Abenomics refers to the economic policy of the current Japanese prime minister Shinzō Abe. The aim of the policy is to stimulate strong economic recovery and help the Japanese economy to escape a cycle of deflation, and low growth.

Can Japan break the cycle of low growth?

The range of policies include:

- Expansionary monetary policy (Quantitative easing, negative real interest rates, and an inflation target of 2%)

- Expansionary fiscal policy (higher government spending financed by borrowing)

- Weakening the value of the Japanese Yen to boost the export sector.

- Supply side policies ‘new growth measures’

How it is supposed to work

- Japan has suffered from a prolonged period of deflation or very low inflation. Since early 1997, the GDP deflator (a broad measure of the price level) has declined by 17 per cent. (FT) This deflation has increased the real debt burden of firms, consumers and the government and acted as a continued depressing factor on spending. (See: problems of deflation) By pursuing expansionary monetary policy and targeting higher inflation, they hope to change expectations of inflation and encourage more private sector investment and spending.

- Expansionary fiscal policy. Fiscal spending will increase by 2% in 2013, increasing the budget deficit to 11.5%. The aim of the expansionary fiscal policy is to make sure that the extra money supply feeds into the real economy. There is concern that quantitative easing alone, just leads to increased bank reserves. But, the extra government spending will provide a direct injection into the economy and provide a stimulus to aggregate demand (AD)

- Confidence and expectation. An important feature of ‘Abenomics’ is trying to change the economic mood and overcome the prevailing ‘economic defeatism’. Opinion polls suggest that many people are supportive of the attempts to overcome recession. This positive effort and talk of economic recovery is improving business and consumer confidence, and will act as a spur to increase consumer spending and private sector investment.

- Expansionary monetary policy and targeting higher inflation rates has helped to cause a depreciation in the value of the Japanese Yen. The depreciation in the exchange rate will make exports cheaper, and increased demand. Because exports are an important component of Japanese GDP, this depreciation is having a significant effect on the economy.

- The new growth policies include some supply side reforms such as trade liberalisation and deregulation.

Concerns over Abenomics

- Critics argue that Japan already has the highest level of public sector debt in the developed world (gross debt over 237% of GDP) Deficit hawks argue increasing the fiscal deficit is irresponsible given this high level of debt. However, supporters may argue that the government debt has been rising primarily because of two decades of economic stagnation. Strong economic growth is essential for reducing debt to GDP ratios. Also, because of the high level of domestic saving in Japan, most of the debt is financed through domestic savings. Japan is not so reliant on foreign borrowing. Low bond yields suggest there is still appetite for buying government debt. If the private sector really recovers, the government will be able to reduce the reliance on fiscal stimulus.

- Rising bond yields. If the policy is successful and economic growth increases, this will lead to higher bond yields. This will increase the cost of servicing national debt. However, although bond yields will rise with economic growth, that is still the main priority of the policy.

- Others criticise the expansionary monetary policy for risking inflationary pressures. If inflation starts to creep above 2%, people could lose confidence in holding bonds and savers could see an even bigger fall in the real value of their savings (real interest rates are already negative) However, this is arguably worrying about the wrong problem. Even with the recent policies, Japan is still struggling to escape from deflation.

- Some argue that the reliance on depreciation in the Yen, is an example of ‘beggar thy neighbour policy‘. I.e. Japan is benefiting from a weaker currency boosting Japanese demand, but this is at the expense of appreciation in other countries and lower demand in the US and Europe. However, supporters may argue that in the current economic situation, the most important thing is to pursue the most appropriate monetary policy. If this appropriate monetary policy causes a depreciation as a side effect, that is fine. Also, the Japanese Yen was arguably overvalued previously.

- Supply side reforms are inadequate. So far the supply side reforms have not sought to tackle many of the underlying structural problems in Japan, such as expensive labour market contracts.

- Another point worth noting is that with unemployment of 4.1%, Japanese economy has not been doing as badly as often perceived. The unemployment rate is considerably lower than Europe and US. This unemployment rate suggests there is less spare capacity in the Japanese economy than Europe.

- The initial burst of growth will need to be maintained, Japan has had many ‘false dawns’ in past few decades.

Initial impact

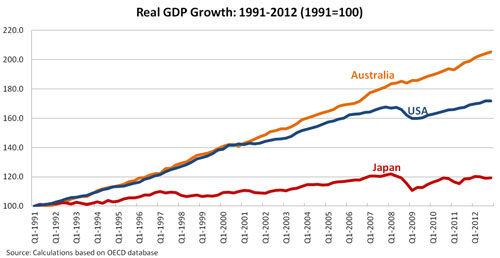

So far, the impact of these policies is relatively positive. Economic growth is higher in Japan than most other industrialised world. In the first three months of 2013, GDP increased at an annualised rate of 3.5% [WSJ] There has been strong export growth. Importantly, there appears to be a change in confidence and attitude towards the economy. People are more optimistic and the concentration is on economic recovery. Wage growth is negative, business investment is still weak, and it remains to be seen whether the pro-growth policies can maintain

What is the *real* standard of living in Japan?

In the UK a lot of nominal GDP is sales of cheap, short life, consumer goods (the “value added”). If we throw the goods out quickly and replace them, we boost sales and so GDP. Does it make us better off in real terms? It is a bit like smashing windows to keep glaziers employed and boost output, or digging holes and filling them in.

Maybe we could boost our *real* living standards by reducing waste; maybe the Japanese have done that, so low growth isn’t a problem.

There are so many people with huge economic problems that it’s impossible to think that the economic crisis is over. People are jobless with no hopes of finding work, public debt is soaring. Politicians have to come to terms with the fact that they need help, they need specialists in the economic crisis who have what is takes to face and more importantly fix the problems linked to the economic crisis. They need specialists like those from the Orlando Bisegna Index in New York, who have come up with made to measure anticrisis solutions over small territories, solving problems like unemployment, low income, and economic relief for families

The problem with Japan is the unbalanced spread of generations in the population. The money spenders are the 40-50 age group, as they have less financial constraints at home and generally higher salaries and more equity in their homes or investments. If this portion of the population decreases over time, then you get deflation. Japan is a generation away from this issue being able to naturally resolve. The first indicator will be income growth.