In 2022, the UK economy is struggling with very weak economic growth and one of the highest inflation rates in the OECD. Some of these problems can be attributed to global short-term problems, in particular recovery from Covid lockdowns and rising oil prices which have caused the worst cost-push inflation since the 1970s. However, short-term issues aside, there are also long-term challenges from the costs of Brexit, poor productivity growth and a decline in competitiveness with our major trading partners.

Video version

Main problems facing UK economy

Low productivity growth.

Since 2009, labour productivity has stagnated, falling considerably behind previous the UK’s trend growth. Poor productivity is a major factor behind the very limited growth in real GDP and a flatlining of average real wages. The UK is not the only country to face a slowdown in productivity growth, but the record of the UK is one of the lowest in the G20.

Reasons for low productivity growth include a lack of investment in new technology and a short-term approach from both business and the government. This unwillingness to invest in new technology has certainly been exacerbated by Covid disruptions, but the problem goes back to well before Covid and even before the Brexit vote.

Low economic growth

The OECD calculate the UK will record lowest growth in G20 (except Russia) in the coming year. With low growth, there is less capacity for real wage growth and it will hit government finances at a time when there is need for more public spending and a wish to reduce taxes.

Brexit. The UK has not only left the EU, but also the Single Market and the Customs Union. This is caused considerable disruption to EU trade, which in 2016 accounted for over 50% of UK trade. Firms exporting to Europe are faced with an increase in regulation, custom forms and charges for selling goods in the EU. The OBR claim the effects of Brexit will cut UK GDP by 4% – this is up to £100 bn in lost output and £40 bn less revenue to the Treasury (OBR). Another think tank Centre for European Reform (CER) models that the cost of Brexit is a shortfall in GDP of 5.2%.

The row over the NI Protocol has meant further problems with the EU’s relationship with the UK. In retaliation, the EU has not ratified Britain’s associate membership of Horizon science funding. Further barriers to trade may occur. It was hoped Brexit would lead to liberalising trade with non-EU countries. But, many trade deals are quite similar to the UK had within the EU anywhere, also there are definitely barriers to switching trade from your geographical neighbours to the other side of the globe. It makes sense to trade with those countries geographically the closest.

Labour shortages. Another impact of Brexit is the loss of migrant flows from the EU. This has led to considerable labour shortages in areas such as lorry drivers, fruit pickets, hospitality and transport. Labour shortages have contributed to queues at airports and fruit remaining unpicked. Recently the chief executive of EasyJet, Johan Lundgren claimed that 8,000 EU job applications were rejected because they could no longer work in the UK.

High tax burden to GDP ratio

Since 1993, we have seen a sharp rise in tax burden as a share of GDP. But, the problem is there isn’t a strong dividend of higher public sector investment. The rising tax burden highlights the weakness of tax revenues and the need for higher government spending on Covid bailouts and also from increased spending on health care and welfare. The concern is that pressures on government spending will continue as we face an ageing population, ongoing Covid treatments, and a cost of living crisis which puts pressure on social security spending.

Real Wage stagnation

Source: ONS

This shows there has been limited real income growth since 2009. In 2007/08 real median disposable income was £37,310. By 2020/21 that was only a very small increase of £37,622 or less than 1% growth over 13 years. It was hoped that Brexit labour shortages, would push up wages, and in some sectors, there have been sporadic increases in real wages. But, with productivity stagnant and a lack of bargaining power in many labour sectors, real wage growth has been patchy at best.

The problem of real wage growth has been exacerbated by the recent cost-push inflation, which has seen the highest inflation since the early 1980s. With inflation at over 9% in the summer of 2022. Whilst, inflation is a global problem, the UK still has one of the highest inflation rates in the OECD, despite weak economic growth.

A knock-on effect of poor real wage growth is that it has led to industrial action, with train staff going on strike and other sectors threatening to join a wave of industrial action.

Post-Brexit devaluation

Since the Brexit vote in 2016, the Pound has devalued 16%, causing an increase in the cost of imports and contributing to domestic inflation. Whilst a devaluation, in theory, makes exports more competitive, there is little sign of a prolonged boost in exports. A good example of the effect of devaluation on the cost of living is how the UK is paying more for petrol. In 2008, oil reached $144/barrel, but petrol peaked at 120p per litre. Today, the oil price is $111 but pump prices are just below 200p per litre. (There are other factors behind petrol prices, such as bigger profit margin at refineries, but devaluation is still a major factor and helps to explain the high prices) Furthermore, recent political uncertainty and a record current account deficit have further weakened the value of Sterling.

Current account deficit

The UK current account deficit hit a record 8.3% of GDP in Q1 2022. This was something of an anomaly with the higher price of raw materials contributing to a record trade deficit, but even discounting this quarter, the underlying trade deficit is a cause for concern, especially since the devaluation of the Pound has done little to improve the current account. The concern is that with Brexit, high inflation and low productivity growth, there is a continued lack of competitiveness with major trading partners. In the past, the UK has been able to finance the current account deficit by attracting capital flows (e.g. China, Russia, Middle East) buying UK assets and saving in UK banks. Post-Brexit, the UK has become less desirable as a destination for capital flows. If these capital flows do slow down, it will put further downward pressure on Sterling.

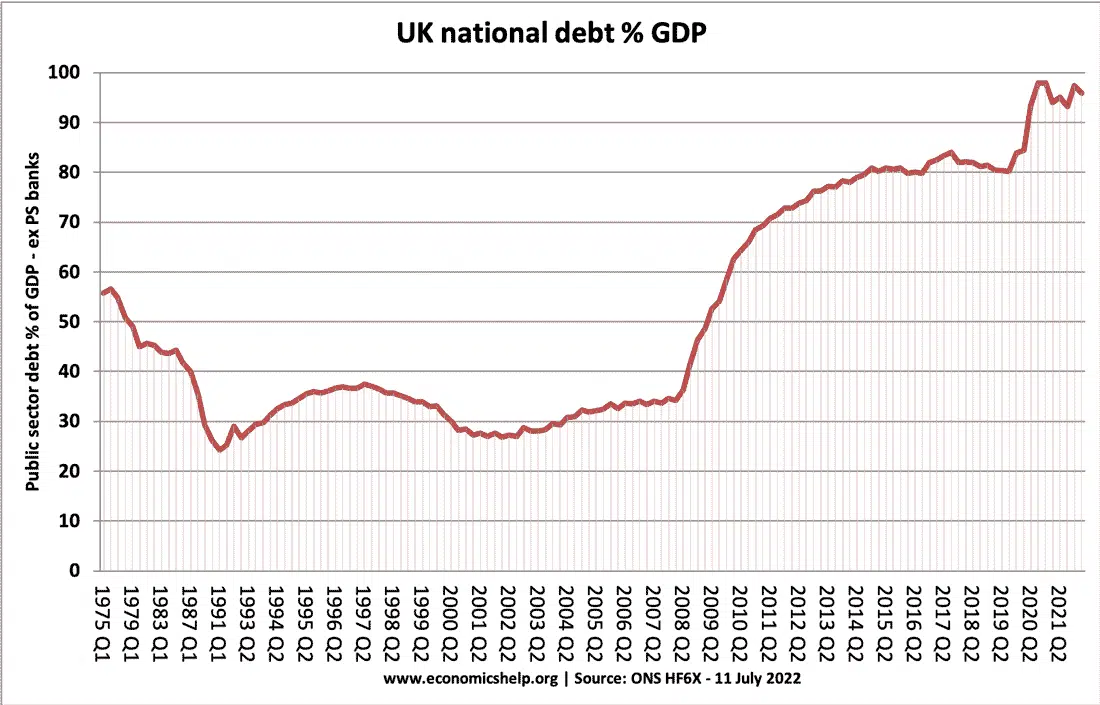

National debt

UK public sector debt has increased since 2008, and with demographic factors, the OBR predict a worse-case scenario of public sector debt of 320% of GDP within 50 years.

Brighter aspects of UK economy

It is worth pointing out, it is not all doom and gloom. It has also been a testing time for all economies around the world with the twin problems of Covid lockdowns, and cost-push inflation. Given these challenges, it is unsurprising that the UK economy faces many problems.

One success of the UK economy is the lowest rate of unemployment since the 1970s.

However, despite short-term challenges there are definitely concerns about the long-term future of the UK economy with a lack of skilled labour, and a lack of investment in both public sector infrastructure and business investment which will enable a boost to competitiveness and productivity.

Fascinating.

Am from an engineering background, associated with fabrication & machinery manufacture for all the major industries the UK was the originator of.

Having weathered the Heath/Gormley 3day week, the hyperinflationary Callaghan/Thatcher years and the boom/bust cycles thereafter, we started to encounter an annual derth of enquiries during the first quarter of each year in the nineties, resulting in having to work hand over fist the second half of each year just to feed the bankers.

By mid nineties, as we were just realising the permanence of the cycle, we got a call from a major customer telling us to ‘Get out. It’s all going East’.

So we did, and flogged everything to the Indonesians, paid everyone off fairly, and made a quiet exit, leaving the competition to fight over a steadily diminishing pie.

We later learned all the competition had succumbed, and now the Country hasn’t even got the Journeymen to train Apprentices. Sad. Politicians & Banksters make for no good.

Thanks for comment. Quite interesting.

I too saw the demise in heavy engineering in this case the printing machinery industry. However it is easy to fail to see the industrial successes driven by technology, our global ability and creative flexibility.

what do you have to say? Brian?!