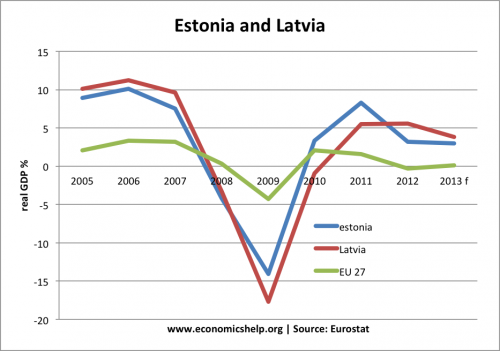

The Latvian and Estonian economies have recently experienced – an economic boom, a spectacular bust, and recovery. Their experience is a chance to evaluate the merits of fixed exchange rates, austerity and the issues of an economy based on trade and capital inflows.

Aspects of the Baltic economies

- Boom period between 2000 and 2007

- Great recession of 2008-2010

- Readjustment policies of fiscal contraction whilst maintaining fixed exchange rate.

- Economic recovery from 2011

Lessons from the boom

Both Latvia and Estonia experienced rapid economic growth in the early 2000s. This was helped by various policies and economic factors

- Free market reforms enabled growth of efficiency and productivity. From 1991, the economies became more market oriented with policies of privatisation and deregulation, enabling greater incentives to be efficient.

- Latvia and Estonia are both small, open economies where free trade has contributed towards economic growth. In Latvia, exports account for 33% of GDP, including raw materials, such as timber, agriculture and manufacturing products.

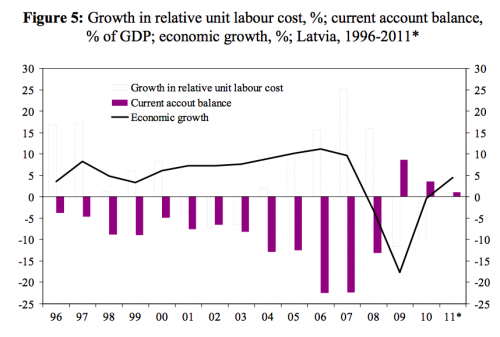

- The open nature of the economy attracted significant capital inflows from Europe. These capital inflows helped to finance a growing current account deficit, which reached 20% of GDP in Latvia and 16% of GPD in Estonia.

Source: Latvia report, EU

Record levels of economic growth in Latvia, led to a corresponding rise in the current account deficit.

This suggests that the economic boom was unsustainable. High rates of economic growth were only possible because of the large inflows of capital. But, this made the economy vulnerable to any economic downturn elsewhere in Europe.

This period of high economic growth massaged the fiscal deficit, improving tax revenues and creating a budget surplus. However, in 2007, these capital inflows dried up as European banks needed to improve their balance sheets and couldn’t afford to continue to lend to the Baltic states. The fall in capital inflows caused a fall in domestic demand; this was quite serious because the economy relied heavily on these capital inflows. As domestic demand fell, it lead to lower consumer spending, higher unemployment and a negative multiplier effect. The impact was a very steep recession.

When the capital inflows dried up Latvia and Estonia were left with a balance of payments crisis, a very high current account deficit. Many economists suggested that in this situation, the best solution is to devalue the exchange rate. A devaluation will help to restore competitiveness and improve the current account.

However, Latvia and Estonia both maintained their currency peg and didn’t devalue. This meant that to restore competitiveness, they had to reduce labour costs through deflationary policies. To reduce the growing budget deficit, the governments embarked on austerity, cutting government spending and increasing taxes. This deflationary fiscal policy had the following effects:

- A reduction in the budget deficit

- A reduction in domestic demand and falling GDP

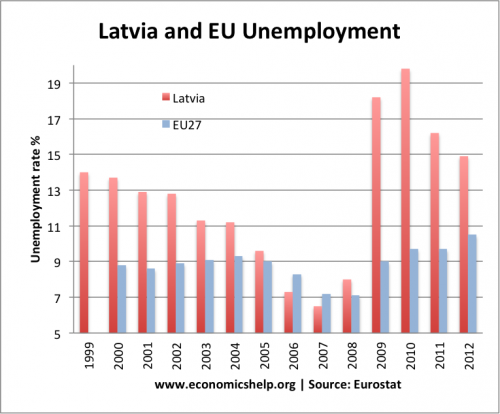

- A rise in unemployment

- Contributed to falling real wages.

The economic situation was so dire both countries experienced significant net migration with young unemployed people moving elsewhere in Europe.

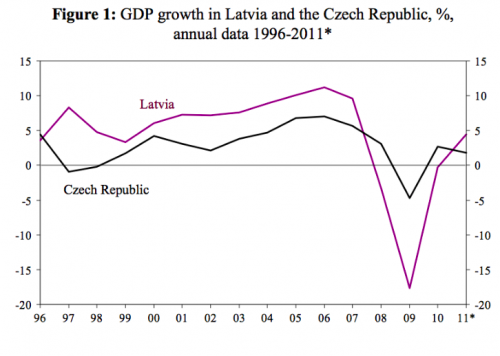

The bigger the boom, the bigger the downturn tends to be. If we compare Latvia and Czech Republic, we can see that the Latvian recession was much deeper.

Source: Latvia report, EU

Source: Latvia report, EU

Recovery

After the depth of the recession in 2010, both countries experienced relatively strong economic recovery, with growth rates of 4% forecast for 2013. This is much better than the rest of Europe. To some, this is evidence that austerity and fixed exchange rates is compatible with a strong economic recovery. The Baltic states have been able to restore competitiveness through lower wages and lower prices. Their current account deficits have moved into surplus and there has been a strong recovery. Furthermore, they are now in a good position because their levels of government borrowing is relatively low. Therefore, they are in a strong position to grow and complete the recovery.

However, others are less impressed. Firstly, the recessions in both Latvia and Estonia was very deep. The austerity policies, combined with fixed exchange rate led to a depression level fall in GDP. In the Baltic states, GDP fell by over 20%, leading to mass unemployment. In 2012, Estonian and Lithuanian GDPs were still 34 per cent below trend. (Latvian economies are no model at FT)

This rise in unemployment would have been even higher, if it had not been for net migration. Even after the recovery, real GDP is still below the peak of 2007.

Lithuania experienced a 10% fall in the population between 2007 and 2012, this is quite significant given the small size of the economy. Estonia (pop. 1.3m), Latvia (pop. 2m) and Lithuania (pop. 3m)

Evaluation

Both Latvia and Estonia have been helped by the fact that their economy is relatively open, with exports a strong part of the economy. The collapse in domestic demand during the recession has been offset by a rise in exports, helped by their increased competitiveness. Countries whose exports are a smaller % of GDP will find it more difficult to recover from a fall in domestic demand. For example, Greece has pursued austerity with a fixed exchange rate, but exports are a smaller % of the economy and so the fall in Greek domestic demand has been more damaging to the economy.

It is also worth pointing out, that it depends how much austerity has been followed. In Greece, the budget deficit has been reduced by 15 per cent of potential GDP between 2009 and 2012. Latvia by contrast tightened its cyclically adjusted general government deficit by 5.3 per cent of potential GDP between 2008 and 2012. (Latvian economies are no model at FT)

It depends how flexible labour markets and accommodating the workforce are. To a large extent, there has been a greater consensus in supporting austerity in the Baltic nations, than Greece or Spain. The Baltic states a strong political imperative in supporting EU membership. If trade unions and workers resist nominal wage cuts, then it is harder to restore competitiveness through lower wages.

Conclusion

The experience of Latvia and Estonia should firstly be a warning for allowing an unsustainable economic boom financed by huge current account deficits.

To some extent, the experience of the Baltic states show that small open economies can pursue austerity with a fixed exchange rate and escape the cycle of austerity and falling GDP. However, it came at a large short term cost of very high unemployment and depression level slump. Also their experience is not necessarily applicable to larger EU economies, which have exports as a smaller share of GDP.

The policies adopted by Baltic states may be less successful for other countries if:

- Countries have higher labour costs

- There is more political resistance to the policies of austerity and wage cuts

- Less flexible labour markets and less potential for migration.

- Countries have bigger banking debts which make it more difficult for IMF / EU to offer bailouts.

Related

Thank you for the article. I studied at the Faculty of Economics and it is very interesting for me to read about the economics of different states