasing power. The simplest way to explain this is the Economist’s Big Mac index.

In July 2022 A Big Mac with the same ingredients costs £3.69 in the UK, $5.15 in the United States. A fair exchange rate would be 1.40. The actual exchange rate in July was 1.20 – suggesting that on purchasing power parity, the Pound was 14% undervalued and the dollar overvalued. (It should be said nearly all currencies are undervalued against dollar on purchasing power parity – because of the strength of the dollar.)

Back in the early 2000s, I remember when it was cheaper to buy a Mac computer in the US. Because the Exchange rate was closer to $2 to £1. But, the actual price was around £1,000 or $1,000. So you could save a lot by buying in the US. With an exchange rate like that the Pound is always likely to fall because it makes sense for UK consumers to import US goods. But, now, in theory, it is more the other way. UK goods should be cheaper for US consumers.

However, exchange rates can deviate from purchasing power parity for a long-time. In the medium term, interest rates, expectations of growth and the relative strength of economies. For example, investors may look at the UK productivity growth and since it has been underperforming, the UK is more likely to see inflationary pressure in the long-term than say the US.

Gas prices

Another reason for strength of dollar versus Pound and Euro, is the Euro economy is much more vulnerable to high gas prices. Although prices have fallen in the past month, the crisis is far from over and there is a real risk of escalation with Russia cutting more gas, and attacking pipelines and this would be devastating for Europe and UK. Causing inflation, recession and a fall in the currency. The US is more protected because of its

Buck the trend

Will Sterling buck the trend of the past 100 years? It would be a brave investor who bought Sterling despite the apparent undervaluation on PPP. The Bank of England forecast the longest recession for a generation. In this climate, the bank wants to keep interest rates low. The long-term underperformance of the UK economy all points to weaker sterling.