Readers Question: To what extent are higher government debt levels a constraint on economic growth? There has been much debate about the extent to which high levels of government debt might slow down rates of economic growth. In particular, a 2010 paper “Growth in a Time of Debt,” by Carmen Reinhart and Kenneth Rogoff seemed to suggest that GDP growth significantly falls once government-debt levels exceed 90% of GDP. This paper was used as a justification for austerity in both the US and EU, but the paper has recently received substantial criticism. Firstly because an excel coding error left out several countries data. Secondly, because it is not clear whether high debt causes low growth or low growth causes higher debt levels. In 2010 two American Economists Carmen Reinhart and Kenneth Rogoff, circulated a paper, this paper suggested that once government debt reached 90% of GDP it led to a sharp drop off in economic growth. It was very influential in 2010 as there was a political interest in reducing debt. However, the paper was later criticised on numerous fronts

They omitted some data

There was an excel coding error

They used questionable statistical analysis.

Later researchers couldn’t replicate their results and only found a very weak link between debt and lower growth rates. Also, they were criticised for their assertion that

“growth drops off sharply when debt exceeds 90 percent of GDP”.

Because even if there is data suggesting a relationship between growth and debt. It remains another question of which factor causes the other factor. It could be that countries with slow growth tend to accumulate debt to GDP (in a recession, you expect debt to GDP to rise. A fairer statement is to say

“countries with debt over 90% of GDP tend to have slower growth than countries with debt below 90% of GDP”

Public debt and Growth OECD There is a reasonably good summary at the Economist here – relationship between growth and debt. Source: De Long. The relationship between growth and debt amongst G7 in post-war period. However, you have to be careful from reading too much in this. E.g. Japan’s post-war miracle with growth of 10% + is different era to today’s situation. But, it is worth mentioning other papers have given a mixture of results.

A 2010 IMF paper turns up “some evidence” of a 90% threshold.

A 2011 study by the Bank for International Settlements identifies a threshold of 85%.

A 2012 IMF paper found “there is no particular threshold that consistently precedes sub-par growth performance.”

Theory behind Growth and debt link

Let us examine the theory behind the possible link between government debt and economic growth Firstly, how might high government debt levels constrain economic growth? Crowding Out. Higher government debt usually requires the government to borrow from the private sector. Therefore, with higher government debt, there is likely to be a fall in private sector investment as the private sector use funds to buy government bonds. In addition, some economists argue that government spending tends to be more inefficient than the private sector. For example, if the government borrow to finance higher pension commitments, there will be less impetus to boosting economic growth than if the private sector had been free to invest itself.

However, crowding out is only likely to occur if the government borrows when the economy is close to full capacity. If the government borrow when savings are high and the economy is stuck in a recession, then there will not be crowding out, but an actual injection of spending into the economy. The government debt is financing spending which otherwise would not occur. In other words, in a recession, higher debt could cause higher growth rates than countries who try to cut budget deficits. The fact European economies have entered a double-dip recession after pursuing austerity policies, suggests there is empirical support for this.

High debt levels eventually exhaust private saving. The argument is that moderate levels of government debt can be financed by domestic saving levels, and therefore there isn’t crowding out. However, if government debt increases above a certain level, it will be harder to finance the debt from ordinary savings. The government will need to divert resources from investment and encourage more saving through higher bond yields. The government may also rely on more on volatile foreign borrowing.

However, even if government debt does lead to a fall in private sector investment and spending, in theory, aggregate demand should be unaffected. If government spending increases by £5bn, and is financed by borrowing £5bn from the private sector, overall AD is unaffected by the shift in the sector of the economy from the private to public sector.

Higher bond yields. A concern about higher debt levels is that there comes a point when markets start to fear government default. For example, suppose government debt rises above 100% of GDP, bond traders may feel that there is now a risk governments could actually default (or resort to inflation which is effective default) and they could potentially lose money. Therefore, markets will demand higher interest rates to compensate for the increased risk of default. These higher bond yields, will increase debt interest payments and also push up interest rates around the economy. The higher interest rates will cause lower investment and lower spending. Thus we can have a reason why higher debt could lead to lower economic growth. Because higher debt pushes up interest rates. In the Eurozone, we saw several countries with rising debt levels have sharp increases in bond yields. Following these higher bond yields, growth rates fell.\

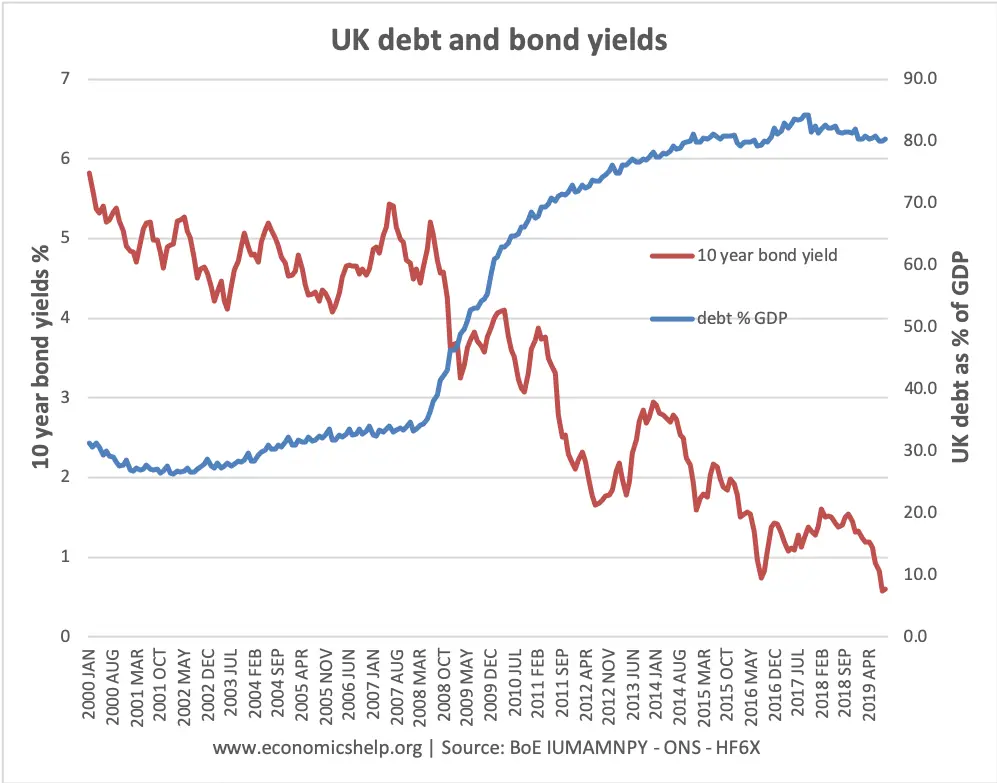

However, there is no guarantee that higher government debt levels will cause higher bond yields. Between 2008-13, the UK and US have seen substantial increases in the level of public sector debt, but bond yields have fallen. In the post war period, the UK had debt levels of over 200% of GDP, but bond yields were not excessive (and growth rates high). There is also no clear link between debt levels and bond yields. For example, gross public sector debt in Japan is over 230% of GDP, but bond yields low. Spain saw rising bond yields with debt of less than 60% of GDP. The real problem for the Eurozone was not public sector debt, but the lack of a Central Bank to intervene in the bond market. In 2012, when the ECB did finally intervene, bond yields fell – despite growing debt levels.

Confidence. Another argument is that high debt levels cause a loss of confidence. For example, the business may expect future tax increases to repay debt. Also, if business fears a government default and / or potential inflation, they may reduce spending and investment. This loss of confidence could lead to lower economic growth.

However, it is hard to find any strong evidence that consumer and business confidence is directly affected by government debt levels. The EU hoped that austerity policies of 2011 would ‘improve confidence‘. But, actually, the deficit reduction policies caused a collapse in confidence and economic growth. Consumers and firms confidence is based on more immediate factors, like employment, real wages and house prices than government debt levels.

The causation issue Low growth will cause higher debt to GDP ratio. If we have low or negative economic growth, we would expect debt to GDP ratios to rise. With negative growth, tax receipts fall, and spending on unemployment benefits increase. Also, falling GDP will increase the debt to GDP ratio. If we look at countries like Spain, Portugal and Greece during 2010-13, we see high levels of debt and low economic growth. But, these are countries trying to reduce budget deficits through spending cuts. The biggest factor behind rising debt levels is the continued recession. Conclusion It is hard to make generalisations about the effect of debt on economic growth because so many factors affect growth. For example, in the 1920s, the UK had a high debt to GDP ratio and low rates of economic growth. In the 1940s and 1950s, the UK had even higher levels of government debt, but economic growth was quite strong. Irish government debt was very high in the late 1980s and early 1990s, but this was not a constraint to the economic boom of the 1990s. There is no direct link between levels of debt and rates of economic growth There can be circumstances when high debt levels act as a constraint on economic growth. If markets were really concerned about the ability of the government to repay, it may cause higher bond yields, lower confidence and reduce investment. However, if a country has its own Central Bank, there are not many examples of countries of actually have these rapidly rising bond yields in response to debt fears. Further evaluation It depends on why the government is borrowing. Is the government borrowing to finance public investment or is it borrowing because of a rapidly ageing population and the need to spend more on pensions and health care. Is monetary policy accommodative? If government debt is high, but there is a tightening of monetary policy and overvalued exchange rate, then you would expect lower growth. High debt, but expansionary monetary policy would give a different result. What is the past record of the country? A country with no history of default may be able to borrow substantially more than a country with a track record of default Is there a patriotic incentive to buy debt? e.g. in World wars, the UK was able to tap patriotic sentiment to sell bonds and finance government debt at low-interest rates. Do investors fear inflation? If savers fear, high debt will be inflated away, they may refuse to buy bonds Related