Readers Question: Between markets and concerted central banks intervention, e.g in currency and shares, which forces are likely to prevail?

Market forces can be very strong in influencing the value of currency or shares (or bond yields). Governments and Central Banks can try and influence the value of the currency and bond yields. In certain circumstances, the government can ‘buck the market’. But, if economic fundamentals really point to a weakening currency, government intervention will typically fail in the face of market forces.

There are times when concerted Central Bank intervention can protect the target level of currency. E.g. if Central Banks wished to prevent an appreciation in the Swiss Franc, they could agree to sell Franc reserves and buy Euros. The Swiss Central Bank should be able to prevent an appreciation of Swiss Franc on its own by increasing the supply of Francs and buying foreign exchange reserves. If markets see the Central Bank is determined to keep the level of Swiss France low, they may give up trying to speculate on the Swiss Franc increasing.

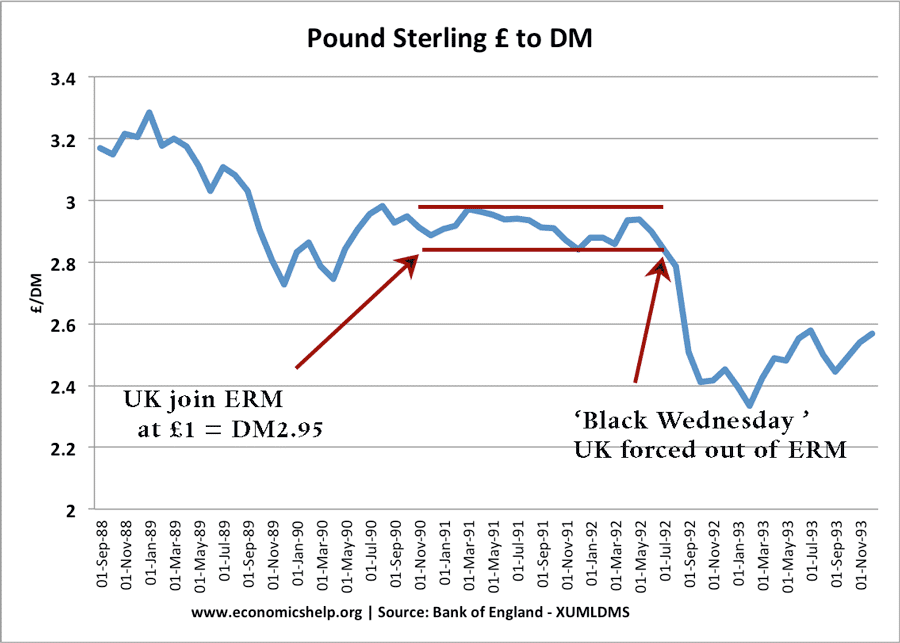

Example of Pound Sterling in ERM 1990 – 92

It can be more difficult to prevent a devaluation in the value of a currency. The best example is the UK in 1992. The UK was in the ERM and markets felt the value of the pound was too high (the UK was in recession with high interest rates to keep Pound strong). Therefore, markets were selling pounds – driving the value lower. The government was committed to keeping pound high. Therefore the government:

- Used foreign currency reserves to buy Pound Sterling

- Increased interest rates to attract hot money flows (savings into UK).

However, markets sensed:

- The UK was going to run out of foreign currency reserves

- High interest rates and high value of pound were damaging for the UK because they were in recession. In a recession, markets felt high-interest rates and high value of pound were unsustainable.

Therefore the government action failed to switch market sentiment. People kept selling pounds (investors like George Soros made billions.

The UK was eventually forced out of the ERM, interest rates fell, the pound fell (and the economy recovered)

Some in the UK government claimed that they just needed more help from other Central Banks in Europe. If other central banks had intervened and bought more pounds, the combined Central Bank intervention may have overcome market forces.

However, I’m sceptical. Government foreign currency reserves are significant but are still only a minority share of total foreign currency traded. It made no sense for the pound to be so high. The market sensed it and they’re selling power was much greater than the buying power of European Central Banks.

When Governments Can Prevent Market Forces

In the case of Switzerland, Central Bank intervention works because it makes economic sense to prevent an overvaluation in the Franc. The UK case of 1992 was different, economic fundamentals (UK in recession) suggested the Pound should devalue. The government were fighting a losing battle.

Can Central Bank Intervention avoid debt default?

An interesting question is can Central Bank and government intervention help avoid government debt default?

In the case of Greece, the government looks bankrupt. There is a structural deficit that the government seems incapable of dealing with. Therefore, it would require massive intervention from other governments to basically buy Greek debt to avoid default.

In the case of other countries like Italy. Prospects are better. The current primary budget deficit is relatively low. Where Central banks can really help is in the case of a liquidity shortage. (this is basically a short term issue of not getting enough buyers of debt at a particular point in time). By buying government debt at key moments of liquidity shortages, the Central Bank creates greater confidence that there will be no liquidity shortages. This encourages markets to buy more government debt.

Countries in the Eurozone have found that the absence of this Central Bank intervention to buy debt during liquidity shortages has made markets more nervous. Which explains why Eurozone countries like Ireland and Italy have much seen increases in bond yields compared to UK. Therefore, it is has been harder to prevent rising bond yields

The point is that Central bank intervention can help prevent temporary liquidity shortages. However, it cannot solve fundamental structural deficits.

Related

2 thoughts on “Question: can governments overcome market forces on currency markets?”

Comments are closed.