Recently, there has been much debate about the direction of monetary policy. Should we make monetary policy ‘looser’ – expansionary monetary policy through quantitative easing / lower interest rates in order to boost growth and reduce unemployment. Or should we consider ‘tightening’ monetary policy – higher interest rates, no quantitative easing in order to reduce inflation

Most economists would agree monetary policy involves

- Maintaining a low and stable rate of inflation.

- Promoting sustainable economic growth and low unemployment.

These two economic goals may not sound too controversial. But, there is a big debate about which goal is more important, and whether we should ever sacrifice a strict inflation target to pursue higher economic growth.

To some economists, the overriding target of monetary policy should be low inflation. They argue that if the Central Bank targets low inflation, then that provides the optimal environment for long-term economic prosperity. If the Central Bank starts targeting economic growth and ignoring inflation, then there is a danger that the Central Bank will lose credibility. The economy will end up with higher inflation, without any long term boost to economic growth. Furthermore, if you allow inflation to increase, this increases long-term inflation expectations and, in the future, it will be more difficult and costly to keep inflation low.

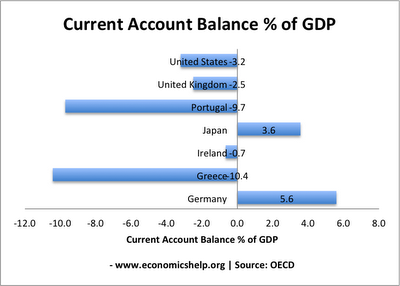

This is essentially the view of the German Bundesbank, and by and large the European Central bank.

If you look at an economic boom, such as the late 1980s in the UK, in this case inflation was allowed to rise as the UK pursued a higher than usual rate of growth. However, it later proved unsustainable and we had a boom and bust.

If low inflation is seen as primary economic goal, then:

- Quantitative easing is seen with great distaste as there is the possibility of future inflation.

- There should be no flexibility over the inflation target. E.g. even temporary cost push inflation should be a matter of concern, over fears that the higher inflation could change expectations and lead to permanent inflation.

- There is an unwillingness to use monetary policy to boost demand and hasten economic recovery.

- The solution for high unemployment and negative growth tends to be:

- Supply side policies to increase competitiveness

- patience, allowing market forces to invest, encouraged by macro economic stability of a low inflation environment.