At the start of the academic year, I always feel a little pressure to justify the study of economics. Students come up asking things like, should they do economics or history? It’s hard to know what to say, but to get people excited about economics it’s good to try and think how economics can be applied in everyday life. Some of this is just common sense, but economics can help put a theory behind our everyday actions.

Buying goods which give the highest satisfaction for the price

This is common sense, but in economics, we give it the term of marginal utility theory. The idea is that a rational person will be evaluating how much utility (satisfaction) goods and services give him compared to the price. To maximise your overall welfare, you will consume a quantity of goods where total utility is maximised given your budget. For example, is it worth paying extra charges by airlines, such as paying for more leg-room? Or pay to get priority boarding? Economics suggests we need to evaluate the marginal benefit of these services compared to the marginal cost. See: Extra charges by airlines

Sunk cost fallacy

A sunk cost is an irretrievable cost, something we cannot get back. For example, suppose we sign up for a gym membership at $40 a month for a whole year. We are committed to paying $480, whether we go or not. If we are feeling unwell, should we go to the gym to get our money’s worth or should we write off the sunk cost and maximise our marginal utility for that particular day? See: sunk cost fallacy

Opportunity Cost

The first lesson of economics is the issue of scarcity and limited resources. If we use our limited budget for buying one type of good (food), there is an opportunity cost – we cannot spend that money on other goods such as entertainment. Opportunity cost is an intrinsic aspect of most economic choices. We may like the idea of lower income tax, but there will be an opportunity cost – in this case, less government revenue to spend on health care and education.

There’s no such thing as free parking

Another example of opportunity cost – no one likes to pay for parking, but would we be better off if parking was free? Most likely not. If parking was free, demand might be greater than supply causing people to waste time driving around looking for a parking spot. Free parking would also encourage people to drive into city centres rather than use more environmentally friendly forms of transport. The result would be that free parking would increase congestion; therefore although we would pay less for parking, we would face other indirect costs. (time wasted)

Behavioural economics and bias

Traditional economic theory assumes that man is rational. However, the work of behavioural economics suggests we can be prone to bias and irrational behaviour. For example, we may be prone to a present bias where we overvalue pleasure in the short-term and ignore long-term implications. For example, consuming demerit goods like alcohol or not saving sufficiently for retirement. The insight of present bias suggests we make decisions our future self would not make. If we become aware of these bias and irrational behaviour, then we can make better decisions which improve our long-term welfare.

Irrational exuberance

Another issue in behavioural economics is that of irrational exuberance or when we get carried away by an asset bubble. Can we be sure we will not get carried away by a boom and bubble? History suggests that many investors are over-optimistic about their ability to leave the market at the optimal time and can feel that this time is different.

On the other hand

In economics, there’s always another way of looking at the world. Borrowing is bad, except when it isn’t. Nothing is black and white in economics; it depends. For example, government borrowing to finance pensions for an ageing population can lead to an unsustainable rise in government debt. However, government borrowing during a recession can help the economy recover.

Diminishing returns

If we like chocolate cake, why do we not eat three per day? The reason is diminishing returns. The first chocolate cake may give us 10/10. The second cake 3/10. The third cake may make us sick and give a negative utility. People may have different opinions about when diminishing returns set in. Some students may feel this is after the second pint, other students only after considerably more. There are also diminishing returns to money. That is why we don’t spend all our time working – extra money gives increasingly less satisfaction and reduces leisure time

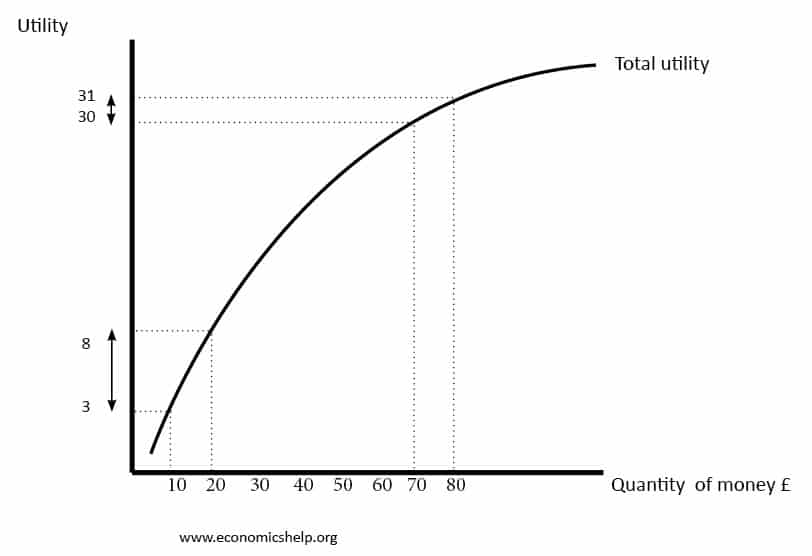

DIminishing returns to wealth/income

A similar concept is that of diminishing returns to wealth and income. Does an extra $100 give us more utility? Yes, but it depends on our current income. If we have a very low salary, the extra $100 will make a big difference. But, if we earn $100,000 a year, we may not notice that extra $100 a year. The importance of this is for choosing the right balance between work and leisure. What is the value in working a long working week, if the extra money earnt has a limited marginal utility?

Externalities

Economics may feel we are promoting selfish ends – firms maximise profits, consumers maximise their personal utility. Adam Smith claimed pursuing selfish goals ended up in improving the greater good. But, in economics, we also try to consider the impact of our actions on other people. If a firm produces chemicals, it may make a profit, but cause an external cost of pollution. To ignore this external cost would be to create an inefficient outcome. We should make the firm pay the cost of its pollution so that it has the incentive to minimise or halt external costs. Externalities are everywhere. Even your decision to study economics could have positive externalities in the future. For example, you could end up being an economics teacher helping others learn all about economics.

Public goods not provided by the free market.

The free market has many advantages. Private firms tend to be more efficient, innovative and respond to consumer preferences. However, many goods and services would either be not provided or under-provided in a free market. Public goods like street lighting and law and order. Also, public services like health care and education would be provided in insufficient quantities. Therefore, to optimise social welfare there is a need for government intervention through taxes and direct public provision. We may dislike taxes, but we would dislike not being able to see a doctor.

Should I worry about automation and new technology?

There are concerns that new technology and automation will lead to job losses and some people losing out. If our job is threatened by new technology is the fear justified? Economic analysis suggests there it is a fallacy that new technology leads to permanent job losses. This is known as the Luddite Fallacy – though some jobs are lost, new ones are created. Automation and new technology are not guaranteed to make everyone better off – especially in the short term. See: Pros and cons of automation

Macroeconomics affects everyone

Everyone is affected in some way by macroeconomic issues such as inflation and unemployment. Inflation can reduce the value of your savings. If you keep cash under your bed during high inflation, you’d be better off trying to buy gold or some physical assets. Mass unemployment can cause society to fragment, therefore there is a need to adopt policies to try and reduce unemployment.

Life-cycle hypothesis

The Life Cycle Hypothesis states that to maximise lifetime utility, we should try to smooth our consumption patterns over the course of our life. It is not good to have substantial income when we are old and unable to move. Spending some money in our student years will give greater overall utility. This justifies taking out a student loan to pay back when we are working and then saving for a pension in our retirement.

Examples of economics in everyday life

- Is the price of Starbucks a rip-off?

- Is it rational to put money in an honesty box?

- How will you be affected by a devaluation of the Pound?

- How will you be affected by low-interest rates?

- How will you be affected by a recession?

Related

Last updated: 10th November 2021, Tejvan Pettinger, www.economicshelp.org, Oxford, UK

Very nice article especially to beginners (students). It’s easily understandable.

interesting

Great, i like economics, its interesting and fascinating.

THEN BATTER THINKS TO DEVLOPMENT A APPLICATION ON PREFROM A APPLICATION TO ECONOMICALS THINKS IN HUMAN ON UNDER CONNECTION IN HUMAN THINKS

concepts are very clear and nite becouse initially importance of economics..

Very easily explained.Make more like these.

make a poem about economics using many different economic topics and email it back to me please its for an economics project !!!

Being an economics student ,it is Very informative for me ….

Very comprehensive thoughts. The application of both micro and macro economics in daily life is lot yet people don’t realize. For example , when you go to mall to purchase your daily needs or other products, you simply calculate opportunity cost between two products. And as a rationale consumer select one product over other who’s marginal value is more.

Soon meet you with more such concepts

I like this. I really helps me as I have to constantly explain these concepts everyday. It’s just nice to know others feel the same.

Quote inspiring. Our everyday application of Economics concepts are enormously. We always use public roads ,streetlights, sewer lines and public security. We also complain about those not using them well without knowing that once these goods and services are provides, we can not stop others from using it, neither can the consumption by others reduce the quantity available for our consumption.