Microeconomics is concerned with the economic decisions and actions of individuals and firms.

Within the broad church of microeconomics, there are different theories that emphasise certain assumptions and expectations of economic behaviour. The most important theory is neo-classical theory, which places emphasis on free-markets and the assumption individuals are rational and seek to maximise utility. However, there are many critiques of the neo-classical model, arguing economics is more complex with issues of market failure and irrational behaviour.

Pre-classical microeconomic theory

Before, Adam Smith, economics was more disparate with no commanding overall theory. Philosophers like Aristotle and Plato made references to issues in economics such as division of labour. The dominant ideas, pre-classical economics, were based on theories of mercantilism – the idea a nation should try to accumulate gold.

Classical microeconomic theory

Classical microeconomic theory was developed by Adam Smith (Wealth of Nations, 1776) and later economists, such as David Ricardo The essential aspect of classical microeconomic theory include:

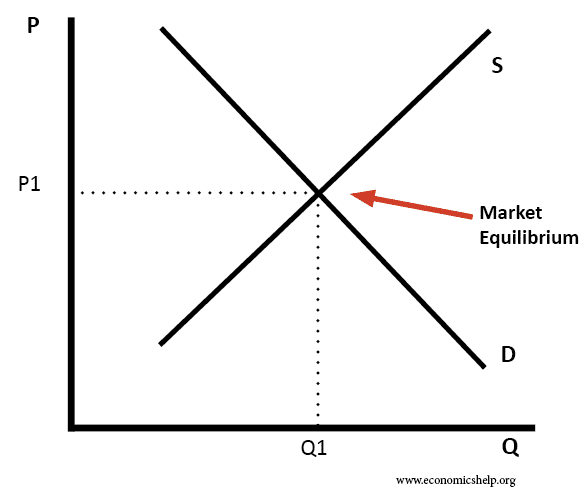

Determination of market price and output

Adam Smith mentioned the ‘invisible hand of the market.’ He noted how when people act out of self-interest, markets tend to provide goods and services which are demanded by the population. It needed no central price setting, but market forces responded to changes in demand and supply, e.g. a shortage pushes up the price and causes demand to fall.

Smith also investigated topics such as the division of labour, specialisation and economies of scale.

The early classical economists emphasised the importance of costs to firms and consumers.

2. Utility maximisation

An important development of classical economics towards the end of the nineteenth century is the concept of utility maximisation. The concept of utility was developed by philosophers/economists – Jeremy Bentham and John Stuart Mill.

In microeconomic theory, it was believed a consumer will buy goods depending on the marginal utility (satisfaction) they get from the good. This theory assumes consumers are rational and seeking to maximise the satisfaction they get.

Neo-classical theory

Neo-classical theory is a modern re-interpretation of classical economics of the nineteenth century. Neo-classical theory places importance on markets, but developed new ideas, especially regarding utility and rational choice theory. Elements of neo-classical theory.

- Market distribution of goods and services.

- Rational choice theory. This is the idea individuals hold rational preferences and make rational choices; seeking to maximise their outcomes – be it profit, wages, consumption or investment.

- People act independently and make use of available information.

- Marginalism. In neo-classical economics, more emphasis was placed on concepts of marginal utility and marginal cost. We make choices depending on satisfaction we get from one extra unit of a good.

Economists such as Carl Menger, William Stanley Jevons and Marie-Esprit-Léon Walras. and Alfred Marshall developed ideas such as diminishing marginal utility.

Many of these neo-classical economic theories were brought together in Alfred Marshall’s very influential textbook, Principles of Economics. (1890)

- Note there is some blurring between classical economics and neo-classical economics.

- Neo-classical economics has also come to mean ‘orthodox economic theory. To a large extent, it has incorporated new developments in microeconomics, such as theories of market failure, market structure and econometrics.

Theories of Market failure

Neo-classical economics has become associated with a belief in the efficiency of markets. However, microeconomic theory has also incorporated the criticisms and limitations of free-markets.

- Monopoly. Adam Smith was well aware of the problem of monopolies and how firms could use their market power to set excessive prices.

- Imperfect competition. In the 1930s, Joan Robinson developed a model of imperfect competition, an awareness many markets were somewhere between monopoly and perfect competition often assumed in neo-classical economics.

- Externalities. Developed by Arthur C.Pigou in The Economics of Welfare (1920) this is the awareness production and consumption decisions can have harmful (or positive) effects on third parties. Therefore, a free market can lead to overconsumption of demerit goods and negative externalities.

- Game theory. An awareness, decisions are not linear or simple, but the interdependence of agents influences what we decide to do.

Behavioural economics

The most important trend in recent decades in economics is the greater emphasis placed on aspects of behavioural economics, which uses many insights from related fields such as psychology.

- Disputes rational choice theory. The essential element of behavioural economics is that it argues individual agents are often not rational and often do not seek to maximise utility.

- Behavioural economics examines how agents can be influenced by biases, and make decisions not predicted by neo-classical economic theory. Behavioural economics can explain the irrational exuberance of booms and busts.

Econometrics

In the post-war period, economics became increasingly mathematical with economists attempting to use mathematics to explain models and theories. Econometrics looks at economic data and seeks to extract simple relationships. The basic tool is the linear regression models and can be used to try and predict consumer spending and demand for labour.

Heterodox models of microeconomics

Heterodox models differ substantially from microeconomic foundations of neo-classical economics. Schools of thought include

Marxist economic theory

Karl Marx developed an alternative perspective on economics. He focused on the surplus value created under the capitalist economic system. To Marx, the invisible hand of the market would be better described as the invisible hand of capitalist exploitation of workers. Marx claimed workers did receive their full labour value but were compensated for their necessary labour only – enabling capitalists to profit from the surplus.

Institutional economics. The role of society and institutions in shaping economic behaviour. For example, Thomas Veblen looked at theories of ‘conspicuous consumption’ and noted how the desire for social status could drive much economic theory. Institutional economics could be seen as a forerunner for later behavioural economics.

Environmental economics Argues traditional economics wrongly places value on increasing output. The most important thing is creating a sustainable environment which maximises living standards.

Buddhist economics/non-profit goals. Like environmental economics, this questions the assumption higher incomes and higher output are desirable. The theory of hedonistic relativism suggests higher incomes do nothing to increase happiness levels, and traditional economics can encourage society to pursue materialistic goals which actually create more problems of stress, conflict and environmental degradation.

Some of the basic models you might find in A-Level economics

- Price Discrimination

- Perfect competition

- Price Mechanism

- Monopoly

- Oligopoly and kinked demand curve

- Game Theory Pricing strategies

- Market failure

- Behavioural economics

Theory n A model or framework (made up of a body of principles) to explain phenomena. The word ‘theory’ derives from the Greek word ‘theorein’, which means ‘to look at’.

Related

Thank you soooooooo much that was really great.

I was searching entire internet to get models and you explained it so simply by making me understand tmodels as theories.

Iam greatful.

Studying at AME University in Liberia

i really appreciate this..

tnx for this web,

i find it so easy to understand the micro economic theory becouse,On how they have explain it,one find it easy to relate it in real life business action.

Thanks for the the informative site indeed

Thanks for providing such compressed information in very simple and effective way. It is a road map of how you should read economics, it’s theories and principles.

thank you so muccchhhh

Please can I get assistance here, I need a tutor in microeconomics theories and econometrics

Thank u soooo much😊

Thank you👊