Definition: Scarcity refers to resources being finite and limited. Scarcity means we have to decide how and what to produce from these limited resources. It means there is a constant opportunity cost involved in making economic decisions. Scarcity is one of the fundamental issues in economics.

Examples of scarcity

- Land – a shortage of fertile land for populations to grow food. For example, the desertification of the Sahara is causing a decline in land useful for farming in Sub-Saharan African countries.

- Water scarcity – Global warming and changing weather, has caused some parts of the world to become drier and rivers to dry up. This has led to a shortage of drinking water for both humans and animals.

- Labour shortages. In the post-war period, the UK experienced labour shortages – insufficient workers to fill jobs, such as bus drivers. In more recent years, shortages have been focused on particular skilled areas, such as nursing, doctors and engineers

- Health care shortages. In any health care system, there are limits on the available supply of doctors and hospital beds. This causes waiting lists for certain operations.

- Seasonal shortages. If there is a surge in demand for a popular Christmas present, it can cause temporary shortages as demand as greater than supply and it takes time to provide.

- Fixed supply of roads. Many city centres experience congestion – there is a shortage of road space compared to number of road users. There is a scarcity of available land to build new roads or railways.

How does the free market solve the problem of scarcity?

If we take a good like oil. The reserves of oil are limited; there is a scarcity of the raw material. As we use up oil reserves, the supply of oil will start to fall.

Diagram of fall in supply of oil

If there is a scarcity of a good the supply will be falling, and this causes the price to rise. In a free market, this rising price acts as a signal and therefore demand for the good falls (movement along the demand curve). Also, the higher price of the good provides incentives for firms to:

- Look for alternative sources of the good e.g. new supplies of oil from the Antarctic.

- Look for alternatives to oil, e.g. solar panel cars.

- If we were unable to find alternatives to oil, then we would have to respond by using less transport. People would cut back on transatlantic flights and make fewer trips.

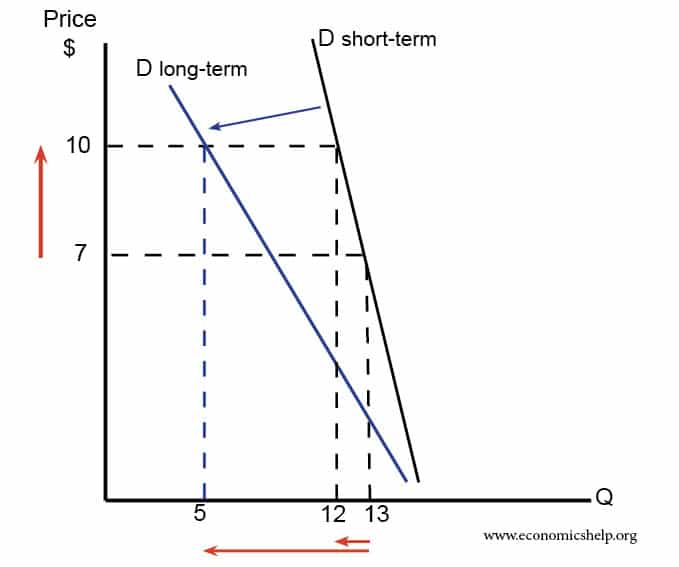

Demand over time

In the short-term, demand is price inelastic. People with petrol cars, need to keep buying petrol. However, over time, people may buy electric cars or bicycles, therefore, the demand for petrol falls. Demand is more price elastic over time.

Therefore, in a free market, there are incentives for the market mechanisms to deal with the issue of scarcity.

Causes of scarcity

Scarcity can be due to both

- Demand-induced scarcity

- Supply-induced scarcity

and a combination of the two. See more at: Causes of scarcity.

Scarcity and potential market failure

With scarcity, there is a potential for market failure. For example, firms may not think about the future until it is too late. Therefore, when the good becomes scarce, there might not be any practical alternative that has been developed.

Another problem with the free market is that since goods are rationed by price, there may be a danger that some people cannot afford to buy certain goods; they have limited income. Therefore, economics is also concerned with the redistribution of income to help everyone be able to afford necessities.

Another potential market failure is a scarcity of environmental resources. Decisions we take in this present generation may affect the future availability of resources for future generations. For example, the production of CO2 emissions lead to global warming, rising sea levels, and therefore, future generations will face less available land and a shortage of drinking water.

The problem is that the free market is not factoring in this impact on future resource availability. Production of CO2 has negative externalities, which worsen future scarcity.

Tragedy of the commons

The tragedy of the commons occurs when there is over-grazing of a particular land/field. It can occur in areas such as deep-sea fishing which cause loss of fish stocks. Again the free-market may fail to adequately deal with this scarce resource.

Further reading on Tragedy of the Commons

Quotas and scarcity

One solution to dealing with scarcity is to implement quotas on how much people can buy. An example of this is the rationing system that occurred in the Second World War. Because there was a scarcity of food, the government had strict limits on how much people could get. This was to ensure that even people with low incomes had access to food – a basic necessity.

A problem of quotas is that it can lead to a black market; for some goods, people are willing to pay high amounts to get extra food. Therefore, it can be difficult to police a rationing system. But, it was a necessary policy for the second world war.

Related pages

Good from what are you doing but you have to provide to us some of sample questions concerning the University level

l want to be explained further on scarcity as it is becoming hard topic for me to understand

When we even make a choice we have to forgo the other alternative.The alternative forgone in making am informed choice is also known as oppotunity

I really learned a lot in this website, thank you very much I appreciate

I want my text book explanation of social subject

Actually, I don’t understand about the entrepreneurship.. Can you please help me?.. I’m a senior high student for the upcoming school year..and We don’t have a actual class so please could you help me to understand this?😅

Thank you so much its clear

This makes some sense but the graphs just messed my head up pls help

I enjoyed the nature of information

The only “problem” with the free market is when it is interfered with. It is a natural process, by interfering with it you are indirectly interfering with nature. Everything on our planet is finite, everything has to be paid for. Every action has an equal and opposite reaction. The is no free lunch.

Interfering with the free market is like kicking a can down the road, it may seem just and righteous in the instant, but it is by no means sustainable ultimately over time.

Thank you so much