Readers Question: What effect do interest rates (either a rise, fall or steadying) have on both monetary and real wages? I think I’ve got my head around it, but I’m looking for a nicely explain summary (understanding that there are probably a million of contributing factors that can lead to a million outcomes!)

You are right, there is no direct link between interest rates and wages (either nominal or real), and there are thousands of possible combinations, which make it difficult to create simplistic answers. But, interest rates can have an impact on wages by affecting the rate of economic growth and inflation.

Interest rates and economic growth

Higher interest rates increase the cost of borrowing, so firms will cut back on investment and consumers will cut back on spending. This could lead to lower economic growth. With less demand and higher interest payments, firms may seek to cut wages (or increase wages at a slower rate)

Furthermore, if higher interest rates do have the desired effect of reducing the rate of economic growth, then as well as lower economic growth, we should get lower inflation. This will be another factor leading to lower nominal wage growth.

Fall in AD

In this case, higher interest rates have reduced AD, leading to lower inflation and lower economic growth.

With lower inflation, we would expect to see lower nominal wages. But, also real wages (nominal – inflation) may be less affected.

Suppose inflation is running at 4% and nominal wage growth is running at 6%. (real wages = 2% growth)

Higher interest rates may reduce inflation to 2% and nominal wage growth falls to 4%. (but, real wage stay at 2%)

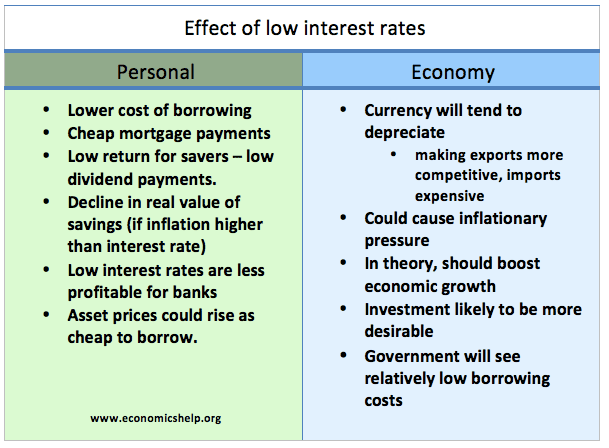

A look at the economic effects of a cut in interest rates.

Summary

Lower interest rates make it cheaper to borrow. This tends to encourage spending and investment. This leads to higher aggregate demand (AD) and economic growth. This increase in AD may also cause inflationary pressures.

In theory, lower interest rates will:

Reduce the incentive to save. Lower interest rates give a smaller return from saving. This lower incentive to save will encourage consumers to spend rather than hold onto money.

Cheaper borrowing costs. Lower interest rates make the cost of borrowing cheaper. It will encourage consumers and firms to take out loans to finance greater spending and investment.

Lower mortgage interest payments. A fall in interest rates will reduce the monthly cost of mortgage repayments. This will leave householders with more disposable income and should cause a rise in consumer spending.

Rising asset prices. Lower interest rates make it more attractive to buy assets such as housing. This will cause a rise in house prices and therefore rise in wealth. Increased wealth will also encourage consumer spending as confidence will be higher. (wealth effect)

Depreciation in the exchange rate. If the UK reduce interest rates, it makes it relatively less attractive to save money in the UK (you would get a better rate of return in another country). Therefore there will be less demand for the Pound Sterling causing a fall in its value. A fall in the exchange rate makes UK exports more competitive and imports more expensive. This also helps to increase aggregate demand.

Overall, lower interest rates should cause a rise in Aggregate Demand (AD) = C + I + G + X – M. Lower interest rates help increase (C), (I) and (X-M)

UK interest rates

UK interest rates were cut in 2009 to try and increase economic growth after the recession of 2008/09, but the effect was limited by the difficult economic circumstances and the after-effects of the global credit crunch.

AD/AS diagram showing effect of a cut in interest rates

If lower interest rates cause a rise in AD, then it will lead to an increase in real GDP (higher rate of economic growth) and an increase in the inflation rate.

When interest rates were cut to 0.5% in March 2009, few would have predicted that interest rates would have stayed low in UK, US and the Eurozone for so long. Interest rates have stayed at zero for several years – defying several predictions that they will rise soon. Who benefits from low-interest rates and who …

The Bank of England set the base rate. The base rate is the rate at which they charge commercial banks to borrow from the Bank of England. In normal economic circumstances, this base rate will influence all the interest rates set by other banks and financial institutions. If the Bank of England cut the base …

It is not a good time to be a saver in the UK. Interest rates are 0.5% and inflation has been above 2% for a high proportion of the previous five years. Because inflation is higher than nominal interest rates, we are seeing negative real interest rates. This means many savers are seeing a decline in the real value of their savings. Pensioners who are relying on interest payments as income, are seeing a decline in their income.

Inflation and interest rates

In most of the post-war period we have seen positive real interest rates – Base rates above the headline inflation. This means that savers are protected from the effects of inflation.

H0wever, 2008 marks a sharp contrast, with Bank of England base rates falling to 0.5% and inflation reaching above 5%.

In recent months, inflation has fallen to below 2%, but that is still higher than base rates of 0.5%

Effectively, you are getting 0.5% return on your saving, but prices are going up 2%, so the real value of your savings is falling by 1.5%.

Base rates and bank rates

The contrast between base rates and inflation looks very high. But, actually bank savings rates have not fallen as much as base rates. This is because banks were short of money in the credit crunch and were keener to attract deposits than lend money. Therefore, when the Bank of England cut interest rates to 0.5%, commercial banks were not so keen to reduce their own interest rates by as much. Usually commercial bank rates closely follow base rates, but after 2008 we see a break in this correlation.

In 2008/09, base rates are cut from 5% to 0.5%, but fixed interest rates (series IUMWTFA) only fall to 2.5 / 3%. Interestingly since mid 2012, fixed interest rates have continued to fall closer to 1%. This suggests the banks are less desperate to attract saving deposits and so can reduce interest rates.

It is a similar story with instant access saving rates (series IUMB6VJ) Since mid 2012, rates have fallen from 1.6% to 0.6%. This suggest the financial sector is in better health, but it means a poorer return for savers.

However, if you look around, you can still see higher fixed rates for those willing to ‘lock their money away’

It also depends how much money you can save. For example, according to ‘Money Saving Expert‘ you could get 3.25% if you can put £25,000 away for 5 years. – hardly a great deal, but you would just about get a positive real interest rate.

Should the Bank of England do more for savers?

In the past few years, many groups representing savers have felt they have been ignored – and the government / Bank of England should have done more to give a better rate of return for savers.

However, the past five years have seen declining living standards for most groups of people – real wages have fallen. Unemployment has been very high. The cost of renting has been very high. Given the general economic decline, savers have not been alone in seeing falling living standards. It is complicated by the fact that people with high levels of saving are more likely to be household owners. Homeowners have seen record low mortgage interest payments and rising house prices, which, to some extent, have offset the fall in the return on savings.

Young people without savings, but paying rent, have seen a bigger squeeze on their living standards.

However, someone who is relying on their savings to pay rent, is definitely in a bind.

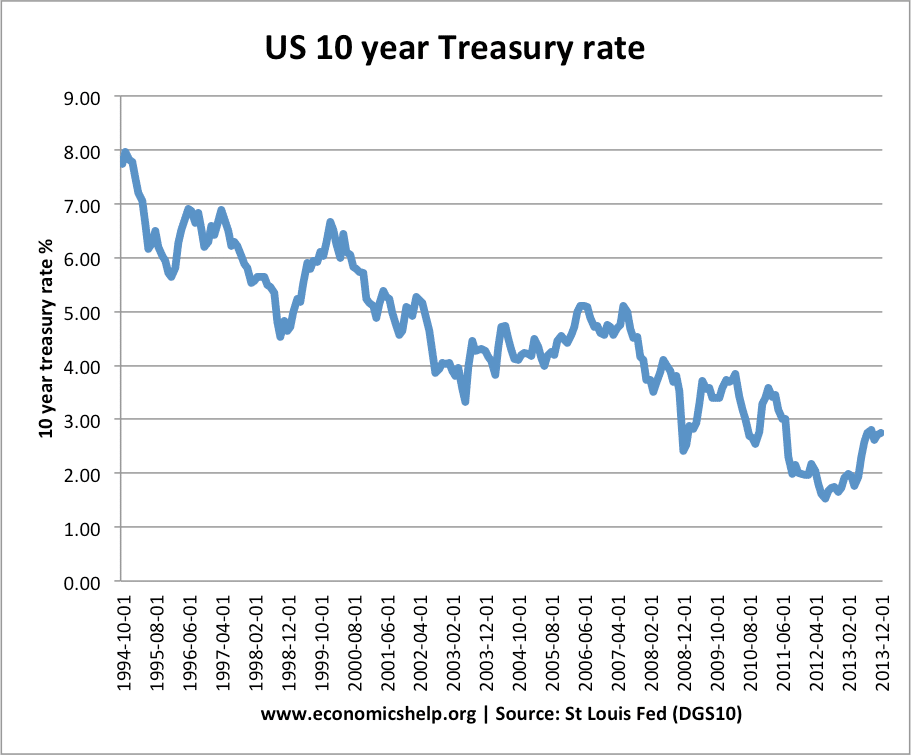

Readers Question: As the FED is talking about tapering and at the same time keeping interest rate low. How can they both go together? Tapering will raise yield as bond prices go down in absence of any freak buying. And interest rate will chase yield this causes interest rate to climb up.

Fed Tapering means that the Federal Reserve will begin to stop buying bonds, and no longer continue to create money and buy bonds. This tapering could also be seen as a preliminary to reversing quantitative easing and selling the bonds that have been accumulated.

It is important to bear in mind there are different interest rates in the economy.

Discount rate –set by Federal Reserve

Federal Funds rate – short term interbank lending rate, influenced by open market operations of the Fed.

Long term bond yields. – Effective interest rate on 10 year Treasury bonds.

Discount Rate

The Federal Reserve can change the discount rate (see: Federal Reserve discount rate). This is the rate that the Fed charges commercial banks to borrow directly from the Federal Reserve. This is a short-term interest rate because commercial banks borrow from the Federal Reserve to meet temporary shortfalls in their cash flow.

The Federal Reserve discount rate is currently 0.75% (link)

This Federal discount rate does influence other interest rates in the economy. If commercial banks find the discount rate has increased, then they are likely to increase their interest rates on loans to consumers. If commercial banks see the discount rate has increased, they tend to increase mortgage rates. Therefore, the Federal Reserve can influence other bank rates.

It is a similar situation in the UK. The Bank of England change the base rate. This base rate usually has a strong influence on other bank rates in the economy.

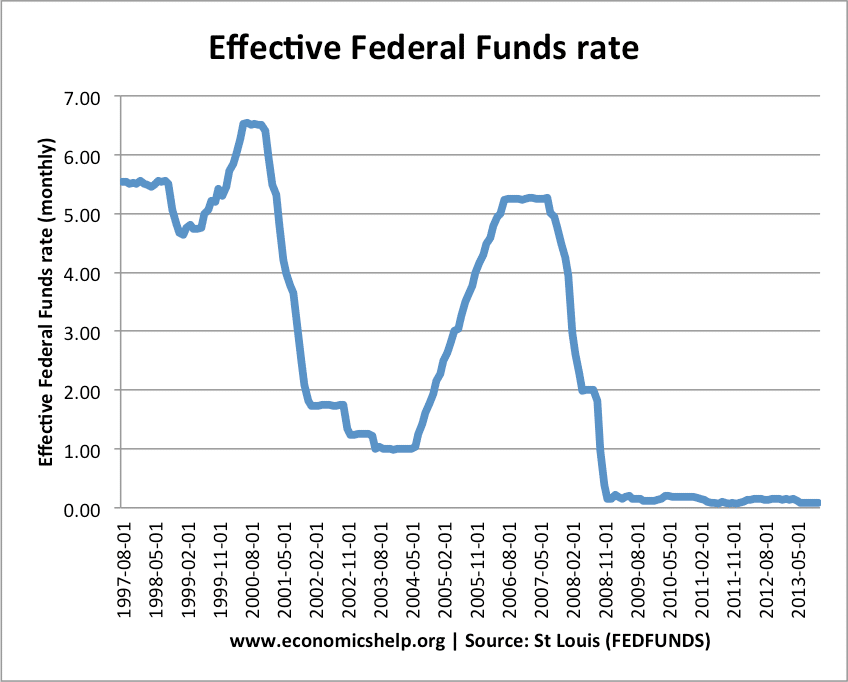

Effective federal funds rate

Another important interest rate in the economy is the effective Federal Funds Rate – see FEDFUNDS. This is the short-term inter bank lending rate. It is influenced by the Fed discount rate, but also the willingness of banks to lend to each other. It is also, influence by the Federal Reserve’s actions in open market operations. The FED has a target for the Federal Funds rate. When the Fed starts to sell bonds, you would expect this to depress the price of bonds and push up the Federal Funds Rate. With the Fed currently buying bonds, this has pushed up bond valued and decreased interest rates.

Readers Question: Is it possible to have negative interest rates?

Negative interest rates occur when a bank charges you money for the privilege of looking after your savings. It is possible to have a negative interest rate (e.g. -0.5%) Although it is quite rare. The Bank of England have recently talked about the possibility of a negative interest rate for commercial bank deposits at the Bank of England.

Why is Bank of England Talking about a negative interest rate?

The UK economy is still stagnant with little sign of economic growth. Usually, a prolonged recession would lead to lower interest rates to encourage borrowing. However, since interest rates fell to 0.5% in March 2009, interest rates have stayed the same as there is little precedent for cutting interest rates further.

The Bank has tried quantitative easing but this has not really encouraged bank lending and normal economic activity.

The Bank of England, in particular want to encourage lending to small businesses – small businesses have complained it is very difficult to borrow from commercial banks in the present economic climate. At the moment, commercial banks prefer to increase their cash reserves, which they deposit at Bank of England and not lend. At the moment commercial banks get a small interest rate payment 0.5% on their deposits. However, if there is a cost for depositing money at the Bank of England, they would have a greater incentive to lend money. In theory, commercial banks will lend more and this would stimulate business investment and economic growth. Higher lending would also help to reduce unemployment and reduce the cyclical budget deficit.

The Bank of England would probably introduce a new deposit rate. For example, deposits over £1billion at the Bank of England would be charged the negative interest rate.

The first £1 billion may still receive the base rate of +0.5%. This means that small building societies would not face a negative interest rate. This could cause problems because a negative interest rate could mean they would have to pay people with tracker mortgages (mortgages that follow base rate), and they could go out of business because they couldn’t recoup money from savers. The deposit rate would mainly affect the large commercial banks with high cash reserves.

What would happen to saving rates?

If the Bank of England had a negative interest rates on deposits, commercial banks would be less keen to encourage banks deposits, therefore they may reduce interest rates on saving accounts. Savers would see a fall in income.

In theory, lower interest rates may encourage spending (rather than saving (substitution effect). However, consumers may be quite inelastic to the interest rate. It may also be outweighed by the decline in income of savers who rely on interest payments (income effect).

What are the Problems of a Negative Interest Rate?

Some fear a negative interest rate could encourage a new lending boom. Banks might be so keen to get rid of cash, they start lending to business without evaluating how good the loan is. Austrian economists are particularly critical of negative interest rates as they argue it can lead to asset booms and distort the market. However, there is no sign of a new lending boom in the short term, the real problem is that banks don’t want to lend because of the economic situation.

Savers will lose out. With inflation already above target, a fall in the saving rate will lead to an even bigger negative real interest rate. Savers will see a fall in their real wealth and living standards.

Banks may still not want to lend. The main thing holding back lending may be the overall state of the economy. Even cutting interest rates to negative may fail to increase lending.