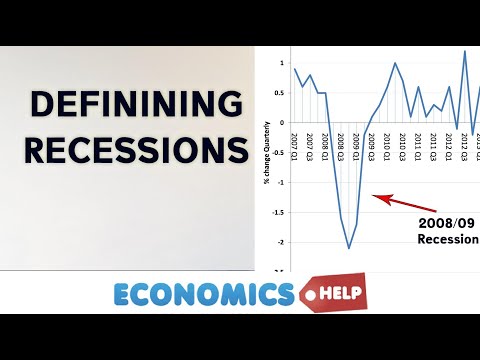

A recession is defined as a period of negative economic growth. However, there can be different causes and types of economic contraction. Different types of recession will influence the length, depth and effects of the recession.

These are some of the different types of recessions.

- Boom and bust recession (e.g. UK 1991/92) – Very high growth causing inflation. Then recession as interest rates rise

- Balance sheet recession (e.g. Global recession of 2008/09 after credit crunch)

- Supply-side shock (1973/74 and 2022 recession due to higher oil prices)

- Depression (the 1930s, decline in GDP)

1. Boom and bust recession

Many recessions occur after a previous economic boom. In the economic boom, economic growth is well above the long run trend rate of growth; this rapid growth causes inflation, and a current account deficit and the growth tends to be unsustainable.

- When the government / Central Bank see that inflation is getting out of control, they respond by implementing tight monetary policy (higher interest rates) and tight fiscal policy (higher taxes and lower government spending)

- Also, an economic boom is often unsustainable, e.g. firms may be able to temporarily produce more by paying workers to do overtime, but this might not last.

- Also, in a boom, consumer confidence tends to soar. As a result, there tends to be a fall in the savings ratio and a rise in private borrowing to finance higher spending. The economic boom is financed by rising debt. Therefore, when there is a change in economic fortunes, consumers radically change their behaviour, rather than borrowing they seek to pay off their debt and the saving ratio increases causing a fall in spending.

Examples of boom and bust recession

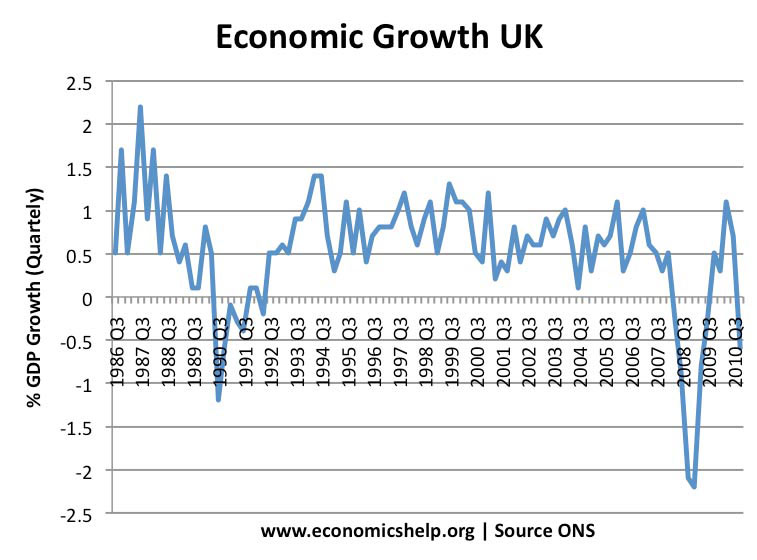

- 1973 recession in the UK – following Barber boom of 1972. (Though 1973 recession was also caused by oil price shock)

- 1990-92 recession – following Lawson boom of the late 1980s. In the late 1980s, UK growth increased to over 5% (annual), causing inflation to rise to double figures. In response to the inflationary growth, interest rates were increased. But, higher interest rates caused a fall in disposable income, a fall in house prices fell, and a decline in consumer confidence. This lead to the recession of 1991-92.

Features of boom and bust recessions

- Can often be short-lived

- If caused by high-interest rates, reversing rate increases can cause the economy to recover

- Can be avoided by keeping growth close to long-run trend rate and inflation low.

2. Balance sheet recession

A balance sheet recession occurs when banks and firms see a large decline in their balance sheets due to falling asset prices and bad loans. Because of large losses, they need to restrict bank lending – leading to a fall in investment spending and economic growth.

Also, in a balance sheet recession, we also see falling asset prices. For example, a fall in house prices causes a decline in consumer wealth and increases bank losses. These are other factors which causes lower growth.

Example

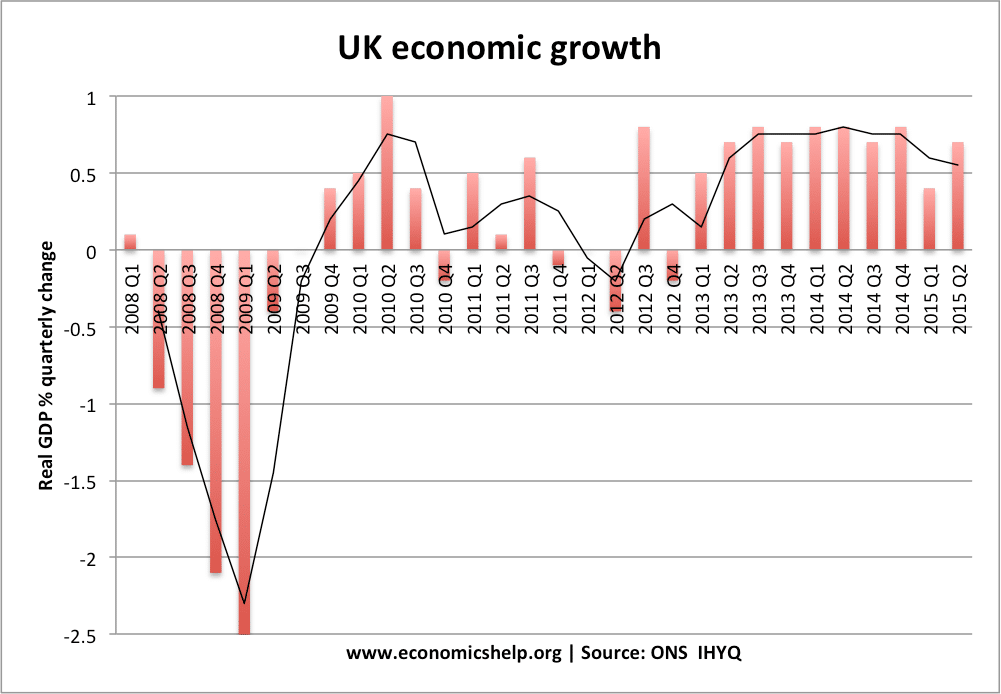

- 2008-09 recession. In 2008, bank losses led to a fall in bank liquidity and banks found themselves short of cash. This led to a fall in bank lending, and it was difficult to get funds for investment. Combined with a collapse in confidence, the economy went into recession – despite interest rates being cut to zero.

Features of balance sheet recession

- Can last a long time

- Cuts in interest rates may fail to cause economic recovery due to a liquidity trap.

- No quick recovery

- More susceptible to a double-dip recession

- To avoid a balance sheet recession, we need to avoid a credit and asset bubble. Targeting inflation is not sufficient.

3. Depression

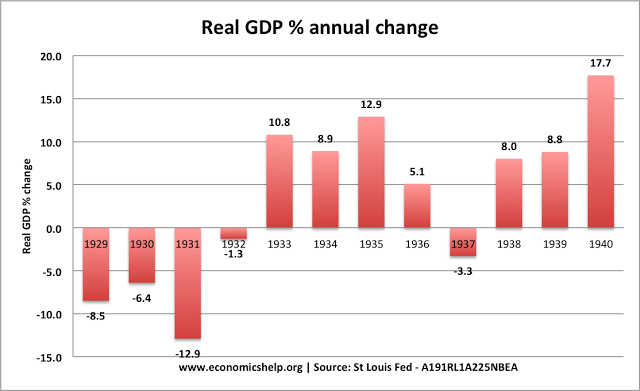

US GDP 1929-32

A depression is a prolonged and deep recession, where output falls by over 10% and very high rates of unemployment. A balance sheet recession is more likely to cause a depression because falling asset prices and bank losses have a long-lasting impact on economic activity.

4. Supply-side shock recession

A very rapid rise in oil prices could cause a recession due to the decline in living standards. In 1973, the world was highly dependent on oil. The tripling in the oil price caused a sharp fall in disposable income and also caused lost output due to lack of oil.

Supply-side shock (Stagflation)

Features of supply-side shock recession

- The world is less dependent on oil than in the 1970s. The rise in oil prices in 2008 was only a minor factor in causing the 2008 recession.

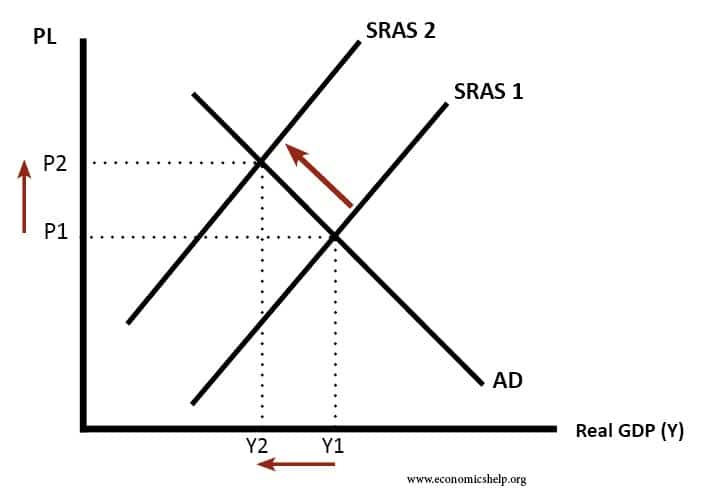

- A supply-side shock causes short-run aggregate supply (SRAS) to shift left. Therefore, we get both a lower output and higher inflation. Often known as ‘stagflation.’

- The cost-push inflation of 2022 was an important factor in promoting economic slowdown in UK and Europe

High inflation caused by rising oil, gas prices, became embedded causing other prices to rise. This led to Central Bank raising interest rates to bring inflation under control. But, the twin costs of high inflation (combined with low wage growth) and rising interest rates led to lower demand.

Demand-side shock recession

An unexpected event that causes a sharp fall in aggregate demand. For example, the short-lived recession of 2001 (GDP fell only 0.3%) was partly caused by fall in consumer confidence as a result of 9/11 terrorist attacks (and also the end of dot com bubble).

Covid-Recession – Black Swan Recession

The 2020 Covid Recession was an unexpectedly sudden drop in output, due to the economic lockdowns. It is sometimes known as black swan event as the Covid pandemic was non economic and unexpected.

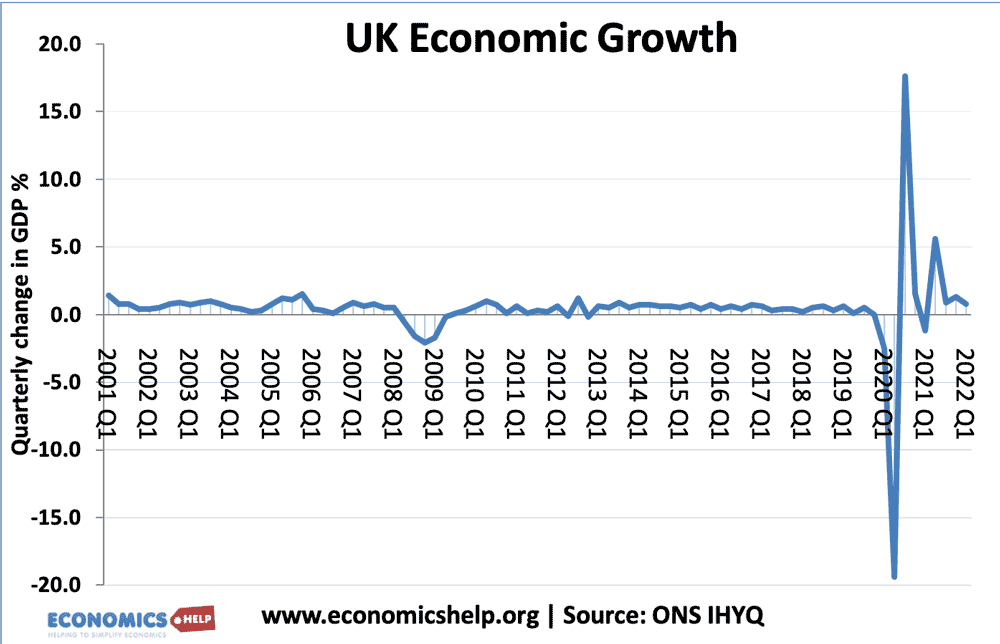

The 2020 Covid Recession was an unexpectedly sudden drop in output, due to the economic lockdowns. Output rebounded when normal economic activity resumed. The Covid Recession was off the scale in terms of nearly 20% fall in GDP. The great recession of 2008/09 with 2.5% is barely noticeable.

Different shaped recessions

- W-shaped recession – refers to a double-dip recession, where the economy goes into recession shortly after recovering from first

- V-shaped recession – refers to a quick recovery after an initial recession

- An L-shaped recession – refers to a period of stagnant recovery after an initial fall in GDP. Even though technically the economy may have positive growth (e.g. 0.5%), it still feels like a recession because growth is very slow and unemployment is high.

Depth of recessions

Source: ONS Total fall in GDP.

Biggest recession 1929-30 – 10% fall

Cumulative Recession

In 2019, several economists suggest the next recession will be a combination of factors

- Low confidence

- Poor productivity growth

- Falling house prices

- Weak investment spending

- Uncertainty over Brexit in UK / political turmoil in US.

Related