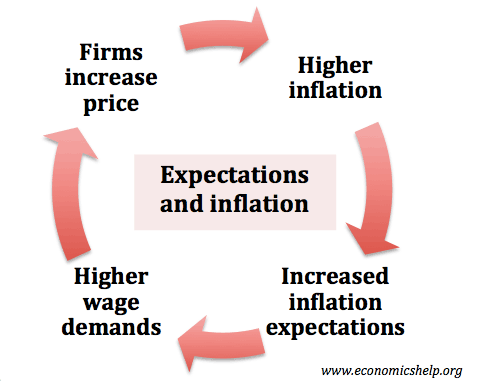

A key factor in determining inflation is people’s expectations of future inflation.

If firms and consumers expect future inflation then it can become a self-fulfilling prophecy. If workers expect future inflation, they are more likely to bargain for higher wages to compensate for the increased cost of living. If workers can successfully bargain for higher wages, this will contribute towards inflation. Higher wages:

- increase cost-push inflation (wages increase firms costs)

- increase demand-pull inflation (workers have more disposable income)

Also, if firms are expecting inflation to rise (e.g. expecting the price of raw materials to increase) then they will be more likely to increase prices to protect their profit margins.

Central Bank and Reducing Inflation Expectations

One reason why Central Banks have been given control over monetary policy and inflation targeting is that it is hoped an independent Central Bank will have a strong reputation for keeping inflation low. When politicians used to set interest rates, there was the feeling that they may sacrifice low inflation to cut interest rates before a general election. But, a Central Bank doesn’t face these political pressures and so can be strict in keeping inflation low. If people feel the Central Bank will keep inflation on target, then it becomes much easier to achieve this target. Workers and firms will make decisions around a 2% inflation target.

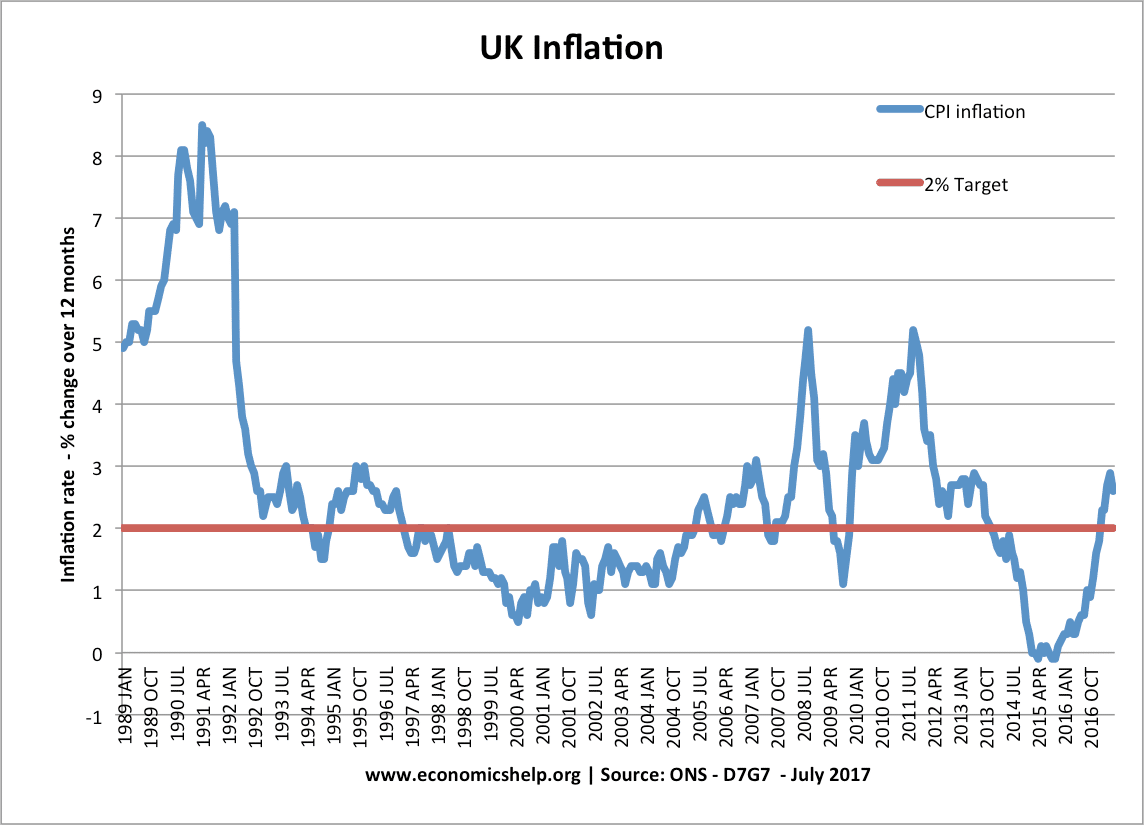

In 1997, the Bank of England was given independence to set monetary policy. Since then inflation has generally been lower than previous decades of the 1970s and 1980s.

What Influences Inflation Expectations?

- Current Inflation Rates. The current inflation rate is the biggest guide to expectations of the future.

- Past inflation trends, e.g. a country with a history of inflation is likely to make people more pessimistic.

- General economic outlook. e.g. prospects for growth and unemployment. However, it’s not entirely clear people make the same links economists might. For example, if there is the prospect of a recession and unemployment, we would expect inflation to be lower. However, some people may just equate recession with bad news like prices going up. (e.g. in current recession of 2011, that is exactly what seems to have happened, lower incomes and higher prices)

- Wage growth

- Monetary policy credibility. If people feel the government is willing to expand the economy and risk inflation, then they may start to expect more inflation. If people believe Central Bank will be unyielding in keeping inflation low, then there will be low expectations and it will be easier to keep inflation low.

Role of inflation expectations in Monetarist Adaptive expectations

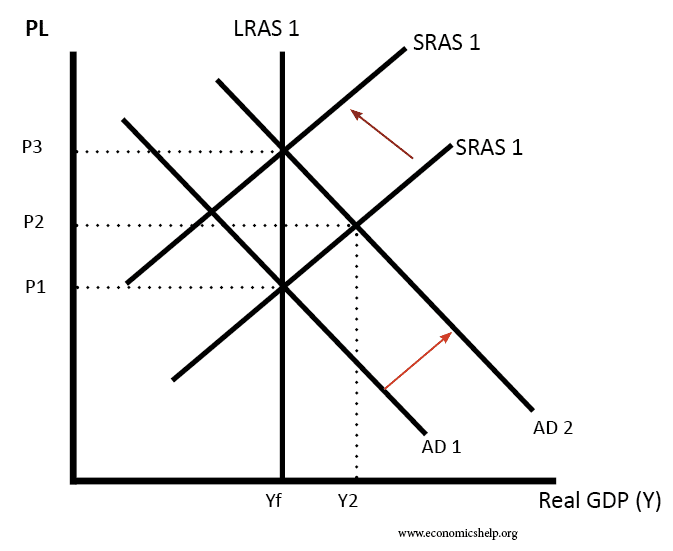

Milton Friedman argued that if the government/Central Bank increase aggregate demand and inflation, then there will be only a temporary fall in unemployment. Importantly, people will respond to higher inflation by expecting higher inflation in the future. Therefore,

- Suppose people expect inflation to be 0%.

- Then assume there is an increase in Aggregated Demand (AD) and the Money supply. This leads to an increase in nominal wages of say 2%.

- Because people expect inflation to be 0%, they feel that real wages (w/p) have increased by 2%.

- Therefore, with an increase in real wages, people are willing to work longer hours (substitution effect of higher wages). Because people work longer hours firms can increase production. Therefore, there is a movement along the SRAS (short-run aggregate Supply). This leads to an increase in real output but also causes inflation.

- Later, workers realise that their inflation expectations of 0% were wrong. Because inflation has increased by 2%, their real wage has stayed constant. Therefore, they stop working overtime, the SRAS shifts to the left to readjust to the new inflation expectation of 2%.

- Therefore, in the long run, the Aggregate Supply stays the same (inelastic).

- In the classical model, the Long Run Aggregate Supply is inelastic. Increase in the money supply only causes a nominal increase in GDP.

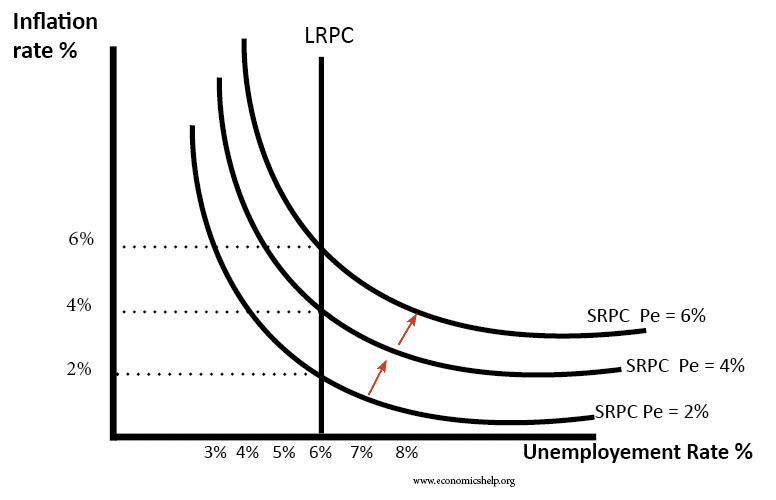

This view of aggregate supply and aggregate demand causes a Phillips Curve like this

When people expect inflation of 2%, the economy is at a natural rate of unemployment NAIRU (6%) with inflation of 2%.

If there is an increase in AD, then whilst expectations are stuck at 2%, there is a temporary fall in unemployment to 4%, but after workers realise inflation has increased, the SRAS shifts to the left, and we return to the non-accelerating rate of unemployment (NAIRU) 6% but at the higher rate of inflation of 4%

The classical model assumes that labour markets are efficient and competitive.

The Keynesian view is different. They argue that Labour markets can be inefficient and in a state of disequilibrium. For example trades unions can cause wages to be above the equilibrium. Therefore, they argue the long run aggregate supply function may not be perfectly inelastic. Often they can be spare capacity in the economy, due to underutilized resources – especially in a recession. Therefore, if there is an increase in aggregate demand it can cause an increase in real output.

Rational expectations

In the rational expectations model, people are better at predicting inflation. If they see expansionary fiscal/monetary policy, they change expectations of inflation and don’t get tricked by outdated expectations of inflation.

Temporary Inflation and Inflation Expectations

An interesting issue is whether temporary cost push inflation influences long-term inflation and inflation expectations. For example, in 2011, the UK saw a rise in CPI inflation to 5.2%. This was due to temporary cost push factors like

- Effects of devaluation increasing import prices

- Tax Increases

- Rising Commodity prices

Yet, despite inflation well above target, the Bank of England decided not to increase interest rates because of concerns over a fall in economic growth and unemployment.

Leaving interest rates unchanged and accepting an inflation rate of 5% may undermine people’s confidence in the Bank’s commitment to low inflation. It could translate into higher inflation expectations. It depends on how long inflation remains above target.

However, in practice, inflation fell sharply. Wage growth was weak so there was no long-run change in inflation expectations.

Related

thank you for your deeply explanation of inflation expectation, very useful for me to understand macroeconomy.