Economics is concerned with the optimal distribution of scarce resources within society. For example, economics is concerned with how individual decisions like how firms produce goods and which goods people buy. An important element in economics is concerned with the extent to which governments can intervene in the economy to improve economic welfare. Economics is also concerned with wider issues such as economic growth and unemployment – issues that affect the whole of society.

Supply and Demand

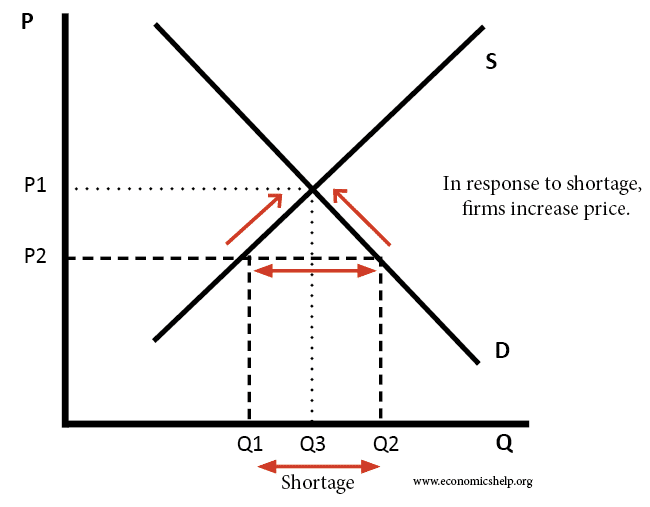

The most basic model in economics concerns how the price and quantity of goods and services is determined. If there was a shortage of a good – queues of people forming, then there is an incentive for firms to increase price. This increase in price reduces demand and encourages supply. Prices change until markets reach equilibrium. Adam Smith referred to the ‘invisible hand’ of the market for explaining how prices adjust.

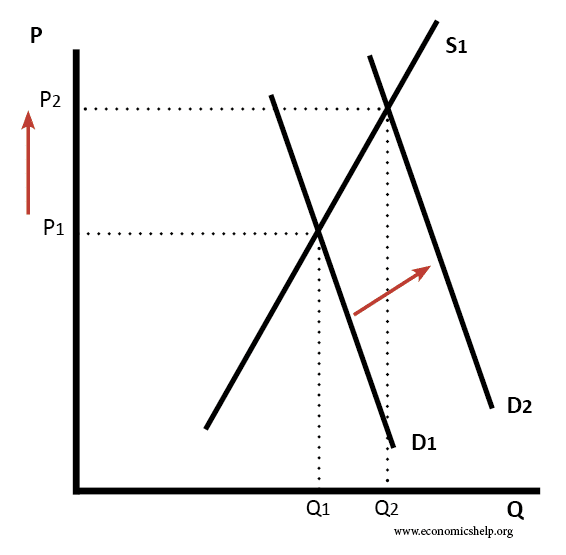

If demand for a good rose, we observe that this usually leads to a higher price. This higher price, in turn, encourages firms to supply more. This simple model helps explain a whole variety of different issues and topics. For example, we can use supply and demand to explain wage differentials. A lawyer can command a high wage because the number of qualified lawyers is very low. Cleaners tend to get lower wages because there are many more people with necessary qualifications.

Behaviour

Economics is concerned with decisions that agents (firms and consumers) make. For example, classical economics generally assumes that people wish to maximise their well-being; i.e. we assume firms wish to maximise profits and consumers wish to maximise their utility (happiness)

However, the real world is more complicated. Not all firms wish to maximise profits; they may seek to maximise market share or pursue other social/environmental objectives. Also, people may not be rational but get caught up in irrational booms and busts (e.g. stock market booms, housing booms, dot com bubbles). Therefore there is a branch of economics known as behavioural economics. In recent years, this branch of economics has increased (Richard Thaler was awarded the Nobel Prize in Economics (2017) for his work on behavioural economics, which included work on

Dual-system theory – the idea we have two decision making elements. One is impulsive, the other is more rational, cognitive and analytical. Similar to ‘hot-cold’ states.

Mental accounting – how individuals separate their budget into different accounts, limiting spending on particular aspects of expenditure.

Prospect theory – the idea we suffer comparatively more from losses than gains. It also places emphasis on a relative starting point. We judge utility from our loss/gain – rather than our finishing point.

Macro Economics

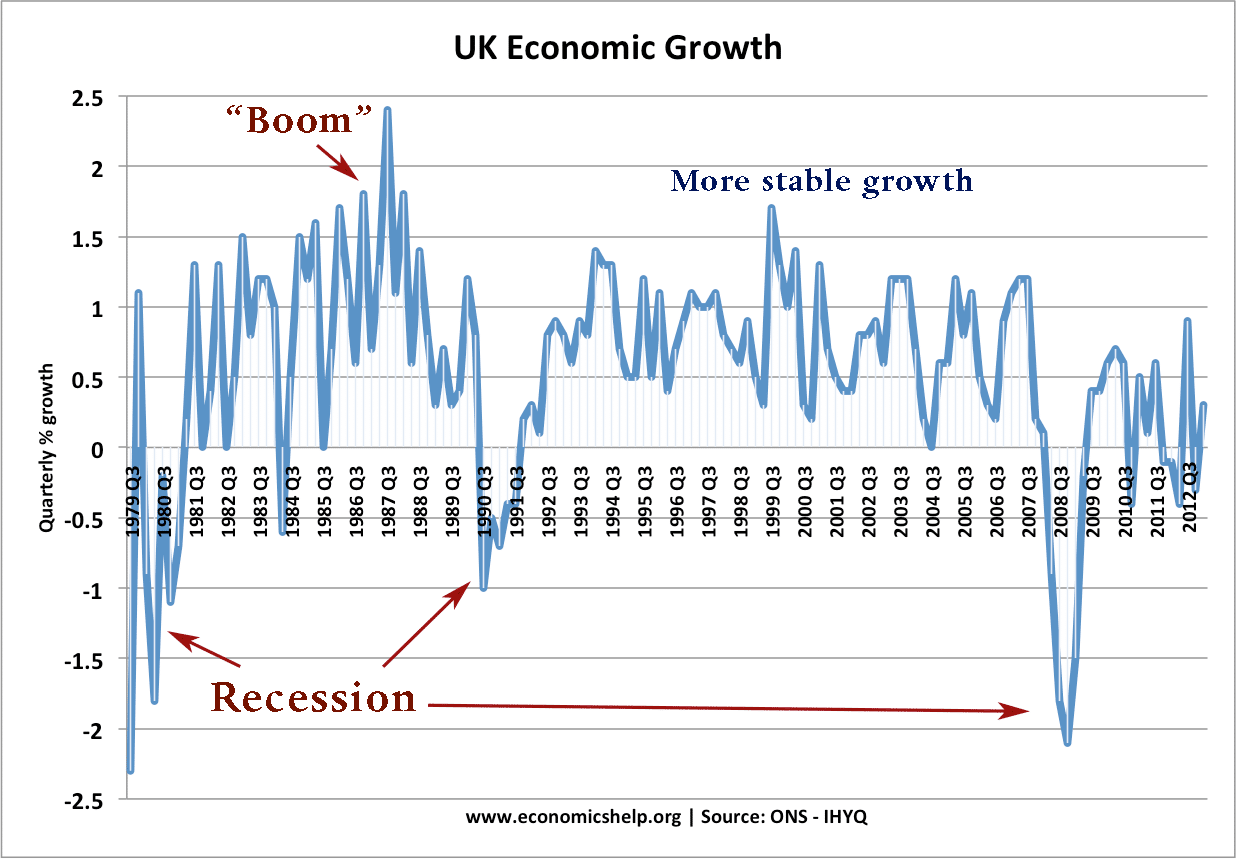

Macroeconomics is a term relating to nationwide economic problems. For example, the rate of inflation in a country measures the average increase in prices. Higher inflation affects both savers and borrowers and can influence living standards. Economic growth is another key factor that can determine living standards. Higher economic growth can lead to improved living standards and lower rates of unemployment. A recession (negative economic growth) can lead to the opposite. Macroeconomics

See: differences between macro and microeconomics

Government Intervention in the Economy

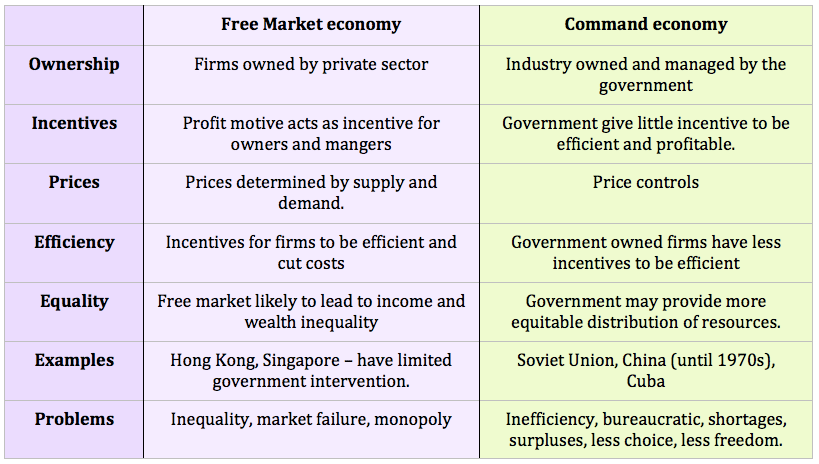

A continual debate in economics is the extent to which governments intervene in the economy. On the one hand, free-market economists argue government intervention should be very limited (e.g. the protection of private property, national defence). The argument of free market economics is that governments tend to be inefficient, they don’t have the same incentives to produce what people want and need. If you leave it to markets, the ‘invisible hand’ automatically responds to changes in demand to provide goods that people want.

On the other hand, other economists argue that the free market actually creates many problems. In a free market, we may have monopolies, inequality, under-provision of important public services. Therefore to improve economic welfare, there is a necessity for governments to raise tax and spend on public goods not provided by the free market. Markets vs Government Intervention

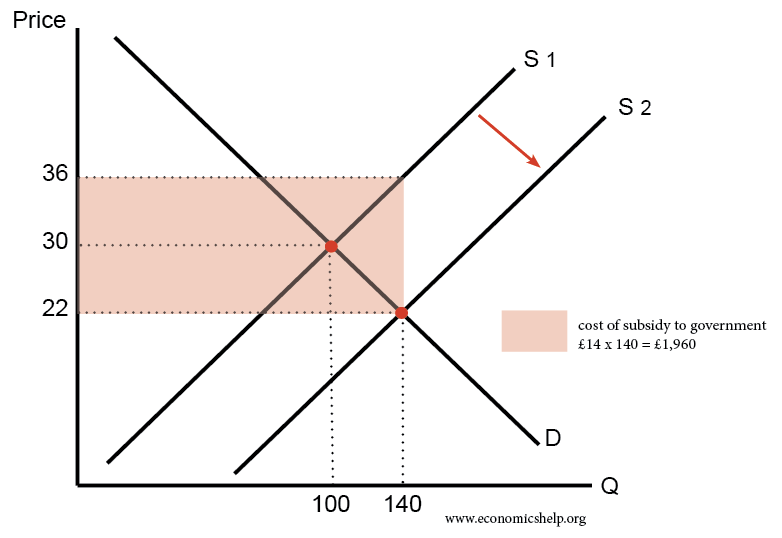

Goods with positive externalities (e.g. trains which reduce pollution and congestion) may be under-consumed in a free market. A government can raise taxes and subsidise these positive externalities.

A big issue is to what extent should a government intervene in the economy?

What is the goal of economics?

Classical economic theory assumes the goal of economics is to maximise utility (satisfaction of material wants). This emerged from the philosophy of utilitarianism. It is an assumption firms seek to maximise profits and consumers seek to maximise consumption.

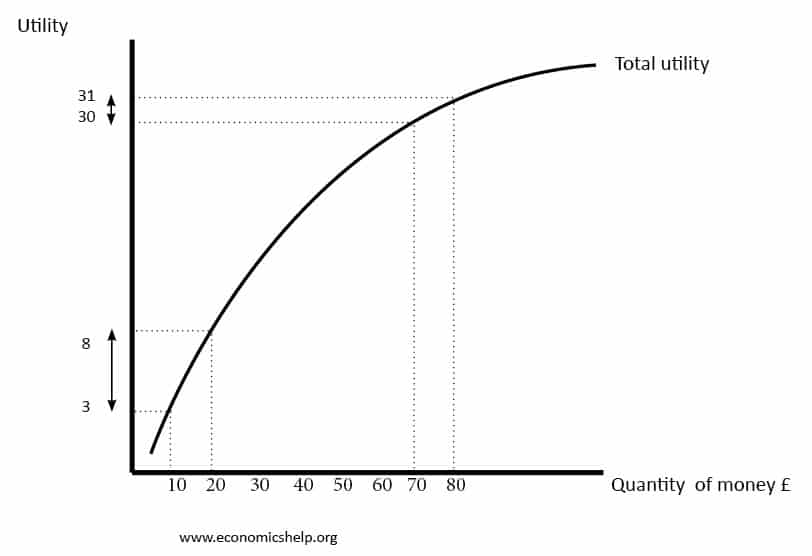

However, in recent years, more economists have challenged whether economic welfare is the same as maximising production and consumption. For example, with a diminishing marginal utility of wealth, we may get more happiness from increasing leisure time and looking after the environment

DIminishing returns to wealth/income

Happiness economics looks at ways to increase happiness – rather than net welfare.

Economic Systems

To some extent, all major economies have converged on a similar model which may be termed a ‘mixed economy’. This is a combination of free markets (no government intervention) and state provision of goods. The old Soviet Union pursued a ‘command economy’ Communist, where the government decided what to produce, how to produce and for whom.

The opposite to a Command economy is a pure free market, where there is no government intervention. Within the two are mixed economies. The extent of government intervention in an economy varies significantly from 17% of GDP (Hong Kong) to over 50% in Scandinavian countries like Norway and Sweden.

Until we start tceahing our yewts the benefits of Capitalism and what our Republic stands for–we are doomed to have 53% of liberals who think favorably of Socialism.You cannot vote for the right people if you don't even understand what the right policies are.Did I mention lately for the first time in my adult life I am no longer proud to be a citizen of this "mostly free" government?

We could start by teaching our youths how to spell. We wouldn’t want the youth of today to get mistaken for newts.

its good one on point keep it up

IT IS INDEED