Economics is a broad subject concerned with the optimal distribution of resources in society. Within the subject, there are several different branches which focus on different aspects. Also, there are different schools of thought which generally have different views on aspects of economics.

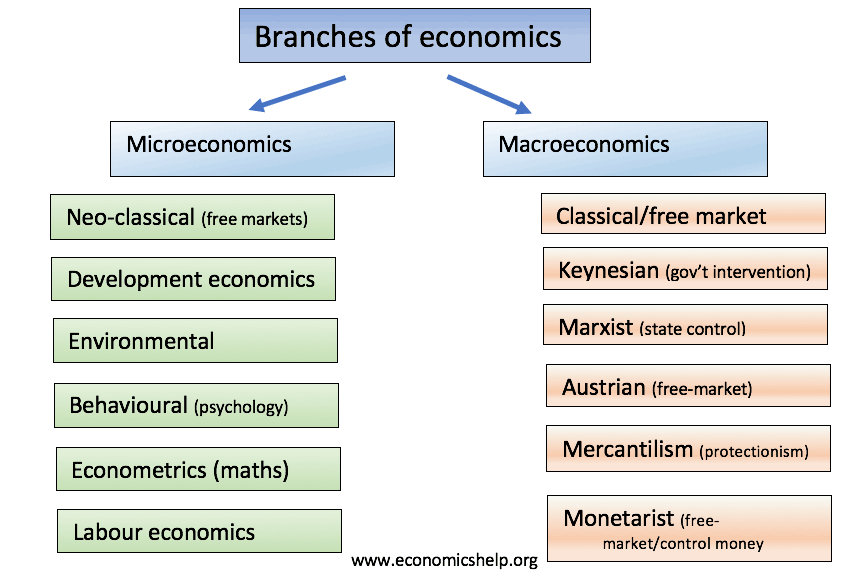

The first way to split economics is microeconomics and macroeconomics.

- Microeconomics – concerned with individual markets and small aspects of the economy.

- Macroeconomics – concerned with the whole aggregate economy. Issues such as inflation, economic growth and trade.

To some extent, the split is artificial. Aspects of microeconomics filter into macro-economics. For example, if you take the study of developing economies, this involves both looking at micro-aspects of development (agricultural markets) and macro-aspects like growth. See the difference between macro and microeconomics.

Branches of economics

1. Classical economics

Classical economics is often considered the foundation of modern economics. It was developed by Adam Smith, David Ricardo, Jean-Baptiste Say. Classical economics is based on

- Operation of free markets. How the invisible hand and market mechanism can enable an efficient allocation of resources.

- Classical economics suggests that generally, economies work most efficiently when government intervention is minimal and concerned with the protection of private property, promotion of free trade and limited government spending.

- Classical economics does recognise that a government is needed for providing public goods, such as defence, law and order and education.

2. Neo-classical economics

Key people: Leon Walrus, William Jevons, John Hicks, George Stigler and Alfred Marshall.

Neo-classical economics built on the foundations of free-market based classical economics. It included new ideas such as

- Utility maximisation.

- Rational choice theory

- Marginal analysis. How individuals will make decisions at the margin – choosing the best option given marginal cost and benefit.

Neo-classical economics is often considered to be orthodox economics. It is the economics taught in most text-books as the starting point for economics teaching. The tools of neo-classical economics (supply and demand, rational choice, utility maximisation) can be used in new fields and also for critiques.

3. Keynesian economics

Key people: John Maynard Keynes, Paul Samuelson.

Keynesian economics was developed in the 1930s against a backdrop of the Great Depression. The existing economic orthodoxy was at a loss to explain the persistent economic depression and mass unemployment. Keynes suggested that markets failed to clear for many reasons (e.g. paradox of thrift, negative multiplier, low confidence). Therefore, Keynes advocated government intervention to kick-start the economy.

Keynesian economics is credited with creating macroeconomics as a distinct study. Keynes argued that the aggregate economy may operate in very different ways to individual markets and different rules and policies were needed.

Keynes didn’t reject all elements of neo-classical economics but felt new ideas were needed for the macro-economy – especially with the economy in recession.

4. Monetarist economics

Key people: Milton Friedman, Anna Schwartz.

Monetarism was partly a reaction to the dominance of Keynesian economics in the post-war period. Monetarists, led by Milton Friedman argued that Keynesian fiscal policy was much less effective than Keynesians suggested. Monetarists promoted previous classical ideals, such as belief in the efficiency of markets. They also placed emphasis on the control of the money supply as a way to control inflation.

Monetarist economics became influential in the 1970s and 1980s, in a period of high inflation – which appeared to illustrate the breakdown of the post-war consensus

5. Austrian economics

Key people: Ludwig Von Mises, Carl Menger

This is another school of economics that was critical of state intervention, price controls. It is broadly free-market. However, it criticised elements of classical school – placing greater emphasis on the individual value and actions of an individual. For example, Austrian economists argue the value of a good reflects the marginal utility of the good – rather than the labour inputs.

6. Marxist economics

Key people: Karl Marx

Emphasises unequal and unstable nature of capitalism. Seeks a radically different approach to basic economic questions. Rather than relying on free-market advocate state intervention in ownership, planning and distribution of resources.

7. Neo-liberalism/Neo-classical

A modern interpretation of classical economics. Considerable overlap with monetarism. Essentially concerned with the promotion of free-markets, competition, free trade, privatisation, lower government involvement, but some minimal state intervention in public services like health and education. Few identify as ‘neo-liberal’ – sometimes used as a term of abuse.

- Neoliberalism | Related terms: Washington Consensus

New Branches of economics

Environmental economics/welfare economics

Key people: Garrett Hardin, E.F. Schumacher, Arthur Pigou.

This places greater emphasis on the environment. This can include:

- Neo-classical analysis of external costs and external benefits. From this perspective, it is rational for man to reduce pollution

- Market failures – tragedy of the commons, Public goods, external costs, external benefits.

- Environmental economics can take a more radical approach – questioning whether economic growth is actually desirable.

Behavioural economics

Key people: Gary Becker, Amos Tversky, Daniel Kahneman, Richard Thaler, Robert J. Shiller,

Behavioural economics examines the psychology behind economic decision making and economic activity. Behavioural economics examines the limitation of the assumption individuals are perfectly rational. It includes

- Bounded rationality – people make choices by rules of thumb

- Irrational exuberance – People get carried away by asset bubbles.

- Nudges/Choice architecture – how the framing of decisions affects the outcome

Development economics

Key people: Simon Kuznets and W. Arthur Lewis, Amartya Sen and Muhammad Yunus.

Concerned with issues of poverty and under-development in poorer countries of the world. Development economics is concerned with both micro and macro aspects of economic development. Issues include

- Trade vs aid

- Increasing capital investment.

- Best ways to promote economic development

- Third World debt

Econometrics

Key people: Jan Tinbergen

Use of data to find simple relationships. Econometrics uses statistical methods, regression models and data to predict the outcome of economic policies. For example, Okun’s law suggests a relationship between economic growth and unemployment.

Labour economics

Key people: Knut Wicksell

Concentration on wages, labour employment and labour markets. Labour economics starts from the neo-classical premise of labour supply and marginal revenue product of labour.

Recent developments in labour economics have placed greater emphasis on non-monetary factors, such as motivation, enjoyment and labour market imperfections.

Other schools of economics

Chicago school – Based on neo-classical economics, rational choice and benefits of free markets. Key people from Chicago university, include Frank Knight, Milton Friedman, Eugene Fama and Gary Becker

Institutional economics – A look at how institutions, society and social trends can influence economics. A forerunner of behavioural economics. Key people include Thorstein Veblen, John Kenneth Galbraith, and Ha-Joon Chang.

Distributism/social-democratic approach. Seeking a third way between capitalism and socialism.

Real Business Cycle – Models that suggest macroeconomic fluctuations caused by supply-side changes, such as technological shocks. See – Real business cycle

Mercantilism – Early model of economics emphasising tariff barriers and the accumulation of gold reserves. Mercantilism

Modern Monetary Theory (MMT) – is a recent development that emphasises the ability of the government to print money and borrow in order to achieve full employment. See Modern Monetary Theory (MMT)

Related

This article was helpful

This article has opened my mind

So simple and so large. That is impossible. Or not.