Question and answers on the difficulty of switching from non-renewable energy sources, such as fossil fuels. (from – finding alternatives to fossil fuels)

Readers Question: Why is it that on a global scale, alternative fuels are somewhat being ignored?

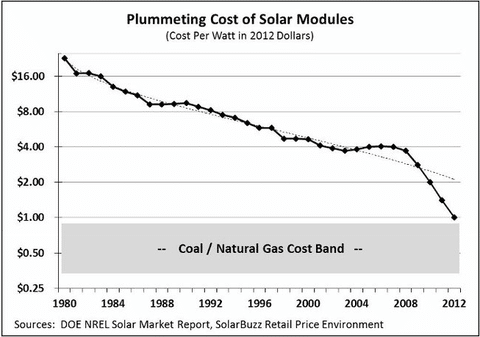

Firstly, fossil fuels are still cheaper. However, the gap is narrowing. For example, see how solar panels are coming down in costs.

There can be a reluctance to switch from one mode of production to another. Even if an alternative became cheaper, it requires significant investment to switch from one mode of power to another. For example, the UK kept steam trains running into the mid 1960s. Diesel was more efficient and cheaper many years previously, but it required a lot of investment in infrastructure to buy new diesel trains. Often it’s easier to keep going with old technology out of habit and merely because it is what has been used in the past. In some parts of the world, steam power is still used.

But, on the other hand, if we look back in history, we can see that a dominant technology can quite quickly lose its position. America quite quickly switched from steam trains to the petrol powered car. Once a tipping point is reached the momentum can swing to the new technology.

Also, a factor is that oil and petrol companies are very profitable and it is in their interests to keep oil based industries strong. If they can delay a switch to alternative fuels they might try. How much ability they have to delay an energy switch is open to question. But, there are powerful lobbyists to support the US coal and oil industries.

Readers Question: If it is not being ignored, Why is research and development is somewhat slow?

Alternatives to fossil fuels are generally not profitable in the short term. Therefore, private enterprise has limited incentives to research alternatives. This is an example of market failure, because the market ignores:

- The long term importance of developing alternatives to fossil fuels, which will one day run out.

- The external benefits of developing alternatives to fossil fuels, e.g. improvement in environment and reduced pollution.