In recent years, I’ve frequently stated that fiscal consolidation can actually increase debt levels. It may seem a paradox because fiscal consolidation aims to reduce the budget deficit by increasing taxes and cutting spending. Yet, under circumstances, policies to reduce debt levels can actually cause a rise in debt to GDP. This seems to be a particular problem for Eurozone countries embarking on deficit reduction during the current recession. The IMF have a produced a paper – The Challenge of debt reduction during fiscal consolidation – which looks at the theory and empirical evidence behind this idea. It’s a difficult paper, but the main conclusions are

- A large fiscal multiplier of close to 1 can cause debt consolidation to increase debt to GDP ratios in the short term.

- Using debt ratio targets (e.g. EU fiscal rules) are likely to lead to disappointment. Because government miss their debt targets, they may engage in even more levels of fiscal consolidation trying to meet targets. The IMF propose the use of cyclical adjusted debt targets. This allows for the short term increase in debt to GDP caused by the cyclical downturn.

- Debt consolidation packages can be modified to minimise the impact on economic growth – e.g. delaying spending cuts until the economy is stronger, and choosing those cuts which have less impact on economic growth. (the IMF don’t mention it, but accommodative monetary policy would also be an issue)

- The increase in Debt – GDP ratios is worse for countries with high debt and in a recession.

From the IMF introduction:

With multipliers close to 1, fiscal consolidation is likely to raise the debt ratio in the short- run in many countries. Although the debt ratio eventually declines , its slow response to fiscal adjustment could raise concerns if financial markets react to it s short-term behavior. It may also lead country authorities to engage in repeated rounds of tightening in an effort to get the debt ratio to converge to the official target. Not explicitly taking into account multipliers or underestimating their value may lead policy-makers to set unachievable debt targets and miscalculate the amount of adjustment necessary to bring the debt ratio down.

Why does fiscal consolidation increase debt levels?

- Firstly debt is usually measured as debt as a % of GDP. (debt /GDP)

- If GDP falls, then even if debt levels stay the same, – (Debt / GDP) will rise.

- In a recession, we are likely to see a fiscal multiplier of 1 or even greater. This means £30bn of fiscal consolidation will see a fall in GDP of £30bn. Therefore, debt falls, but GDP falls by a similar amount.

- Also, if GDP falls, this will cause an increase in the cyclical deficit. The government receive lower tax revenue and have to spend more on unemployment benefits.

- In countries without a flexible exchange rate or flexible monetary policy, the fiscal multiplier effect could be even larger than one.

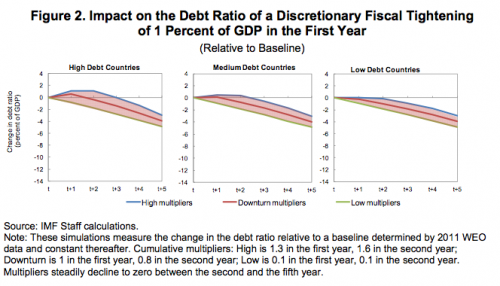

This model shows, high debt countries, with a multiplier of 1.3 would see an increase in the debt ratio for the first three years. In a recession, the multiplier effect of fiscal consolidation.

Example from 2009-11.

Source: OECD | S&P pdf on Europe’s recession