Readers Question: In 2008, did banks lend money to people who wanted to buy a house because they believed that the value of the housing market would keep rising? So even if people defaulted on their loan repayments then the banks could reposes the house as it was used as collateral. As the value of the house would be of greater worth than the loan so that the banks could make a profit. Is this correct? Thanks!

This is partially correct. The great housing boom lasted from 1994 to 2006/07. But, in particular the period 2000 to 2007.

Mortgage lenders in both the US, UK and Europe became very keen to lend more mortgages because of rising prices, but also other factors, such as over-confidence, ability to borrow short term money / resell mortgage bundles. There were also significant differences between US lending and lending in Europe. In the US, mortgage lending was the most aggressive. UK and Europe retained some controls, but even so, mortgage lending rose sharply.

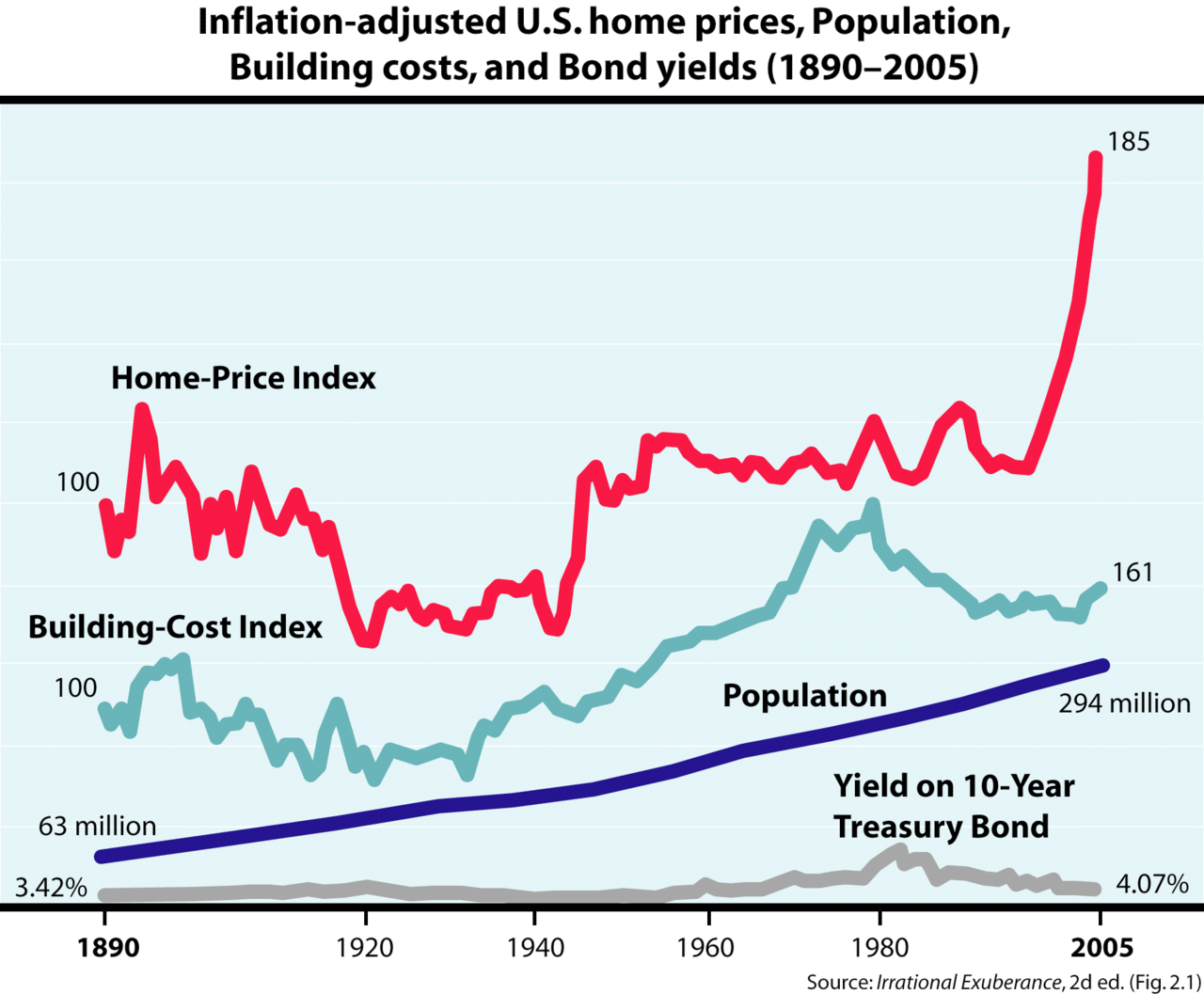

US Housing boom in historical context

{kind=link}

Causes of the US Housing boom

The US housing boom was caused by a number of factors, but extravagant mortgage lending was a key factor.

- Rising property prices created a positive wealth effect. This encouraged people to try and get on the property land (people who previously rented).

- Rising house prices also encouraged banks to lend mortgages because – as you say – even if people defaulted, the bank could make a profit on its mortgage lending by selling the house at a higher price. Usually lending a mortgage is quite a good investment for a bank, especially if house prices rise.

- The rising demand and rising supply of mortgages created a strong effect for pushing up house prices. It became a mutually reinforcing circle. Rising house prices encouraged banks to lend. More bank lending encouraged people to buy, pushing up prices.

- Over-confidence. This climate of rising house prices definitely encouraged over-confidence in the banking sector and amongst householders. There was a feeling that housing was one of the best forms of investment – you couldn’t go wrong with a house.

- Short-term bonuses. In the US, a feature of mortgage lending was that people were employed to sell mortgages who had no interest in checking whether it was suitable in the long term. There were very lax mortgage controls. Mortgages were sold with ‘teaser’ deals to make the first two years cheap and the later higher rates hidden from view. These mortgage sellers were not considering whether it made sense, they were just trying to sell the mortgages to get their commission. Financial bodies were happy to have these rogue salesmen because they thought house prices would keep rising. Also, bankers often got substantial bonuses from the mortgage boom; risky lending often paid high bonuses – encouraging a climate of risk taking.

- Lender of last resort. Banks are unusual in a capitalist economy. Because unlike any other industry, the government/ Central Bank are very nervous about allowing them go out of business. If banks go bust, it can cause a fall in the money supply / collapse in confidence and recession. Because banks have a safety net – it arguably encourages taking risk (Moral hazard). If it goes wrong, the government bailout the banks – which is what happened to several British banks like RBS, Bradford and Bingley.

- Short-term borrowing. In the great housing boom the over-confidence in the financial sector encouraged banks to borrow money on ‘short-term money markets’ to be able to have more funds to sell long-term mortgages. To simplify the scenario, they borrowed short term loans at 2%, and then sold mortgages at 5%. This increased their profitability because they could lend more mortgages. But, it meant that banks reserve ratios fell. Their mortgages were no longer backed by savings (like the old building societies). The mortgages required an easy access to these short-term money markets. However, because banks could now lend more mortgages, a new class of people were able to buy a house – pushing up prices even higher.

- Another way of financing more mortgage lending was to resell the mortgage debt to other banks. (This is how Europe became affected by US credit crunch. European banks bought many of these mortgage debt bundles.

- New types of mortgages. In the great housing boom, new types of mortgages were offered – income only, 100% of income, self-certification. (I got a self-certification mortgage myself, enabling a mortgage several times income

- Rising real incomes. After the wobble of 2001, real incomes rose, helped by relatively low interest rates, especially in the US.

- Modest rise in interest rates 2004-06

The rise in US interest rates from 2004-06 was relatively modest, but it was sufficient to burst the housing bubble because so many had taken out a large mortgage assuming (hoping) interest rates would stay low like 2002-03.

These are some of the factors behind the great housing market boom and bust.

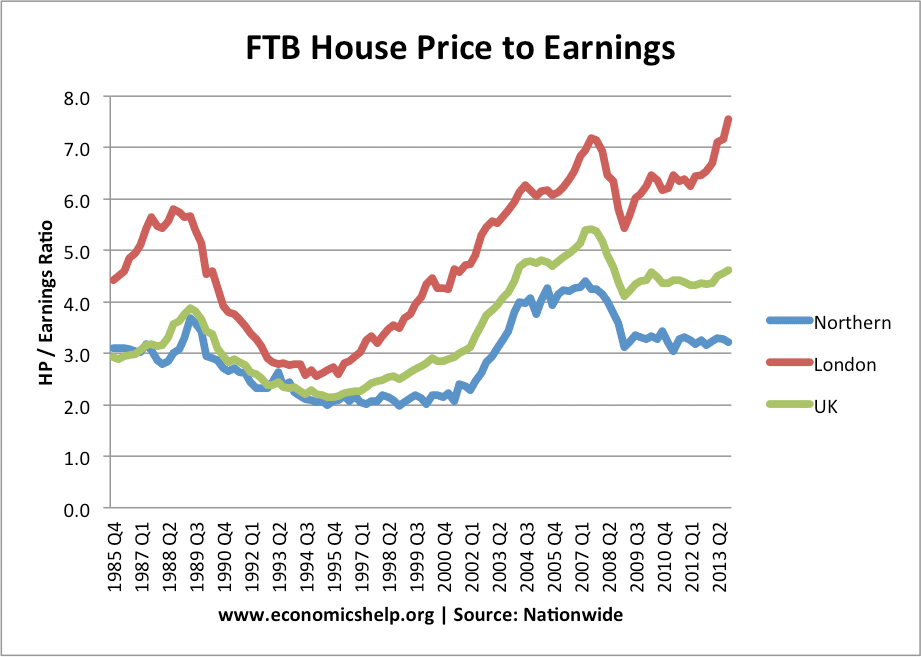

House price to earnings in UK

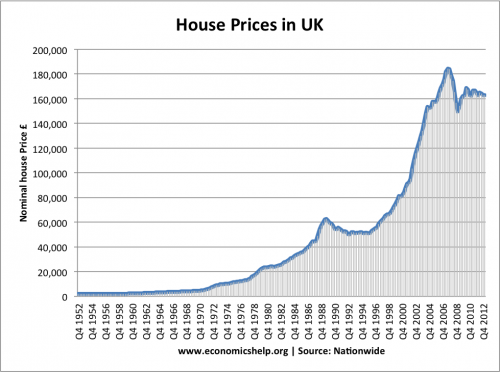

UK House prices

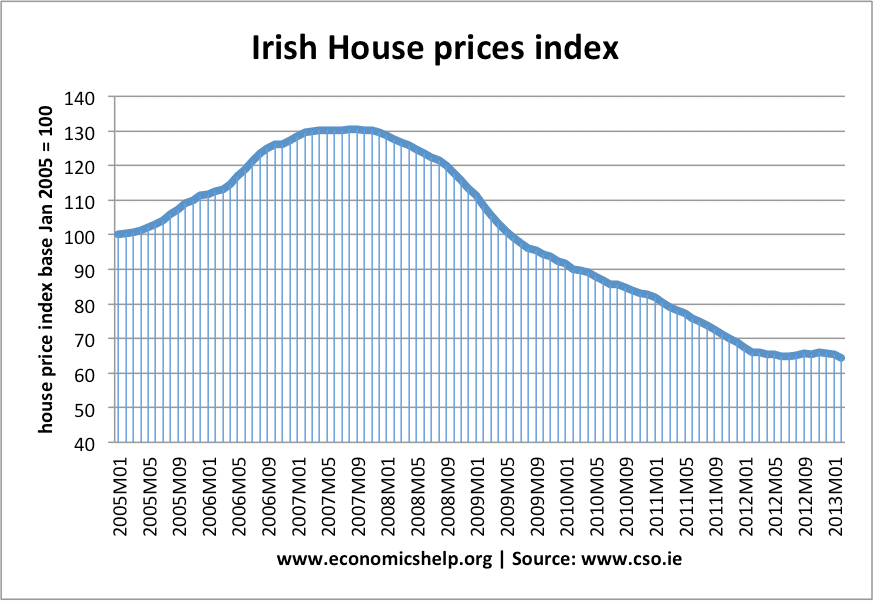

Ireland

Ireland was an example of another country with rapid house price growth. There was a real boom in Irish house prices which caused a boom in home building. The above graph shows the end of the housing boom.

Related

Do you think the help to buy scheme is fuelling a housing bubble? Only about 3% of houses are bought through this method but do you think that it is likely that a bubble will develop? Is this a suitable way to get people on to the property ladder?

It may not be the most suitable way to get people on the ladder but it is equally not a bad stat. It goes to show that some few people actually needs a nudge to get going into the housing market. I do not think it could get to the bubble stage yet via this method.

This will be needed in Nigeria to help with the housing gap and glut in the high brow housing market.

Anytime an artificial market is created, as in packaging loans that would be difficult if not impossible to repay, 2 things happen. A. People that should not get loans do get loans. B. The people who shouldn’t get loans do not pay. Period, then investment funds buy the excess housing when prices go down due to excess inventory. Rinse and repeat.