Deflation means a fall in prices (a negative inflation rate).

Though policymakers should generally be concerned if there is an inflation rate less than the target of 2%.

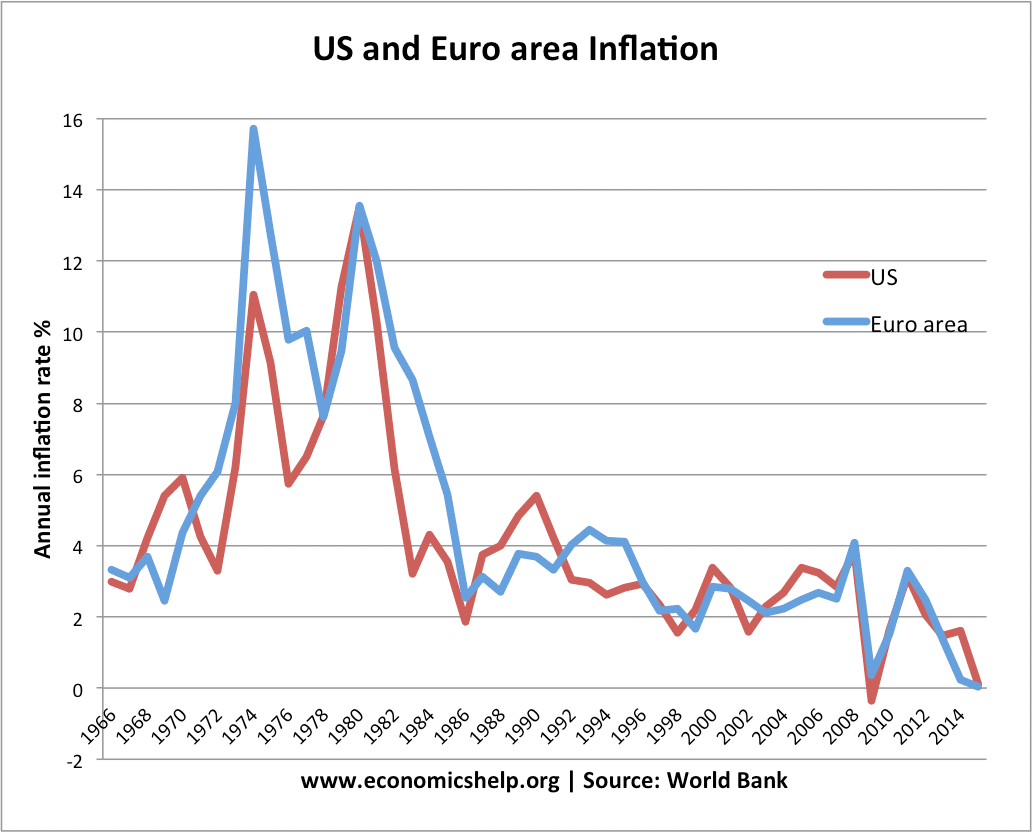

For example, in the Eurozone Jan 2015, the headline inflation rate is -0.2%. Even if we strip away volatile prices like oil, core inflation is 0.8%. This is a very low rate of inflation.

There are many serious potential problems of low inflation/deflation

- Higher real debt burdens,

- Decline in spending,

- Higher unemployment.

See costs of deflation for more detail.

What options are available to overcome deflation?

Monetary policy

The traditional tool of monetary policy is interest rates. If inflation is too low, the Central Bank can try to cut interest rates. In theory, this should boost spending and aggregate demand. For example, lower rates reduce the cost of mortgage payments, giving people more to spend.

However, there are times when cutting interest rates are not sufficient. In a liquidity trap – zero interest rates may not encourage sufficient spending. For example, after the credit crunch – lower interest rates failed to boost demand sufficiently. Lower interest rates failed to solve low inflation for many reasons:

- People preferred to save because of ongoing recession

- People took opportunity to pay off debts

- Banks didn’t want to lend, so firms couldn’t get loans despite low rates

- Banks didn’t pass the full base rate cut onto consumers.

Unconventional monetary policy

With a failure of interest rates, the traditional tool of monetary policy, Central Banks needed to consider unconventional monetary policy. Some of these policies are relatively untried.

Helicopter drop – print money

In theory, creating inflation should be the easiest thing – just print money and according to the quantity theory of money – we should get inflation. A particular policy for printing money is termed the ‘helicopter drop’ – where the Central Bank gives newly created money to consumers directly. Central Banks have been reluctant to pursue this strategy, presumably because it goes against the mentality of serious Central Bankers and their inflation-fighting credentials. But, it would be a solution to deflation. The most challenging aspect would be knowing about much money to print, to get the right amount of inflation.

Quantitative easing

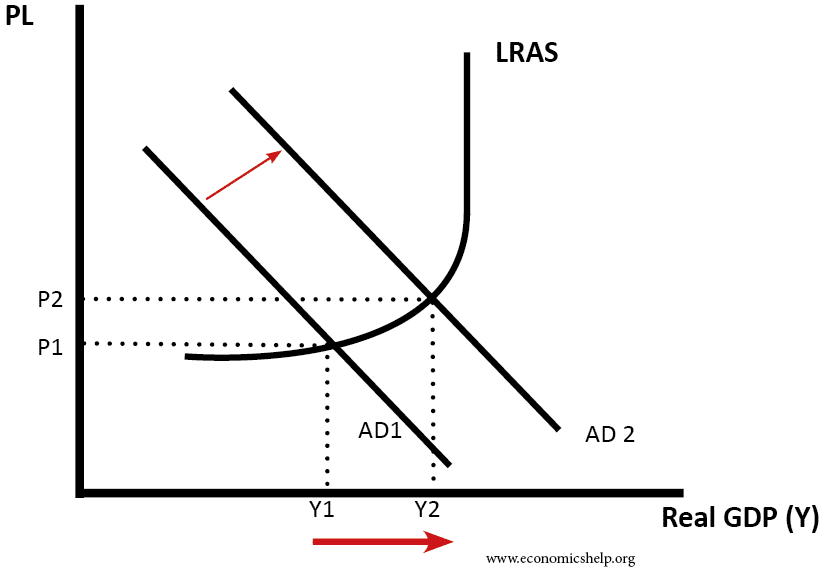

There are different variations of quantitative easing, but the one used by the UK and US, involves the Central Bank creating money and using this to buy government bonds. This should reduce bond yields, and increase the money supply. But, since the introduction of Q.E., the impact has been fairly limited. Banks haven’t been so keen to lend out the money they received from selling bonds. However, Q.E. may explain why UK and US have higher inflation rates and higher growth than the Eurozone, which until Jan 15 avoided real Q.E.

Change inflation expectations

One of the biggest challenges to overcome deflation is to change inflation expectations. When people expect deflation – firms will not give wage rises, consumers won’t pay higher prices. But, if people do expect inflation, then firms are more willing to increase wages and consumers will be more willing to pay higher prices. Expectations are often self-fulfilling. This is why the ECB announced a bigger than expected Q.E. package – they were trying to influence expectations of inflation, which will make it easier to solve deflation.

Devaluation

Another option to increase inflation is to pursue devaluation – attempting to reduce the value of the currency, through selling domestic currency and/or increasing the money supply to try and devalue the currency. Devaluation will help increase inflation and inflation expectations, through a boost to domestic exports and higher import prices. The difficulty is that in an era of general deflation – many countries may be trying to do the same thing, leading to competitive devaluation. Also, it will reduce living standards by making imports more expensive.

Fiscal Policy

When monetary policy is ineffective, many economists suggest fiscal policy should play a greater role. If the private sector wants to save, the government should borrow from the private sector and stimulate economic activity through higher infrastructure spending. This expansionary fiscal policy can help to kick-start the economy and hopefully create a positive multiplier effect to create more normal levels of economic growth and reach the inflation target.

Some fear that in an economic downturn, there is no room for the government to borrow because they are already exceeding debt limits (e.g. growth and stability pact) In this case, the government could fund expansionary fiscal policy through Q.E. – Central Bank creating money and buying the debt the government creates.

The fear is that if governments spend – financed through money creation it will lead to inflation. But, in a period of deflation – that is the aim.

Why is it so hard to overcome deflation?

In theory, it may seem easy to overcome deflation – people are always warning of the dangers of inflation. Yet, in many cases (Japan 90s and 00s. Europe since ’10 – deflation can be dangerously persistent. Part of the reason is deflation expectations can get entrenched and the other part is that Central Banks are so used to fighting inflation – they become fearful of doing too much to solve deflation. Therefore, inflation-fighting policies often tend to err on the cautious side. But, there are real costs in failing to overcome deflation.

Related

Thanks for the post.

I fear we are already beyond conventional means. Europe is heading toward Japanese-style stagnation, and it is due in part to demographics. German cpi can in negative, which is no surprise as they are aging fast. If Japan is the model then I doubt QE will have more than a marginal impact. Helicopter money would have been better, but that isn’t the role of a central bank.

Why the Central Bank creating money and use this to buy government bonds will reduce interest rate?

Ya”ll should do the helicopter drop for sure

the helicopter drop is more effective for sure

KEEP ON THE GOOD WORK

well explained

Is it true that Keynes assumed money supply to be constant in his Liquidity Preference Theory?

Good work they should do helicopter drop