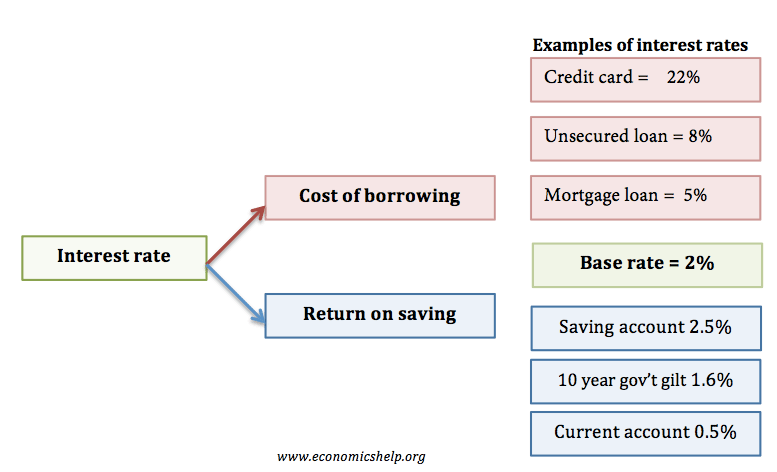

Interest rates are the cost of borrowing money. Interest rates are normally expressed as a % of the total borrowed, e.g. for a 30-year mortgage, a bank may charge 5% interest per year.

Interest rates also show the return received on saving money in the bank or from an asset like a government bond.

Different types of interest rates

Central Bank Base Rate

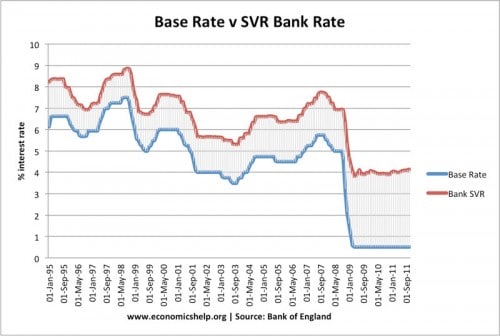

The base rate is the interest rate which the Central Bank lends money to the commercial banks.

This base rate is the most important interest rate because it tends to influence all the other interest rates in the economy.

If the Central Bank increases the base rate. Commercial banks find it more expensive to borrow from the Central Bank. Therefore, they pass this onto their consumers.

Indirectly, the Central Bank rate affects all interest rates in the economy – from mortgage rates to the saving rate you get in a savings account

Commercial banks are free to set their own interest rates, but it tends to be strongly influenced by the Central Bank base rate. If they find it more expensive to borrow from the Central Bank, they tend to increase their commercial rates.

This shows that banks tend to follow the Central Bank base rate, but from 2009, there was a bigger gap between bank SVR and Base rate. Commercial banks didn’t pass the full base rate cut onto their customers.

Standard Variable Rate (SVR). This is the most common lending rate for the bank. Sometimes, banks may give discounts to consumers from their SVR, but the SVR will be the main lending rate for a bank.

Mortgage Interest Rates

Mortgages are a type of loan secured against the value of a house. Banks are willing to lend large sums at relatively low interest because if the mortgage holder defaults, the bank can legally reclaim the house and secure the value of its loan.

Fixed Mortgage Rates. Banks may offer a fixed mortgage rate (e.g. 2 years, 5 years, 10 years) this gives mortgage holders greater security over the cost of monthly mortgage payments.

Tracker Mortgage Rates. Banks may offer a mortgage where the mortgage rate follows the Central Bank base rate. If the Central Bank reduce base rates to 0.5%, the mortgage rate will fall to a similar level.

Variable Mortgage Rate. A mortgage rate which is determined by the banks SVR.

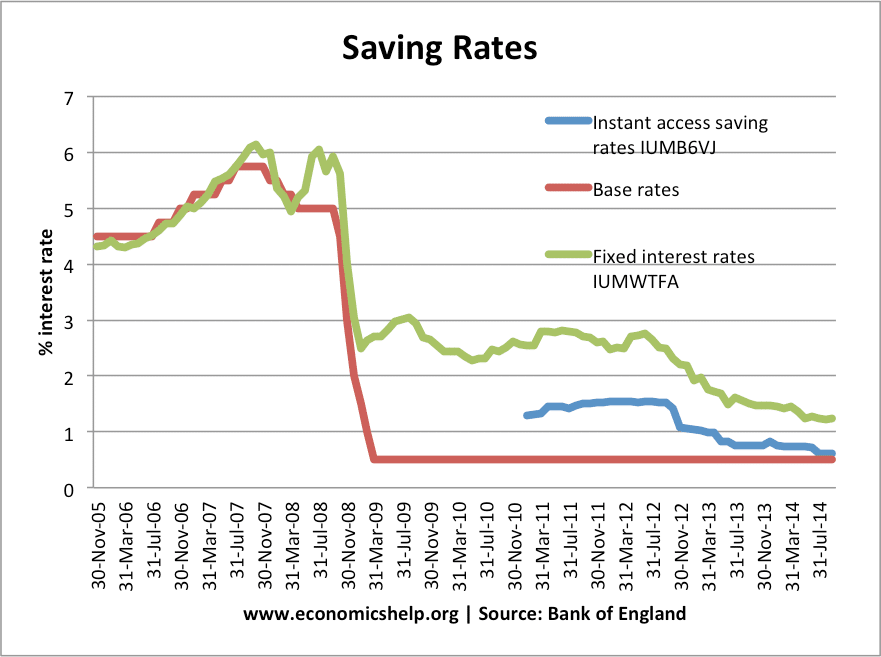

Saving Rates

Interest Rate on Current account (perhaps – 0.5%) . Many banks may pay savers very little interest for their savings in a current account. This is because savers can have instant access to their savings so the bank needs to keep more cash in reserve and these cash deposits are not very profitable for the bank.

Interest rate on savings account (perhaps 2-4%.) For saving accounts, banks can pay a higher rate of interest. This is because money is less likely to be withdrawn. The bank may even place limits on access to funds (e.g. you have to give 7-day notice) This means the money can be more profitable for banks as they use it to lend to other people.

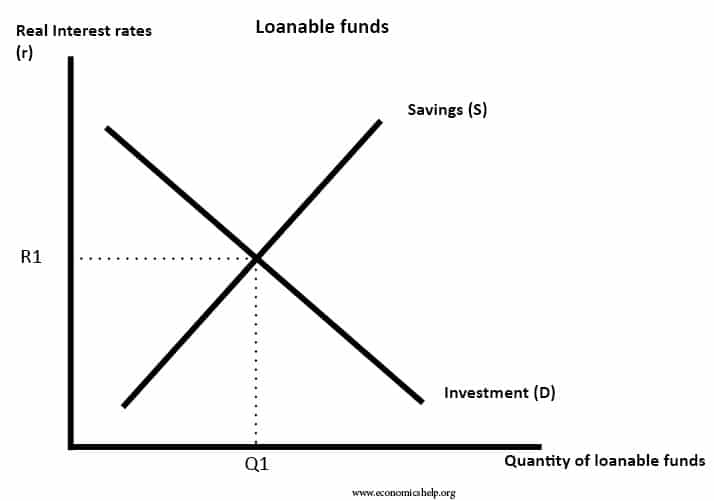

Loanable Funds Theory

The loanable funds theory states that interest rates will be determined by the supply and demand for funds. If people save more, there will be more funds for investment, this will reduce interest rates. If demand for borrowing increases, this will push up the cost of borrowing.

The equilibrium interest rate is at R1 – when demand equals supply for loanable funds. In the credit crunch (2008-11), a shortage of funds pushed up bank rates.

Real Interest Rate

The real interest rate shows the nominal interest rate – inflation. E.g. if interest rates are 5%, and the inflation rate 3%, the real interest rate is 2%. It means savers will see an increase in the value of their savings, despite inflation of 3%. See also: Real Interest Rates

Negative Real Interest Rate

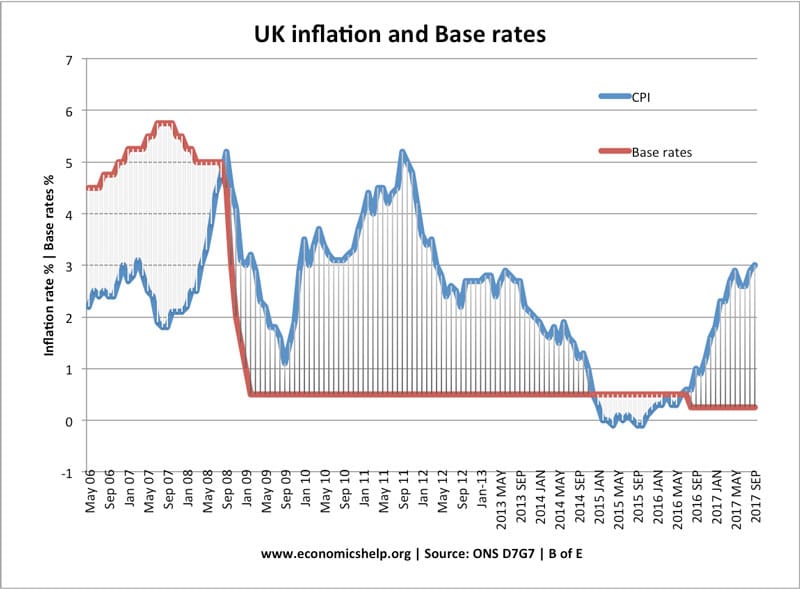

A negative real interest rate means that the nominal interest rate is less than the inflation rate. e.g. if interest rates are 5%, but inflation is 6%, then there is a negative real interest rate of -1%. It means savers see the value of their money fall by more than the interest payments they get. In 2011, inflation was 5%, whilst base rates were 0.5%. See: Negative Real interest rate

Bond Yields

Bond yields show the interest payments that someone will get from buying a bond, such as UK government bond.

E.g. if the 10-year bond yield on a government bond is 3%, it means someone who holds a £1,000 bond will be getting £30 interest a year.

The annualised percentage rate of interest – APR – represents the annual cost of taking out a loan. There is not a simple correlation between a monthly rate and the annual rate. For example, for a loan with no repayments, if the monthly rate is 1%, the APR will not be 12%, but about 13.5%. This is because the interest is compounded and you end up paying interest on the interest accrued to the loan. Banks and building societies are legally obliged to tell customers of their APR as monthly rates can be misleading.

this is great l used it on my presentation ….the information is clear and straight

I get good lessons and informations clear and possible lessons from this website

Thanks.