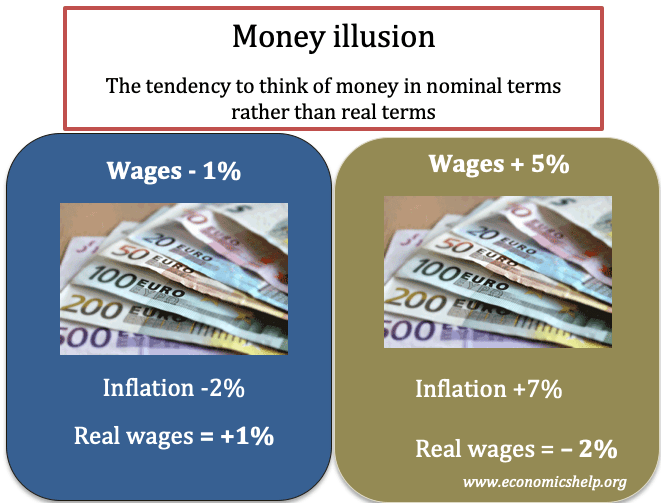

Money illusion is the belief that money has a fixed value and the effects of inflation are ignored. Because of money illusion, during inflation, individuals may perceive an increase in nominal income as higher welfare – when this is actually an illusion and their real spending power has not changed because prices have risen at the same rate as wages.

For example, if workers receive a 5% pay rise, they may feel that this represents an increase in their living standards as their income is higher. However, if inflation is 7% then prices are rising faster than income, the effective purchasing power of a worker is falling (real wages -2%).

If workers receive a 1% pay cut, this is a psychological blow and workers may feel worse off. However, if prices are actually falling by 2%, then in effect, despite this nominal pay cut, their real income has increased by 1%. Despite the nominal wage cut, they can buy more goods and services than before. However, this may not be immediately apparent. At first glance, people may prefer a wage increase of 5% to a wage cut of 1%.

Origin of the term money illusion

The term was created by Irving Fisher who felt that a combination of rising prices and money illusion could seriously destabilise the economy. The concept of money illusion was popularised by John Maynard Keynes.

Reasons for money illusion

Price stickiness. Firms may resist changing prices according to costs because there is a psychological blow to raising prices. Consumers prefer stable prices and when prices rise, it can cause uncertainty and discourage consumption.

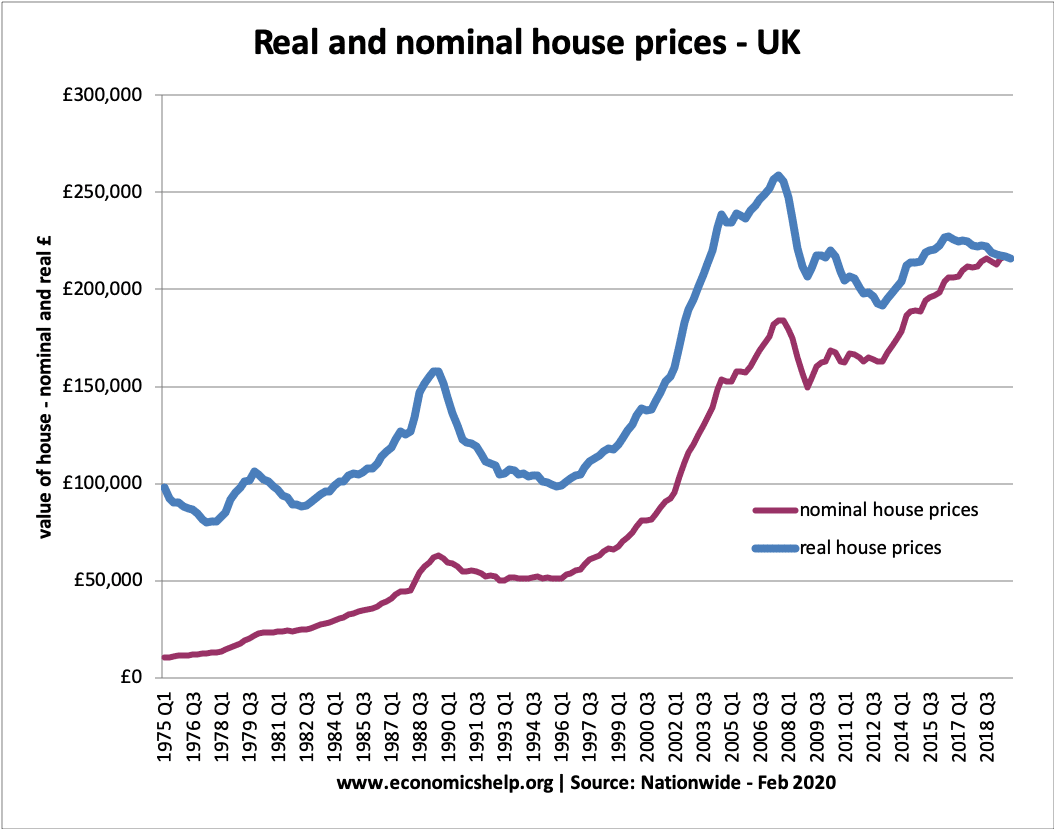

Failure to distinguish between nominal and real values. For example, if a government boasts about spending record levels of money on the health care system, it is not obvious that this might include inflationary effects and represent a smaller real increase. Another example might be the change in house prices. The nominal house price is more easily compared than the inflation-adjusted price.

The change in nominal house prices from 1975, gives a much more startling figure £7,000 to £200,000. The change in real house prices is more muted £100,000 to £220,000

Wage stickiness. Even in a period of deflation (falling prices) workers are likely to resist nominal wage cuts because of the psych0logical cost of seeing a fall in nominal wages. Thus in a period of deflation, we can end up with real wage unemployment – unemployment caused by wages above the equilibrium.

Myopic loss aversion. Behavioural economists have suggested we are more affected by visible losses than invisible losses. For example.

A) If prices rise 4% and wages rise 2%, this is a real wage cut of 2%

B) If prices rise 0% and wages fall 2%, this is a real wage cut of 2%

Despite giving the same outcome, research suggests that people feel A) is fairer than B)

Heuristics. In everyday life, people do not make precise calculations but use rough rules of thumb to save time. Thus viewing money as a constant source of value makes life easier. For this reason, people assume $100 has a constant value and disregard the small effects of inflation.

Missing information. People can easily see their nominal wage, but real wage requires knowledge of price changes and calculation of real values.

Contracts are not closely linked to inflation. Because of the dislike of price changes, contracts often seek to keep prices the same.

Underestimating the rate of inflation. Some countries have sought to reduce the official rate of inflation to give misleading impression of what is happening to prices. For example in 2015, the official rate of inflation in Argentina was given as 15%, but private economists stated it was closer to 28%. If consumers based real spending on official inflation, they would over-estimate their spending power.

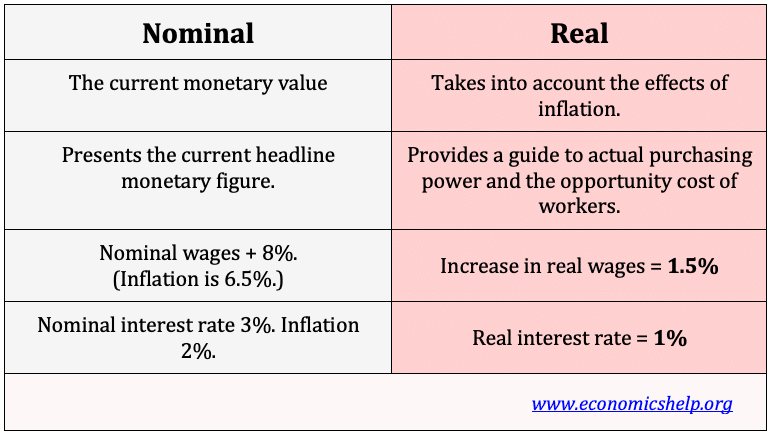

Real and nominal terms

To understand money illusion it is necessary to see difference between nominal and real.

Money illusion and adaptive expectations

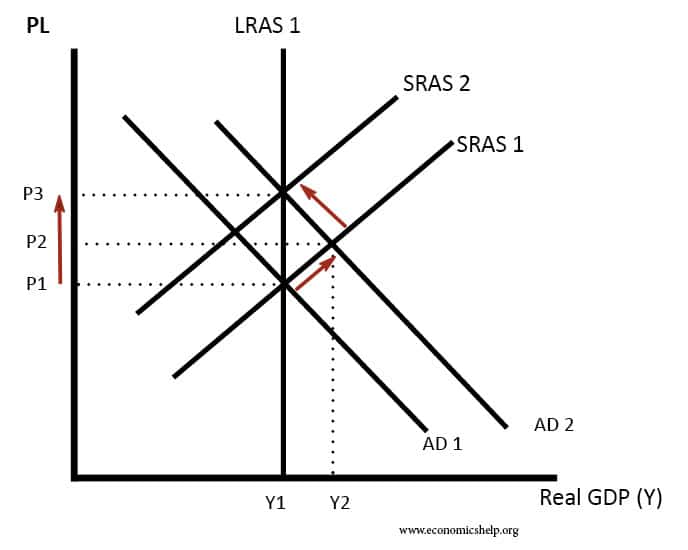

Monetarist economists, such as Milton Friedman argue that money illusion tends to only occur in the short-run, where there is a time lag before consumers realise prices have increased.

Because money illusion exists in the short-run, an increase in the money supply can cause a temporary increase in real output. People respond to the increased money supply by spending more causing a rise in aggregate demand. The rise in the money supply also causes an increase in nominal wages – so workers agree to supply more labour and there is an increase along the short-run aggregate supply. However, over time, workers realise that the increase in wages was only a nominal increase – because prices have risen. Therefore, in the long-term, workers cut back on overtime and output returns to the same real output.

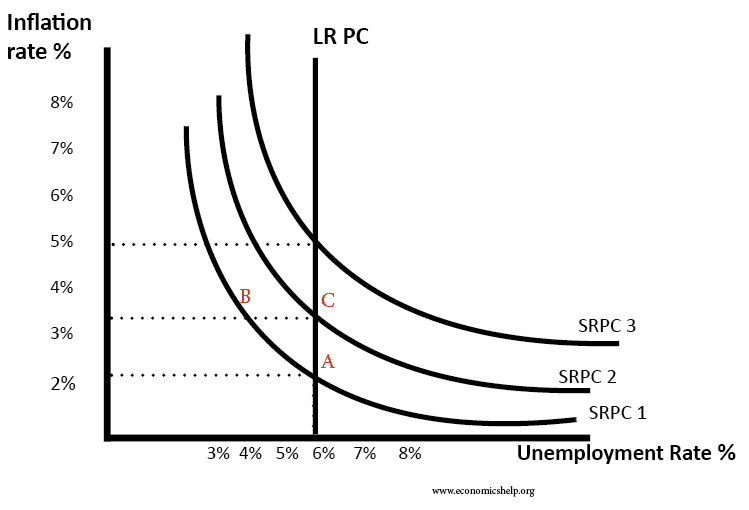

Monetarist Phillips curve

Because of this money illusion an increase in the money supply can cause a short-term fall in unemployment

But, in the long-run, unemployment remains at the natural rate.

Rational expectations and no money illusion

Some economists dismiss the idea of money illusion. They argue that although individuals may be wrong some of the time. In aggregate they are correct on average over time. Thus, if there was an increase in the money supply, it is not the case that workers will be fooled into thinking nominal increases are real increases. Rational expectations suggest workers have a better knowledge of prices than some economists give credit. Rational expectations was promoted by John F. Muth (1961) and popularised by Robert Lucas.