Tax competition occurs when different countries seek to attract investment and multi-national companies, by offering lower tax rates. Usually tax competition refers to corporation tax, but can also include competition on income tax on labour.

Tax competition has become more important in recent decades as multi-national companies find it easier to locate in different countries. Countries face an incentive to reduce tax rates because it can lead to more investment, more jobs, and higher tax revenue. However, critics of tax competition argue that the competition is unhealthy and leads to lower overall global economic welfare.

Problems of tax competition

- Encourages a beggar thy neighbour policy. If a country cuts corporation tax to attract investment, it means other countries who don’t cut taxes lose out.

- There is no net gain, only some countries benefit at the expense of others.

- If countries retaliate to the initial tax cut by also cutting tax rates, then the increase in investment will prove temporary. For example, suppose Ireland cut corporation tax from 20% to 10% – initially multinationals will respond by investing in Ireland. However, if other European countries respond by also cutting tax rates to 10%, then Ireland will not lose this initial greater investment, but all countries will have lower corporation tax rates.

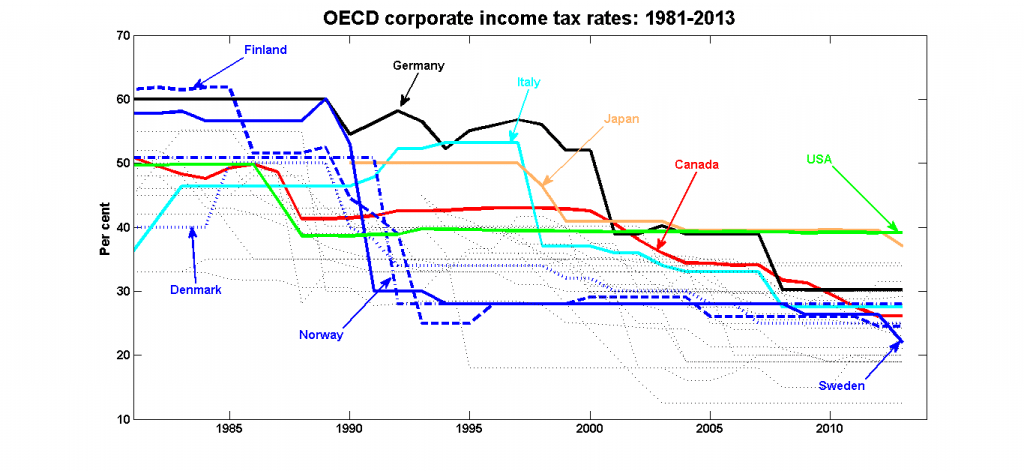

- If corporation tax rates are cut in a form of tax competition, then other taxes, such as income tax and VAT will have to increase to meet the shortfall. This could represent an increase in inequality and means countries lose the right to choose how to distribute the tax burden in their economy. (Note: the average corporate tax rate for OECD members has declined from 37.6 per cent in 1996 to 28.3 per cent in 2006, according to KPMG)

How corporation tax rates have fallen in past few decades.

Tax competition is not a real increase in competitiveness. When a government cuts corporation tax, there is no actual increase in labour productivity or increased efficiency of using resources, it only means firms get to keep a higher percentage of their profits. Countries which attract investment through low tax rates may have less incentive to encourage other forms of competitiveness, such as higher labour productivity. If we look at competitiveness, high tax countries can still make it into the top 10 list of most competitive countries (http://www.weforum.org/issues/global-competitiveness)

Benefits of tax competition

- Supporters argue that lower corporation tax rates are beneficial for encouraging investment. Lower corporation tax gives firms more profit that can be used to spend on research and development and investment.

- Tax competition provides incentives for governments to cut wasteful spending and increase the efficiency of spending.

Related