Costs of production relate to the different expenses that a firm faces in producing a good or service.

Types of costs

- Fixed costs – costs that don’t vary with output

- Sunk costs – costs that cannot be recovered on leaving industry, e.g. advertising

- Variable costs – costs relating to how much is produced (e.g. raw materials

- Semi-variable costs – costs like labour which to some extent depend on output.

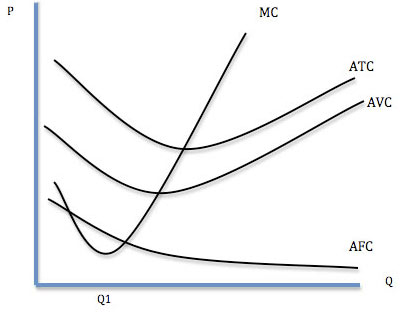

- Marginal Cost: This is the cost of producing an extra unit.

- Short-run costs (subject to diminishing returns)

- Long-run costs (potential economies and diseconomies of scale.

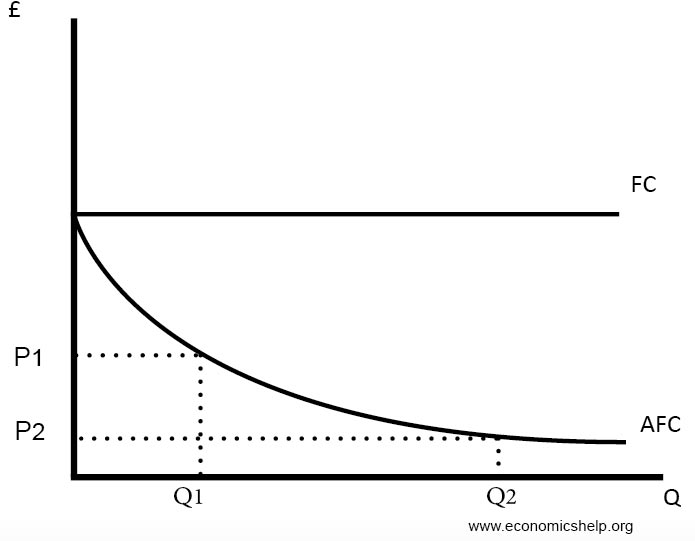

Fixed Costs FC

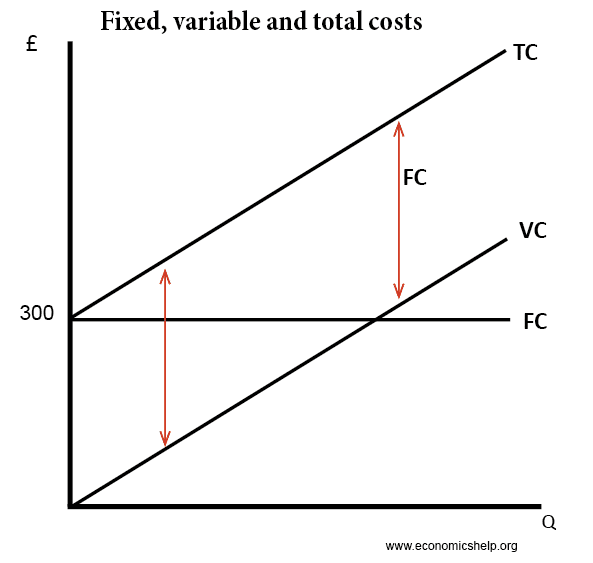

These are costs that do not vary with output. However many goods are produced, fixed costs will remain constant. For example, if a new factory costs £1 million, this cost is unaffected by the number of goods produced.

Average fixed costs (AFC) = FC/Q. As more goods are produced, the average costs will fall.

Variable Costs

These are costs that do vary with output. As output increases, there will be more variable costs. For example, as you produce more cars, you will have to pay for more raw materials, such as metal, tyres and plastic.

Average variable costs (AVC) = VC/Q

Semi-Variable costs

Some costs may exhibit both fixed and variable factors. For example, a firm may continue to employ workers, even during a slump in production. But, as output increases, they may take on more workers or pay overtime.

Short Run Costs

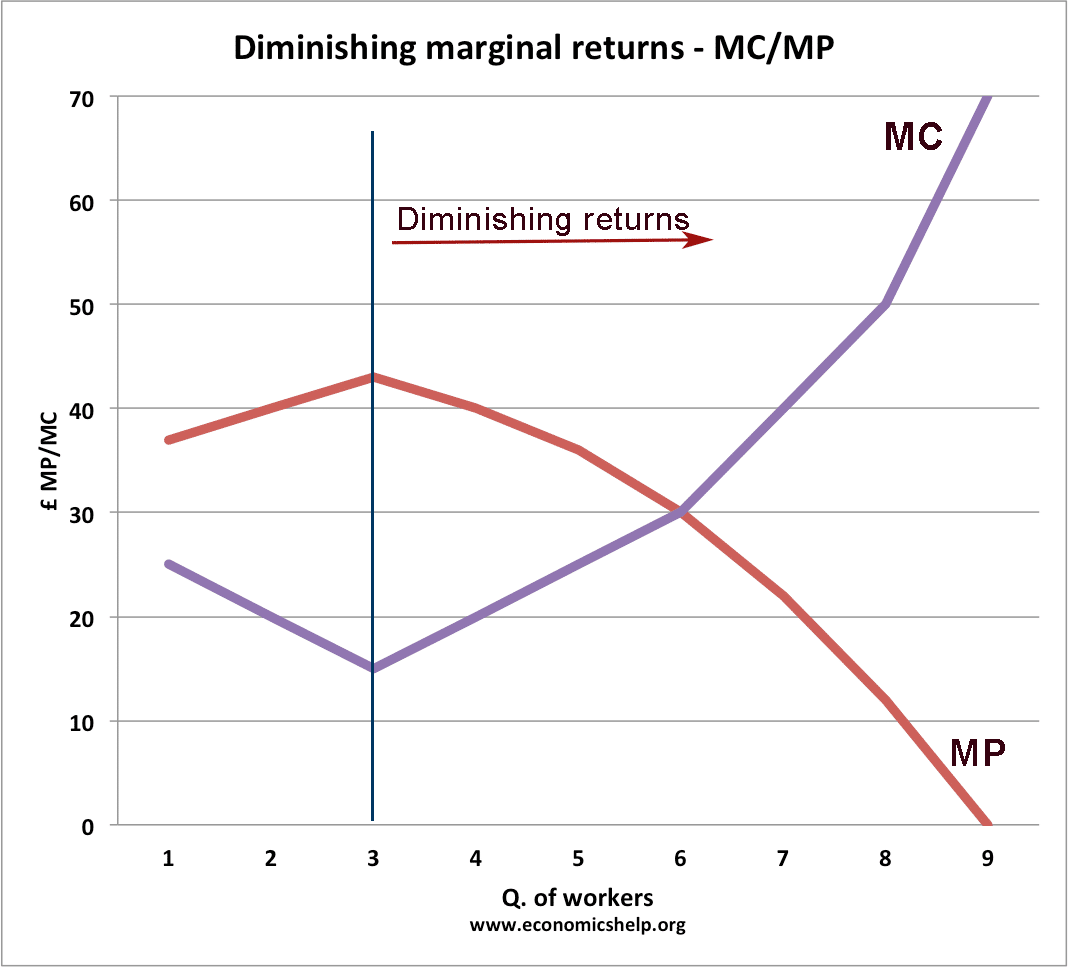

Diminishing Returns in the short run

As productivity (and marginal product) falls, the marginal cost of production will increase.

See: Diminishing returns to scale

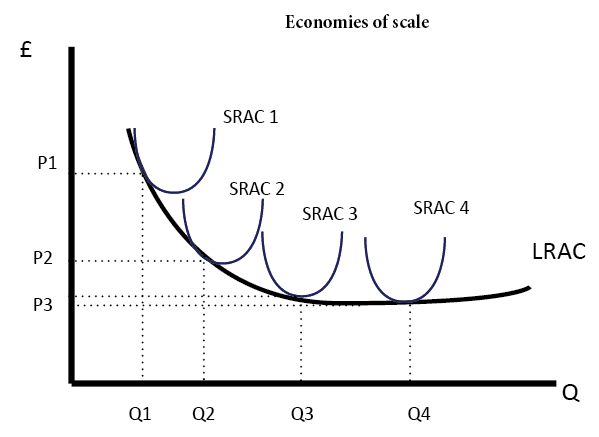

Long Run Costs

In the long run, a firm can vary all factors of production, such as capital and labour. Therefore, the firm will not face diminishing returns. However, as the amount of capital can vary, the firm may experience economies or diseconomies of scale.

- Economies of scale occur when increased output, leads to lower long-run average costs

- Diseconomies of scale occur when increased output leads to higher long-run average costs.

Factors affecting costs of production

- Wage costs. For labour intensive industry (service sector/manufacturing of clothes) a small change in wage costs has a big impact on the overall costs of firms.

- Labour productivity. New technology which improves output per worker enables the firm to cut back on employing workers, leading to lower costs.

- Exchange rate. A rise in the exchange rate makes imports cheaper. If the firm needs to import raw materials, an appreciation can reduce the cost of production (though exports will be less competitive)

- Raw materials. A rise in the cost of raw materials, e.g. oil, plastic, and metal – will increase the cost of firms. Nearly all firms will be affected by higher oil prices – which increase the cost of transport.

- Tax. Higher national insurance (tax on workers) raises costs.

- Bureaucracy and administration. Firms which have to fill in paperwork and complicated tax returns will have higher costs. This could be significant for firms who export but have to pass through administrative hurdles (non-tariff barriers)

- Transport costs

- Interest rates. FIrms who borrowed to invest will be affected by an increase in interest rates – which raises the cost of loan repayments.

Related

Thank You!!!

This was indeed helpful

yeah, it was really helpful to me .thank you

Lovely, I appreciate your good work. Nice piece

Thanks alot

Appreciated it

Increase in electricity cost not mentioned. It is a MAJOR INCREASE in the cost of production. China burns coal. We do not.

Electricity is under fixed cost it can affect the volume/quantity of production hence it can be mention/calculated under total cost in order to know your average cost accurately before fixing price…

This is very comprehensive & exquisite!

Thumbs up to the writer👍👍

Production coct

Good

How can I cite this piece

It’s very impressive

Thanks you so much

Thank you so much