The UK housing market is something of a national obsession. But, it faces numerous problems

- High prices (especially affecting younger people)

- High cost of renting – Shortage of properties

- Decline in birth rates due to high living costs

- Concealed households – people having to live with parents

- Inequality

- Volatility of prices

- Homelessness

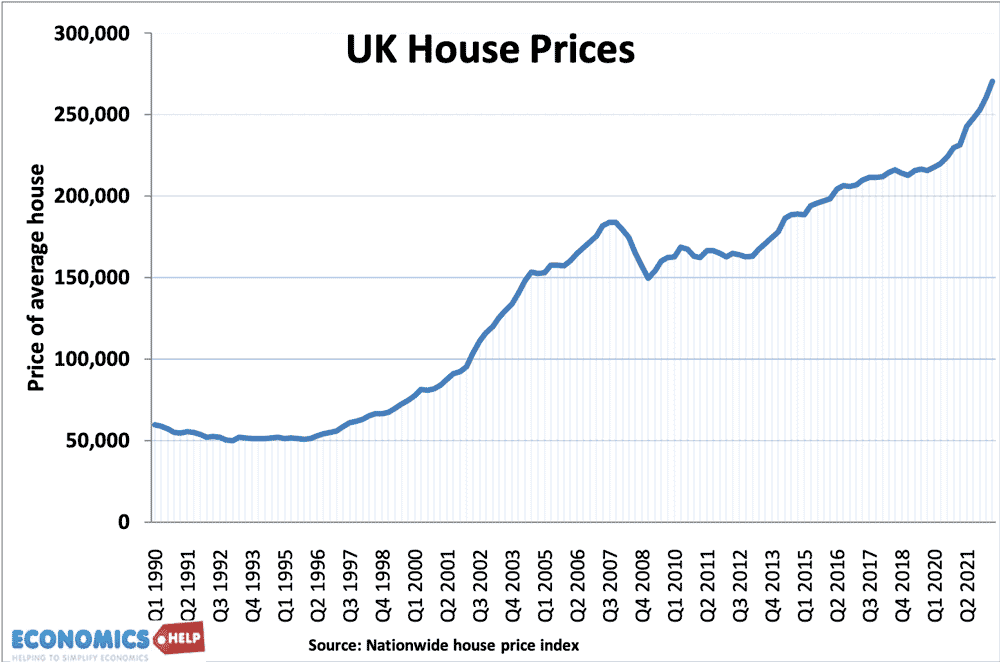

Since the early 1990s, house prices have risen 429%, but average incomes have not kept up – stagnating in recent years.

The average house price is now nearly seven times the average income – the highest level since the nineteenth century. Owning a home is often portrayed as the ultimate goal but for many that dream is out of reach, leading to a generation of renters, increasingly left behind in the property boom.

The problem is that renting – the alternative to buying is just as broken. The rental market is seeing an acute shortage of properties, with renters facing intense competition to get even low-quality and expensive rents. Rents have soared faster than inflation in recent years and are expected to keep rising.

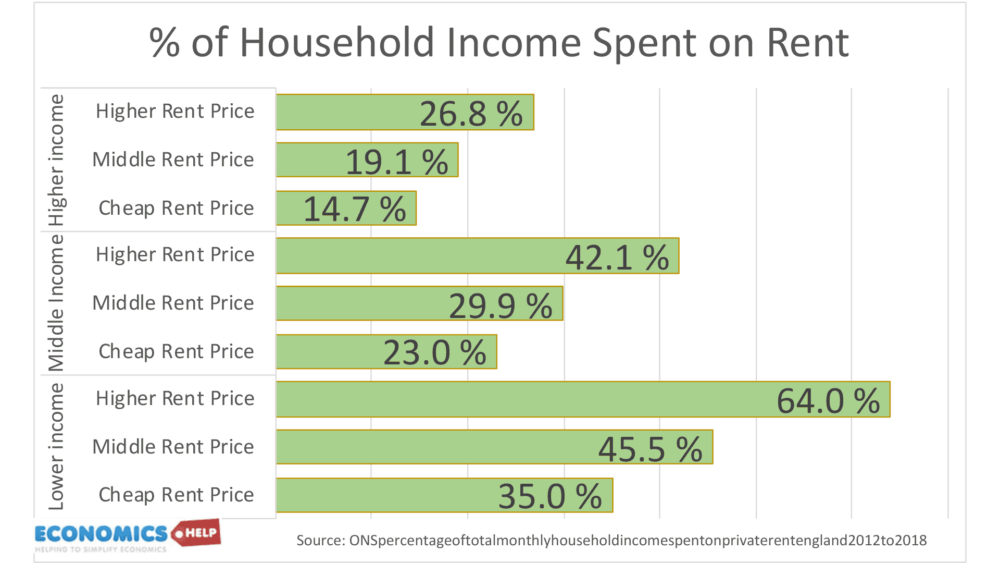

Rent can account for up to 57% of income amongst low income renters. Yet, the problems of the housing market is not just about high prices, we shall see how it has also distorted other aspects of the economy, family life, and equality and is storing up problems for the future.

A major problem of the housing market is that supply is very unresponsive to price. Price goes up, supply doesn’t.

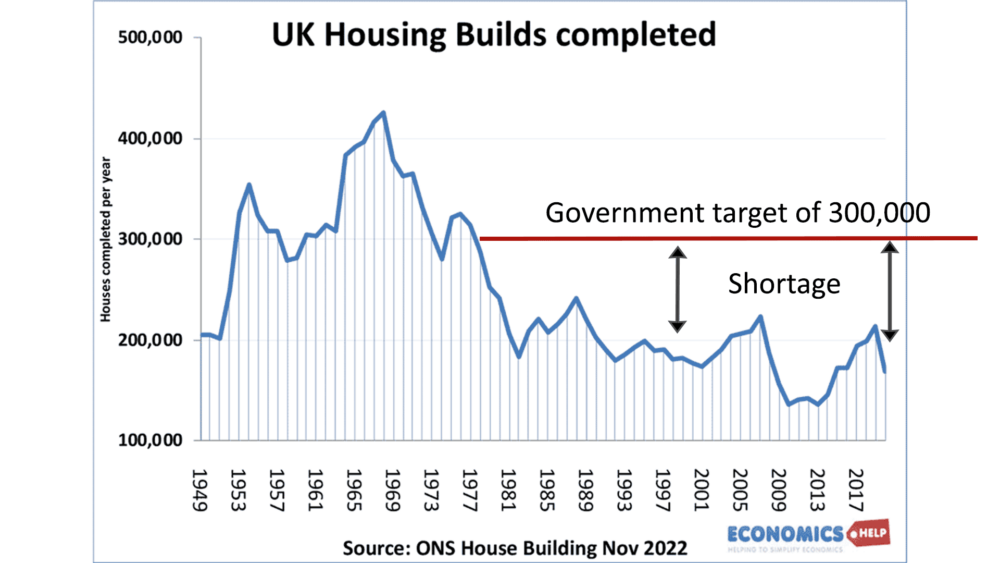

From the 1980s, social housing was sold off, but new social housing was not built. It was all left to the private sector. However, leaving it to the market is a real problem when it comes to housing. To build houses where they are needed is expensive and difficult, if not impossible. A combination of planning restrictions and legal barriers, means the UK is facing a shortage of housing. One report claims a missing 4 million homes. Others claim a backlog of closer to 2.1 million homes. It is open to dispute, but the UK does one of lowest rates of homes per person in Europe.

However, this shortage, if anything is likely to get worse. Under pressure from its own backbenchers, the government recently dropped compulsory targets for councils. Combined with very strict environmental legislation, homebuilding will be curtailed with industry forecasting a sharp drop from already low rates. This highlights an unresolvable tension in the UK housing market.

On the one hand, there is a shortage of housing causing economic misery. On the other hand, there is huge opposition to any new homebuilding because people don’t want to lose green fields. We know the problem, but we don’t particularly like the solution. In the short term, prices are falling in response to higher interest rates. But, what about the long-term, are we ever going to see a return to the affordability levels of the 1970 and 80s, when prices were 3 or 4 times the average income and within reach of most people?

Another problem with the UK housing market is the volatility. Whilst long-term prices have been rising, there is an element of speculation, which has caused housing to be seen as a surrogate for the stock market and pensions – which often provide better returns. It means that the housing market is not just about places for people to live, but places of speculation and investment. It has led to a rise in the number of second homes and also empty homes.

In the period of low interest rates, house prices soared, but now interest rates have increased, homeowners are seeing a rise in mortgage payments and renters are facing a shortage of properties. The swings in interest rates and market sentiment risk causing boom and busts like we saw in 1991 and 2008. It is an added element of uncertainty and periods of rapidly falling prices can easily damage the economy.

The problem is that housing has exacerbated wealth inequality – a divide between those who own and those who don’t. This rise in wealth has also magnified or even created a generational divide, with home-ownership increasingly being the preserve of the older generation, and young people being left out unless they can borrow from their parents. Lending from parents was worth £54bn in the past 10 years – a sign that getting on the property ladder is increasingly dependent on family help.

Like elsewhere in the western world, the UK is seeing a fall in fertility rates to below 2. Whilst there are many reasons for this. Economic costs are the most widely reported reason. Parents don’t want to have children or prefer to have smaller families, because they can’t afford to live in properties with more bedrooms. The cost for parents is also magnified when housing near good schools is more expensive. Living in expensive areas can get access to better education, but can push up prices even further. Another aspect of the housing market is that it increases the pressure for a household to two full-time earners, leaving less time for parents to stay at home with children during their early years.

The cost of housing is a brake on UK economic growth. The areas with the highest rates of employment growth are also the least affordable. The ratio of house price to earnings is over 12 times in London. This has forced many to leave the capital in order to find affordable accommodation. However, it leaves firms in the south and big cities struggling to attract sufficient workers, especially in public sector employment, such as education and health. It is not just high house prices, but the costs and difficulty of moving, which reduce labour flexibility. High quality and affordable renting sector, would do much to improve geographical flexibility, but the market is struggling to keep up with demand.

The worst manifestation of the broken housing market is the impact on homelessness. Shelter estimate there are 271,000 people recorded as homeless, including 130,000 children. Of these 2,400 are sleeping rough on any given night. Whilst there are different reasons for homelessness, the shortage of social housing and the cut throat nature of the UK’s private rented sector makes it easy for the vulnerable or unlucky to slip through the gap.

The shortage of homes has also influenced how we live. It is estimated that there are 1.6 million supressed households in the UK. This is people living together out of economic necessity rather than preference. It includes a record rise in young people stuck living with their parents. The rate has increased from 35% in 1998 to 42% in 2021. A reflection of the economic situation and cost of living. The UK may in theory be a rich country, but our living standards and quality of life are held back by the cost of housing.

The problem with housing is not just about price, many homes are defined as sub-standard quality, with problems such as damp and overcrowding. This can cause health problems as well as being unpleasant to live. In a survey of 5,000 tenants, by YouGov, 35 per cent of tenants claim to suffer from infestation, damp or electrical problems. Yet, the increase in rent controls and regulations which have been brought in recent years, have seen many landlords sell up. Combined with higher interest rates and falling yields, landlords leaving the market is a problem as it further reduces supply and pushes up price.

Another aspect of the housing market is that it is storing up problems for the future. In particular, those who face renting in the private sector will struggle when they reach retirement. When Generation Rent reach retirement, it will be a social and economic problem. Pensioners who own a home and who have paid off their mortgage will have a completely different economic reality to those who have to continue paying market rents.

Further reading