Readers Question: ‘Outline two reasons why the UK’s housing market represents a barrier to the UK’s membership of the euro’.

Joining the Euro involves a common monetary policy. This means that UK interest rates will be set by the ECB. Therefore, if the ECB has to increase interest rates it will increase UK rates and therefore increase the cost for UK homeowners. If interest rates increase at the wrong time it could cause economic hardship for homeowners.

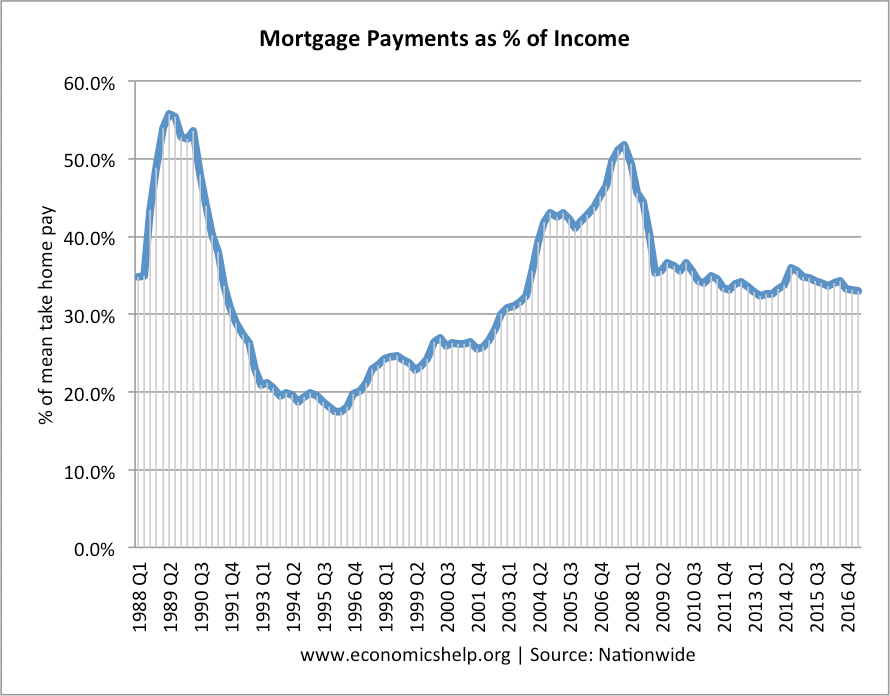

1. Mortgages are a high % of consumer’s disposable income and therefore are sensitive to changes in interest rates. UK House prices are a high ratio of average incomes. Many homeowners have had to take out mortgages 4-5 average incomes to get on the property ladder. This means mortgage payments are a high % of disposable income. If interest rates increase, it could make mortgages unaffordable.

2. Variable Mortgages. In the UK, a high % of mortgages are variable mortgages as opposed to a fixed rate. Therefore, a change in rates has a big effect on homeowners and therefore, the housing market.

Also, the UK has a high % of homeowners compared to the continent where more people rent.

Basically, the UK Housing market is very sensitive to changes in interest rates and would struggle to cope with common monetary policy.

In times of high interest rates mortgage payments as % of disposable income can reach over 50%

Related