Could UK Economy Make An Unexpectedly Strong Recovery?

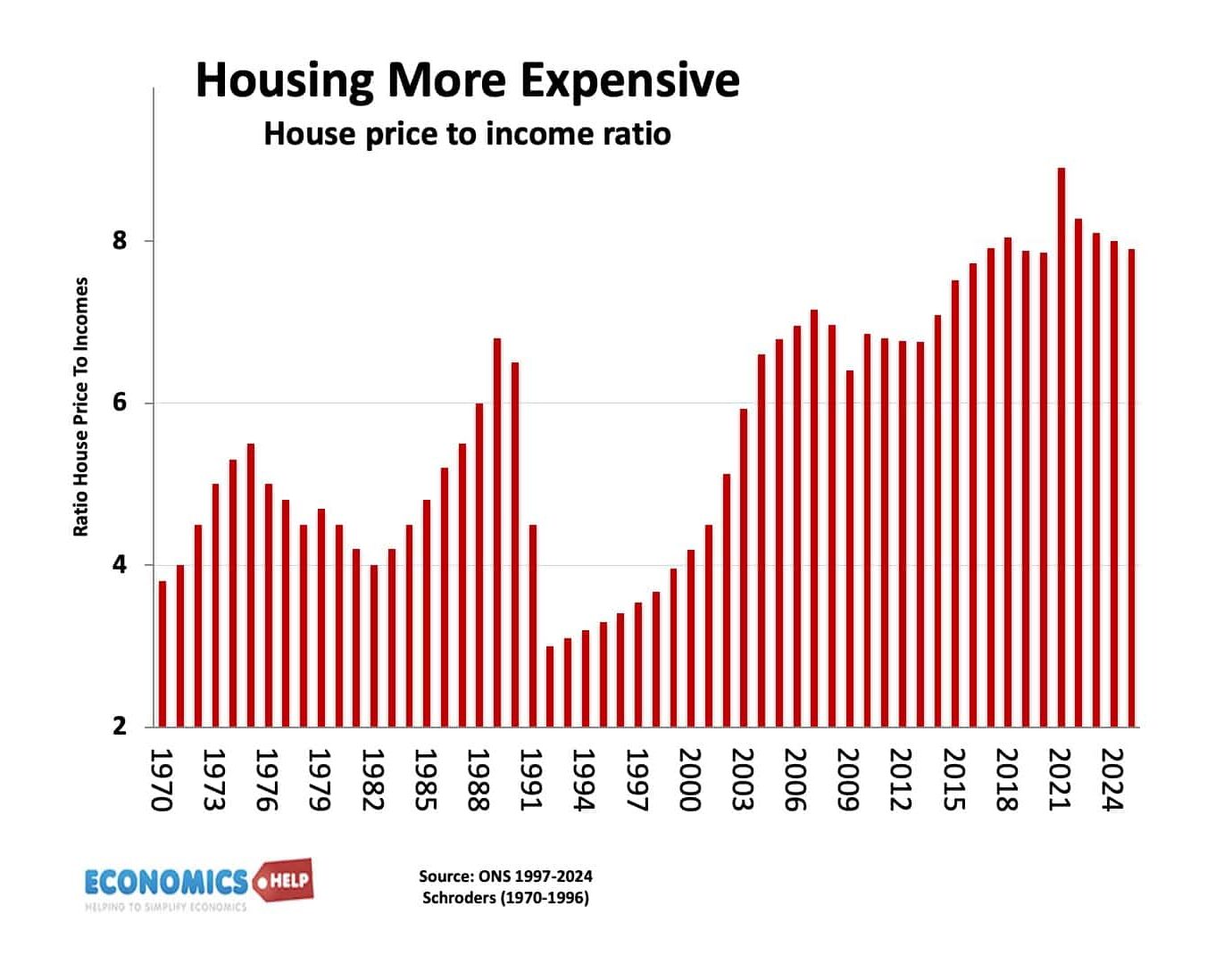

People often observe my videos/articles on the UK economy tend to be doom and gloom, this is partly the youtube alogorithm, but mainly because the UK economy really hasn’t been doing very well, whether you look at average wages, productivity or housing costs, it’s pretty grim and you can’t change these facts. And there is …