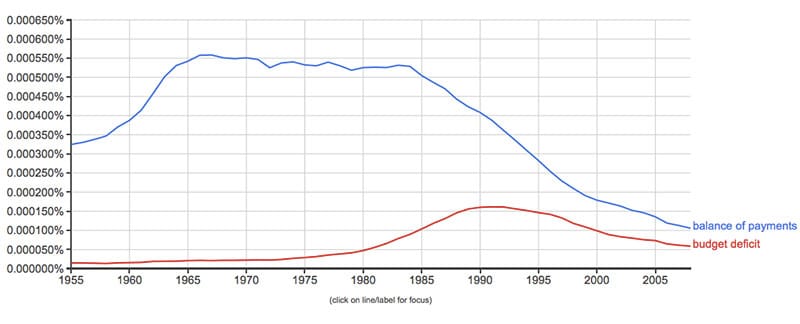

In the 1960s, a big political issue was the size of the deficit. Not the budget deficit, but the current account deficit on the balance of payments. In recent years, worries about the balance of payments (current account deficit) have slipped from the political and media agenda.

However, we have a very strong importance attached to reducing the deficit. It is taken for granted that a government who fails to balance the budget must be doing something very wrong. But, economic theory may take a different view. For example, the large deficit of 2009 a symptom of the deepest recession on record, and a necessary consequence of the fall in GDP. By making the deficit the priority, you tackle symptom more than underlying problem (of low growth)

Changing importance of deficits.

This is a useful tool from Google in examining how frequently these terms are mentioned in books.

Source: Google Books Ngram viewer. Frequency of terms mentioned in English books.

This obviously has its limitations, and it would be interesting to measure the number of newspaper headlines in recent years referencing – budget deficit, national debt)and balance of payments.

One point is that the political importance of economic issues can rise and fall depending on media / political trends. But, this political importance doesn’t necessarily translate into economic importance.

Should we worry about the current account balance of payments?

These days, the current account is buried in the business section, and little importance is attached to it. I would imagine quite a lot of people aren’t entirely sure what the current account on balance of payments actually is (including economic students…). Admittedly the terminology isn’t straight forward with people often mixing up balance of payments deficit when technically they mean current account deficit. (Just to confuse matters, the ‘trade deficit’ is a component of the current account.)

The current account comprises balance of trade in

- Goods

- Services

- Net investment incomes and transfers

In the 1960s, a big political issue was the desirability of the current account deficit. It was seen as a major problem when the current account deficit increased. There was a big campaign to ‘buy British’. In 1968, the PM launched a brief campaign I’m Backing Britain aimed at boosting the British economy. There was a similar Buy British campaign in 1931. These days, these campaigns seem rather quaint and outdated.

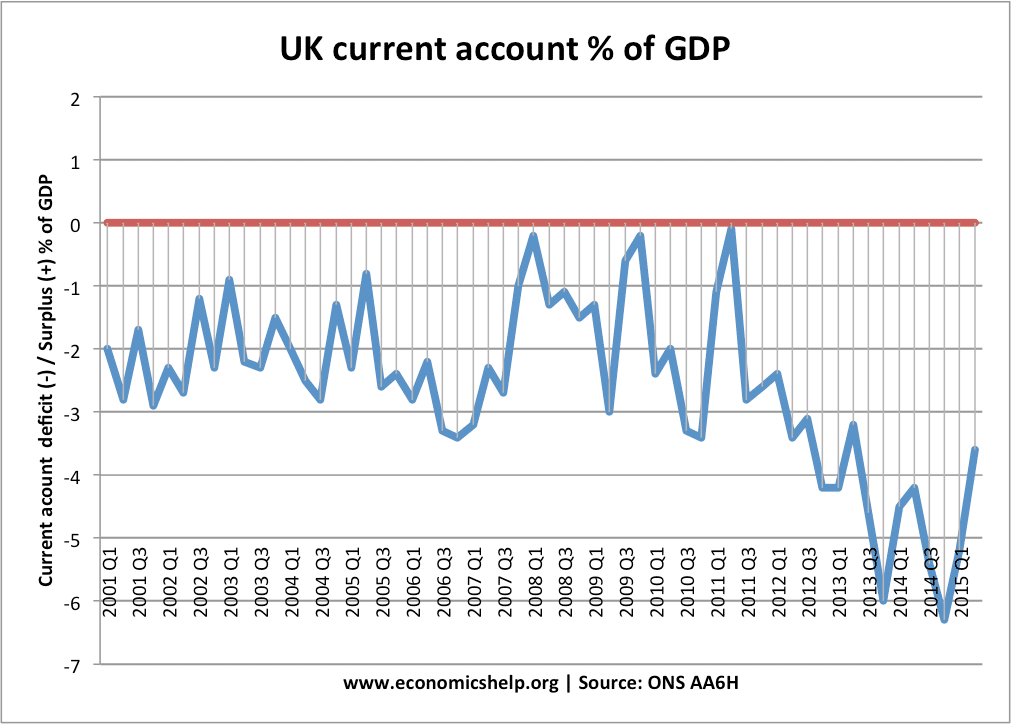

However, the Bank of England, Financial committee has placed the UK’s current account deficit at the top of the UK’s domestic concerns. At a time when the current account reached 6%, they stated:

That said, the current account deficit was large and could, in adverse circumstances, trigger a deterioration in market sentiment towards the United Kingdom. (Link)

Reasons to be concerned about a current account deficit include:

- Relies on financial flows to finance it. This can lead to the UK becoming reliant on financial flows and if they dry up, it could cause a sharp depreciation in the exchange rate.

- Implies the economy is lacking in competitiveness, with the UK unable to export sufficient goods and services to meet demand.

- Unbalanced nature of economic recovery – relying on consumer spending and low levels of saving and investment.

- A current account deficit is much more a problem when the economy is an official or unofficial currency peg – e.g. it was a major problem for Eurozone economies who can’t devalue.

However, it is a moot point about how much we should be worried about a current account deficit.

- Some countries have run large current account deficits for a long period without any adverse consequences.

- A current account deficit can be caused by economic growth being faster than other competitor countries, leading to more imports

- Financial flows, e.g. inward investment can help boost the economy (e.g. Chinese investment to help build nuclear power stations is increasing UK capital stock. Though this also shows that a current account deficit can lead to foreign investors ‘owning’ more UK assets, which some may seem as undesirable.)

- The UK has a full flexible exchange rate and so the exchange rate can act as a mechanism to deal with imbalances.

As usual whether a current account is a problem depends on

- How you finance the current account deficit (e.g. borrowing or attracting foreign investment)

- The magnitude of the deficit and when it occurs.

- The UK’s current account deficit of 5% of GDP is large by historical standards – especially given weak economic growth.

The UK current account has improved in recent months, and the recent depreciation in Pound Sterling may help improve even more.

But, the current account is still an important indicator. Perhaps the most important aspect of the deficit is the indication of the relative unbalanced nature of the economy. On the other hand, the current account deficit is partly related to the relative growth of the UK compared to even slower growth in Europe and the rest of the world.

More on – Should we worry about current account deficit?

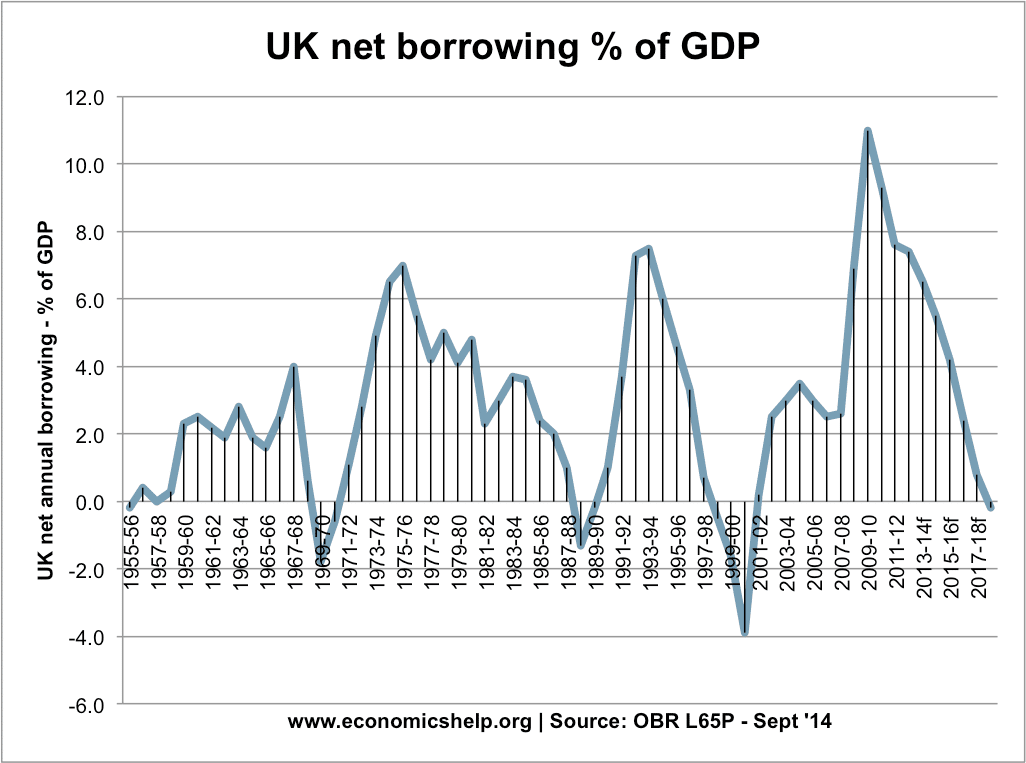

Should we worry about the budget deficit?

I’ve written a lot about whether we should be concerned about budget deficit so I won’t repeat myself here. But in summary

The budget deficit is given too much importance. And in a historical context, there is every reason to believe the current fetish with obsessing over deficit may be a passing trend. In the future people will look back and think why were the government so reluctant to finance public sector investment when interest rates were near zero.

See:

You explain that the emphasis on reducing the budget deficit is not logical particularly when borrowing rates are so low. Of course, it is only low for those countries deemed by the bond and money markets to be a relatively safe risk, which is jeopardised if the borrowing requirement is not seen to be controlled. The second question I have refers to the funding of the accumulated deficit, which has increased so greatly since 2008, in years to come when interest rates might be back at 3, 4 or 5%, rather than at the exceptionally low levels we have been experiencing. The chancellor plans (he says, and perhaps more in doubt now than before the last budget) to get into budget break even by the end of this parliament. That means an end to the annual borrowing requirement, but there is still the huge accumulated national debt to service, which has not been paid off. Your thoughts on this would be appreciated. Many thanks