‘Beggar my neighbour’ is a term used to describe an economic policy, where you seek to gain an economic advantage by making other countries lose out. Cutting corporation tax is an effort to take away investment from countries with higher corporation tax. It creates an incentive for countries to keep cutting to see who has the lowest tax rate.

Currency and beggar my neighbour

For example, in a depression, a country may seek to devalue their currency to increase exports and domestic demand. However, if one country artificially keeps a currency undervalued – it means other countries suffer from being relatively over-valued and lower domestic demand. It was a charge often levelled at China – claiming currency manipulation gave Chinese exports a benefit over other countries.

See also: beggar my neighbour

Corporation tax and beggar my neighbour

In a globalised world, there is a temptation for a country to cut corporation tax rates below the global average to attract more inward investment. The country cutting corporation tax benefits from more investment, and although tax rates are lower, they hope to make up tax revenue by attracting more firms.

However, if one country cuts corporation tax, you effectively are attracting firms away from other countries, who lose out. Cutting corporation tax in the UK, doesn’t increase global economic welfare – it tries to increases UK economic welfare at the expense of other countries.

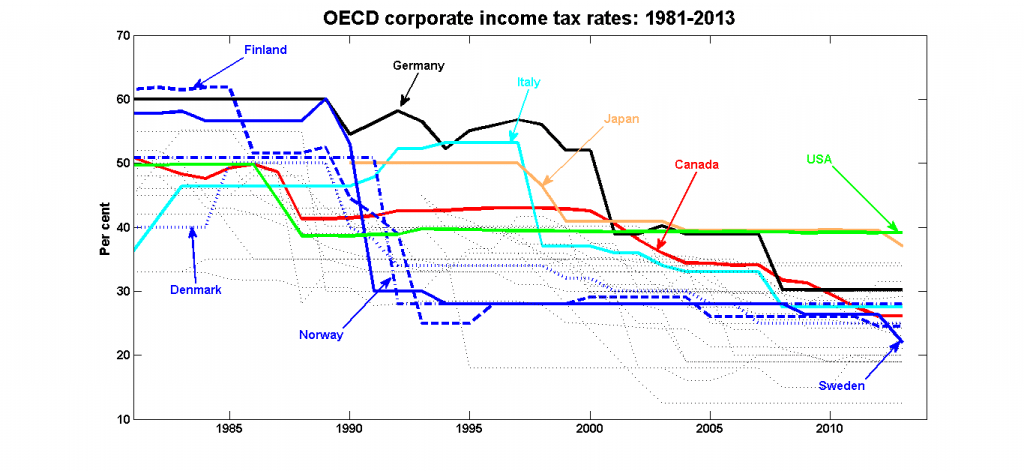

International Corporation tax rates

Note Ireland has corporation tax rate of 12.5% on trading income and 25% for non-trading income. US corporation tax rate is misleading because there are so many loopholes, which enable a lower actual rate.

Consequence of beggar my neighbour

The other problem is that if the UK were to cut corporation tax to below EU average, the EU countries may think – we need to cut corporation tax too to prevent this ‘unfair tax competition’ attracting inward investment away from our economies.

There has been a general decline in corporation tax rates as countries try to stay competitive.

This can create a situation of tax competition – where countries keep cutting tax rates to attract investment. But, the total level of investment doesn’t increase, it is just competition for a certain level of investment.

In theory, strong tax competition could lead to very low corporation tax rates – and a situation where no one has gained any more investment. The only real winners are companies who benefit from lower global corporation tax rates.

Also, this will increase inequality, with companies benefiting from low tax, and ordinary workers having to pay relatively higher tax to compensate.

International co-operation to avoid beggar my neighbour.

There would be a very good case for global co-operation to try and avoid this kind of ‘beggar my neighbour’ tax competition. It is unfortunate the EU didn’t manage to harmonise EU corporation tax rates and prevent Ireland undercutting European rivals with very low corporation tax rates. I’m against harmonisation of monetary policy (EU single currency) and income tax rates, but corporation tax by nature of global investment does lend itself to international competition.

UK decision to cut corporation tax rates

Worried by loss of inward investment because of leaving Single Market, the UK chancellor has suggested cutting the rate of corporation tax to less than 15% to attract more firms to the UK.

From a selfish point of view, there is a logic to this. Compensate firms for loss of Single Market by offering lower tax rates. The UK can’t afford to see a big exodus of global multinationals. A cut in corporation tax could be the incentive they need to stay in. But, there are drawbacks to this policy.

Problems of cutting corporation tax rates

- For a chancellor who promised to balance the budget at the last election, and threatened tax rises before the EU referendum, he seems to have given up on previous fiscal targets and now is seeking to cut tax rates, just as the budget situation is likely to deteriorate.

- Lower corporation tax is likely to mean higher taxes on income and expenditure to compensate for decline in corporation tax rates. It will represent another shift in income from working people to multinational companies, exacerbating previous trends in inequality.

- Some argue cutting tax rates can lead to higher overall revenue because you attract more investment, but investment demand may be quite inelastic to tax cuts – especially if others follow suit.

- Beggar my neighbour policy. This cut in corporation tax is a classic beggar my neighbour policy. After leaving the EU, the UK would do well to portray itself as a country interested in global and European co-operation – seeking to have the lowest corporation tax gives the completely opposite impression – that the UK is only interested in narrow self-interest and isn’t concerned about the wider implications and it how it may adversely affect other countries.

- EU may well retaliate. If the UK cuts corporation tax, the EU is likely to retaliate; either member countries will also cut corporation tax or the UK will have to pay a higher cost for accessing EU single Market as a consequence. It’s not a great bargaining chip to go into negotiations.

- Lower corporation taxes have been a possible reason for the rise in cash reserves of major companies. This saved money is unused and can be viewed as a welfare loss because it is not been used in a more profitable way. According to FT, the net cash position of FTSE 100 companies has risen from £12.2bn in 2008 to £73.9bn this year in 2013. See: Cash reserves of major companies

Personal view

I was really dissappointed to hear this, but perhaps not surprise from a chancellor who is adept at putting his political future above wider national interests.

I don’t want the UK to become some kind of selfish, inward looking, tax haven. The chancellor would be better off addressing underlying factors of business investment – better infrastructure – new airport, better roads and transport – that business repeatedly say the UK needs, rather than this corporation tax cut which will only really benefit multinational companies.

Whether in the EU or not, the UK needs to think in terms of European co-operation and not just how we can maximise our self-interest at the expense of others.

Related

good artical

We must not forget the other side of the coin. For with every cut in corporation tax worldwide, private companies will retain more of their profits. They may then spend the extra funds how they wish, in dividends to their investors, or further investment in their company, leading to further economic growth.

Surely you don’t consider that government is as efficient at spending money on infrastructure as private companies are at spending the extra profits they will get to keep from the tax cut.

We must strive to cut taxes, everywhere and at every opportunity.

It is a mistake to feel greater profit by firms will all be usefully invested in society. Just look at the cash piles of companies like Google and Apple. Apple will never invest in public goods like transport and infrastructure.

yes, agreed!

Funny how it’s a ‘personal note’ just at the end when the entire article is a biased commentary to cut corporation tax. A shame, this could have been actually full of knowledge and not opinion.

That’s was a wonderful informative post you share on this page for removing of neighbour cutting corporation tax by writing an authentic application with the required original documents of big neighbour taxpayer return after reading and understanding all the most important key points are mentioned in the above passage of information especially ”current tax reform” which is very helpful for you to find the solution of a problem and solve it in a very short interval of a time .

Thanks.

Nice information post . Thank you very much.