Economists generally agree that a high inflation rate has various economic costs and therefore, we should use economic policy to keep inflation low. Since the mid 1980s, governments have increasingly set strict inflation targets, e.g. ECB inflation of less than 2%. The Bank of England targeting inflation of 2% +/-1.

However, some economists argue that in certain conditions, inflation can be too low. Targeting a higher inflation rate can help the economy to grow and overcome problems of a liquidity trap, such as debt deflation, high unemployment and low growth.

However, other economists are less impressed. They argue that targeting a higher inflation is irresponsible. It doesn’t do anything to overcome problems of low growth, but will create additional problems of uncertainty and lost confidence in economic policy.

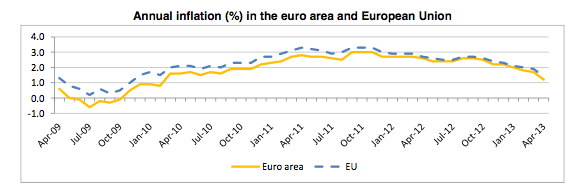

Eurozone inflation fell to 1.2%, in April 2012 but GDP also fell and unemployment rose to record 12.1%. Why are the ECB so keen on keeping inflation low?

Arguments for a higher inflation rate

- After a period of deflation, the price level may have been below its long term average. Example, suppose we had three years of 0% inflation. The price level will be 6% less than we would expect with our target inflation rate of 2%. Therefore, in this case, we need higher inflation to ‘catch up’ with the long term price level target.

- Higher inflation can help overcome a stagnant economy. If economies are stuck with zero or negative growth, then it may be necessary to tolerate a higher inflation rate to enable a loosening of monetary and fiscal policy. If the economy has a large negative output gap, then there is no need to fear runaway inflation. For example, in Europe at the moment, GDP has been falling, unemployment very high, but the ECB are mistakenly still targeting low inflation. If they could tolerate slightly higher inflation, it would make it easier for the economy to recovery. Although, there are some costs of a slightly higher inflation rate, the costs of unemployment are much higher.

- Cost push inflation misleads underlying inflationary pressures. Sometimes, Central Banks face a high headline inflation rate, but this is due to cost push factors (e.g. higher oil prices). Therefore, even though the economy is stagnant (not growing), inflation may be high because of these misleading cost-push factors. In this case it is a mistake to target inflation of 2%. One alternative may be to target core inflation – which strips away these misleading cost-push factors.

- In liquidity trap, higher inflation can encourage spending. In a deep recession, we see a rise in savings because people don’t want to spend. The problem is that savings can rise too quickly causing a recession. Higher inflation discourages excess saving and encourages spending, which the economy needs.

- Higher inflation reduces debt burdens. A higher inflation rate makes it easier to reduce debt burdens – both private and government debt. If inflation is too low, we risk debt deflation. This means spending will fall because we are struggling to deal with rising debt burdens. With low GDP growth, Europe is facing rising debt to GDP ratios, despite austerity. Targeting higher nominal GDP, which may require higher inflation, makes it less painful to reduce debt to GDP ratios,without the cost of high unemployment.

- In normal circumstances, targeting inflation of 2% may be best. But, in a liquidity trap / prolonged recession, governments need more flexibility to evaluate changed circumstances.

- Eurozone. The Eurozone present a particular dilemma. Many countries are trying to restore competitiveness through internal devaluation (cutting wages and prices). This is made more difficult by the low Eurozone inflation rate. With Eurozone inflation of 1%, for Portugal to restore competitiveness may require an inflation of -2%. But, this deflation in Portugal is very damaging. A higher inflation rate, would make it easier for the periphery to adjust, without requiring a prolonged slump and deflation.

Arguments against a higher inflation rate

- Allowing inflation helps increase future expectations. This means inflation will become harder to reduce in the future.

- Lose credibility of monetary policy. If Central Banks allow higher inflation, then they will no longer expect low inflation, and it will be harder to reduce inflation in the future.

- Using inflation to reduce burden of public debt risks losing confidence bond holders have in purchasing government debt. If savers see a reduction in the value of their savings because of inflation, they will be less willing to buy bonds in the future. Inflating away debt will have future costs as bond holders will demand higher interest rates to compensate risk of future inflation.

- There is an argument there is no trade off between inflation and unemployment. Monetarists may argue that allowing higher inflation will not actually lead to higher growth and unemployment. They argue demand side expansion just causes inflation, without any real increase in GDP.

- In a period of ultra low interest rates, higher inflation will erode the value of savings, making savers worse off. Pensioners may struggle to survive on declining real savings.

- Costs of higher inflation include, declining international competitiveness, menu costs, greater uncertainty leading to less investment, and reduced value of savings

Overall

The strongest case for allowing higher inflation is in the Eurozone. Yet, this is probably the least likely area to tolerate any deviation from the goal of low inflation. Usually targeting low inflation is sound economic strategy. However, if we look at Europe, we see a real economic crisis. Stagnant economies, deep recessions on the periphery, rising real debt burdens, record levels of unemployment. The depth of the recession threatens the social fabric. In this case, allowing moderately higher inflation can help escape the cycle of stagnant growth and rising real debt burdens. There may be some minor costs, such as a slight reduction in inflation credibility. However, I don’t accept that pursuing monetary and fiscal policies to escape a recession will lead to runaway inflation. Nor do I feel there will be a real loss of credibility. There is a need to concentrate on problems at hand, not potentially possible problems 5 years down the line. Even savers and bond holders need economic recovery. Higher inflation may appear bad news, but if it means Europe can escape the cycle of recession, it would be desirable for the long term interests of even savers.

A good question is whether higher inflation will be a magic bullet to enable higher growth. There is no guarantee that higher inflation will promote a strong recovery. Some may argue that it’s not about the inflation rate, but the correct monetary and fiscal policy. If the correct monetary policy causes slightly higher inflation, then that is a price worth paying. But, the persistent ECB fixation with low inflation is damaging the fragile Eurozone economy.

Related

While choosing your nursing pajamas, care has marketing campaign taken for more information on grab going to be the appropriate material and circumference and length for more information regarding ensure that you believe comfortable all of which will relax all around the element