Austerity can mean different things. See: definition of austerity. But, for this article, I will take austerity to mean a squeeze on public sector spending. In real terms (adjusted for inflation), government spending is rising. However, despite an overall rise in government spending, some departments have seen spending fall or at least shrink as a percent of GDP.

To end austerity, there are three possibilities:

- Increase taxes to enable more spending on public services

- Allow higher levels of government borrowing.

(If wages took a bigger share of GDP compared to company profit this may feel like an end to austerity for many workers who have seen falls in real wages in past decade)

Why has there been austerity?

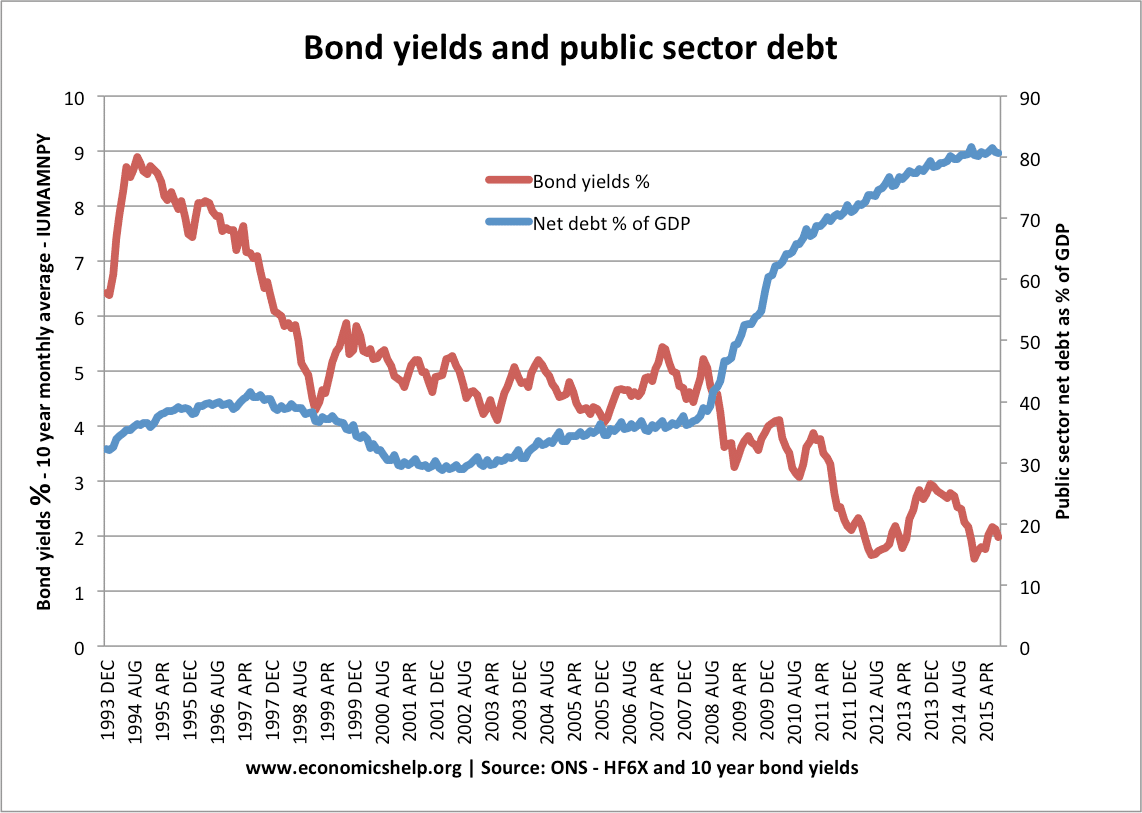

- High budget deficit. In the aftermath of 2008/09 recession, government borrowing rose rapidly. Post 2010, the UK government was committed to reducing level of government borrowing and (at least under G.Osborne were aiming to reducing share of government spending as % of GDP)

- Rise in spending commitments in certain areas. Despite the squeeze on spending, some departments have seen significant increases in real spending – for example, state pensions, housing benefit, health care. Therefore other departments, such as education, local government, public sector pay have had to bear a bigger brunt of spending cuts.

- Pressure on services. Despite rises in real spending (e.g. health care) spending has grown slower demand for services. This is because the NHS has seen growing demands from ageing population, rising population, increased medical costs. Therefore, despite rise in real spending, services feel under pressure and waiting lists have grown. Hence the feeling of ‘austerity’ without technical ‘cuts in real spending’ Health care is an example of how services can feel over-crowded and under-funded – despite an actual increase in real spending.

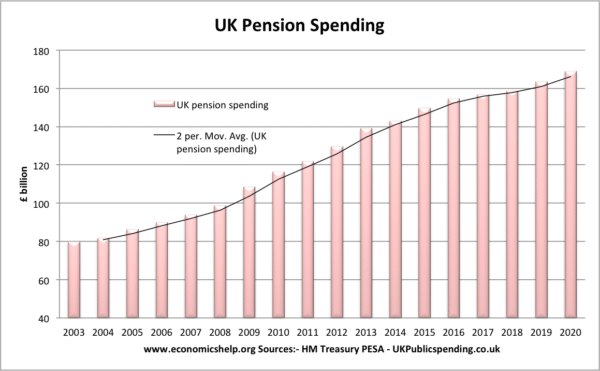

UK pension spending double from around £80bn in 2004 to £160bn in 2019. - Pension spending. One issue which helps to understand the current situation is government spending on pensions. With an ageing population and the ‘triple lock’ guarantee, pension spending is rising at a rapid rate compared to other government departments. It means with overall government spending limited, non-pension spending is being squeezed at a higher rate.

Can we end austerity?

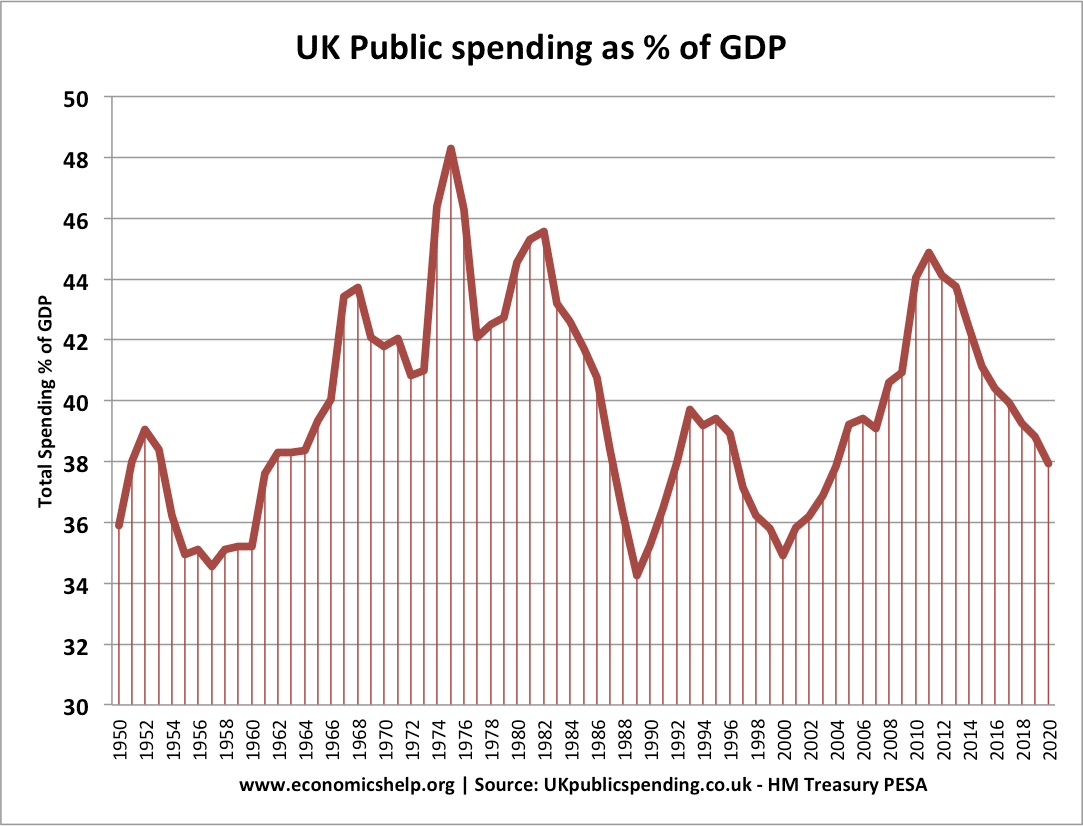

The government is projecting a fall in government spending to 38% of GDP (under Osborne the target was 35% of GDP). However, this is not a necessity, many Western European economies have government spending of 40-50% of GDP. Keeping government spending at 40% of GDP, though increasing the tax base, would enable more government spending.

Redistribution

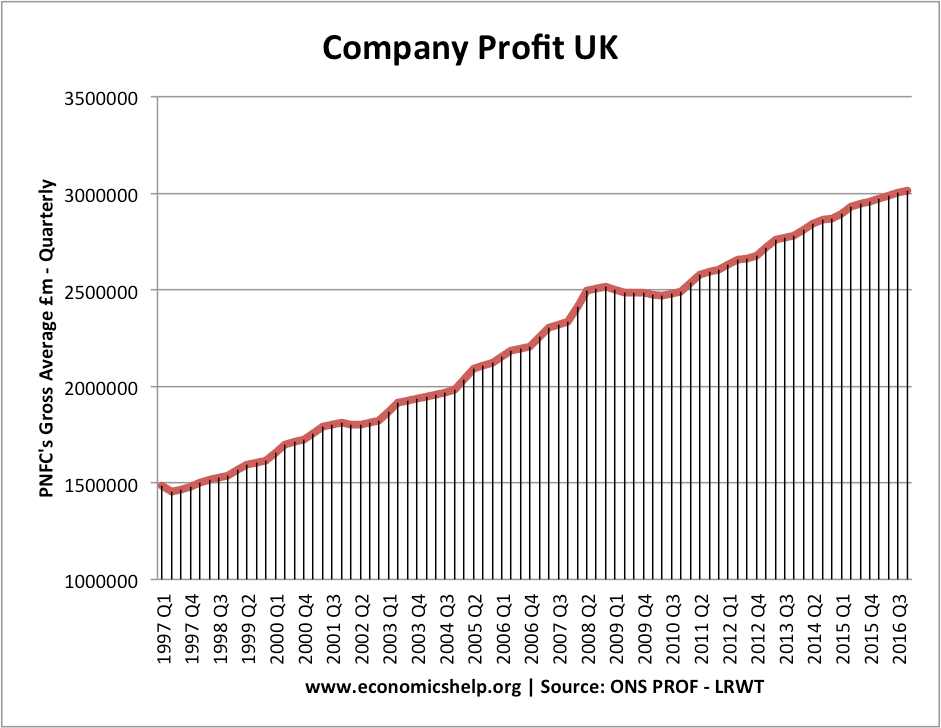

In 2016, gross profit by UK companies – £2,993 bn

One aspect of ending austerity is simply redistributing resources in the economy. Since 2010, the share of GDP to education, health care and public sector pay has fallen. Company profit, income from renting property spending on pensions have increased. In this sense, we can afford to ‘end austerity’ – it is a matter of redistributing GDP. For example, higher corporation tax (reversing recent tax cuts) would enable more government tax revenue for spending on these sectors which have been squeezed.

Critics may argue higher corporation tax may encourage firms to find ways to avoid paying tax (e.g. setting up abroad). This is certainly a possibility but given the rise in corporate profit in recent years, increasing corporation tax is, at least one way, to try and redistribute national income.

When people say we can’t afford to end austerity, what they really mean is they are unwilling to contemplate redistributing the economic pie.

Government Borrowing

Government borrowing is a tricky issue because the amount a government can borrow is not a simple science. For example, the idea the UK could quickly become Greece is misleading. Unlike Greece, the UK has ability to print its own currency and so is not subject to the same liquidity constraints. In 2011/12 austerity (cutting real public spending) arguably undermined economic recovery, and was in large part self-defeating. At least from a Keynesian perspective, the best way to reduce debt to GDP is promote economic growth (i.e 1950s/60s debt reduction), rather than risk depressing demand.

The situation in 2017 is not as clear as 2010/11. Five years after a recession, in theory, we should be seeing strong economic growth and this would be the optimal time to reduce the budget deficit and reduce the debt to GDP ratio. However, economic growth remains sluggish – investment and now consumer spending are slowing down. With base rates still stuck close to zero, excessive tightening of fiscal policy would be a major drag on growth.

With very low borrowing costs indicating strong demand for buying government bonds, the best way to improve the debt to GDP situation is still to concentrate on returning to more normal rates of economic growth. It certainly makes sense to borrow to fund capital investment in the UK’s infrastructure – especially given how long structural inflation is.

In economic terms there is probably more flexibility on debt than in political terms.

Overall

The UK can afford to increase share of GDP in sectors which have struggled in the past decade. Health, education and public sector pay have all seen a fall in the share of GDP. By contrast, rent, company profit have done relatively well.

There are limits to how much you can redistribute through tax and spending. But, there is no logic we have to keep reducing the share of government spending to GDP. Furthermore, easing austerity could help the macro-economic performance. Rising real wages would strengthen demand, and capital investment would help both productive capacity and the demand side. All this creates a positive multiplier effect of higher public spending.

Ending austerity is by no means a panacea for the UK economy which has serious challenges- i.e. weak manufacturing, Brexit uncertainty, and low productivity growth, but the country can afford to increase public sector pay and spending on health care – if the political will is there.

Related

Interesting analysis, with which I broadly agree.

However, it would be good to get some idea of the scale.

Taking Osborne-like austery , which *should* have ended the era of deficits in 2015, but didn’t, at one end. And Corbyn-like debt explosion at the other, with £100bns more of spending. One suspects reality is somewhere in the middle, but has the current government, which is broadly spending in line with Ed Balls’ putative 2015 budget, rather than George Osborne’s, hit the target, or aimed too low, or too high?

At what level of increased real spending does the benefit to the economy outweigh the cost, or vice versa?

One fears that the current position may actually be pretty much as good as it can get – with only incremental gains remaining from increasing the national debt, particularly as it seems we can *never* spend enough on the NHS and pensions to truly meet the desires of the population, but it would be nice to know some of the maths, and whether this gut feeling is over-pessimistic or not.

We are back to conflicts between macroeconomic objectives. Your analysis highlights this very clearly.

The pressure to end austerity will increase as inflation rises. However, pressure for pay increases has escalated at householders and unions see increasing splits within government. Is this opportunistic? You only have to ask the people directly affected. In the meantime failing public services have also create a demand for increase in spending on essential services, both capital and operational. The Grenfell disaster has highlighted the problem while it could be argued that the local authority took shelter by using government policy constraints.

We are living n most interesting times. Leading members of the Cabinet have made favourable comments to support pay increase. One wonders whether they had done a complete and objective analysis or whether they were just using this furore as an opportunity to have a go at the Chancellor .

I feel we should be encompassing a global perspective within the UKs thinking. It seems obvious to me as a man in the street, that we need to be working towards a more equitable global society. It is essential that we all stop thinking of our economies in isolation. There is a need for profit but not excessive profit and greed. As a species we must reshape our thinking, values and ethics. We are having to learn, due to fuel prices that we have to make do with less. This is just the start of processes that are coming our way, partly due to climate change, partly global echoes from the controlling influence of stock market trading all sorts of natural resources to make money [greed]. We have to learn to share … The world still has enough to house, feed and clothe everyone everyone, but materialism and greed are still preventing this. Nature will eventually ‘teach’ us the error of our ways if we aren’t prepared to change. There are no pockets in a shroud …