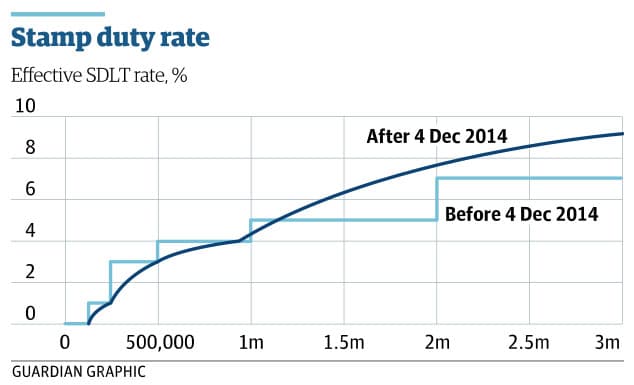

The government have announced a change in stamp duty. The chancellor George Osborne claims the change to stamp duty will cut the rate of tax for 98% of house purchases.

New marginal tax rates are:

0% tax on house purchases up to the value of £125,000

2% tax on purchases between £125,000 and £250,000

5% tax on purchases from £250,000 up to £925,000

10% tax on purchases from £925,000 to £1.5m

12% tax on purchases over £1.5m

The tax change will cost the public purse £800m and represent a £4,500 cut in tax on average home of £275,000.

For an average priced home of £275,000, there will be £4,500 cut in stamp duty.

Commentary

Firstly, it makes sense to get rid of the old system, where a £1 increase in house price could cause £3,000 extra tax. Marginal tax rates avoid this tax-cliff, which distorted house sales around the stamp duty rates.

It is also very progressive, with a steep increase in tax rates for more expensive houses. In some ways the new stamp duty is a weak substitute for the proposed mansion tax.

However, there are two main problems.

1. This is not a good time for tax cuts. Given the need to improve public finances, it seems strange to offer a big tax cut on stamp duty. Revenues from stamp duty have already fallen significantly since 2008 because of lower house sale volumes. This tax cut will worsen public finances. It would be better to avoid a tax cut for stamp duty and have an extra £800m to spend on infrastructure (like for example, building affordable social housing).

Some might say, ‘But, you often argue for expansionary fiscal policy, so why not support a tax cut to boost spending and support economic growth?” – Well firstly, the aim of this tax cut is not to boost economic growth. If you did want to pursue expansionary fiscal policy, you would cut VAT or income tax. Increasing income tax threshold would increase consumer spending, but I’m not convinced a cut in stamp duty would have much impact. A cut in stamp duty is not really going to encourage people to go out and spend supporting a sustained economic recovery.

With stamp duty cut we get the worst of both worlds – we get a deterioration in public finances, but it doesn’t even offer much help to the economic recovery.

Readers Question: There are around 22 million households in the UK, 2/3 of whom own their house. So the rental market would be around 7 million of whom one million receive benefit, some portion living in social housing, some in private rented housing. Does that seem reasonable? Can you point me towards actual numbers?

In August 2014, 4.93 million received housing benefit, at an average weekly payout of £93. This gives a rough annual cost of £23 billion. Dept Work and Pensions

What is housing benefit?

Housing benefit is a means tested benefit paid to the unemployed and low paid to help with the cost of rent. For a family living in a large four bedroom house – housing benefit can be up to £400 a week. (Housing Benefit.gov.uk)

The aim of housing benefit is to help those on low income afford their housing costs.

It is particularly important for areas of high housing costs, such as London. Without housing benefit, there would likely be a shortage of workers because people would have to move away to cheaper areas.

Housing benefit helps to reduce inequality and relative poverty by helping people with their major living costs.

Housing benefit can help avoid homelessness by giving people help with housing costs.

Housing benefit can be claimed with other benefits, such as unemployment benefit and tax credits.

Whether you are eligible and the amount you get is determined by a local authority housing allowances (LHL)

Source: Single Housing Benefit Extract (SHBE), via Stat-Xplore

Of this 4.93 million

1.28 million are over 65.

468,000 are receiving job seekers allowance

3.3 million are in the social rented sector. 1.6 million are in the private rented sector

The biggest area for receiving benefits was London with 835,000.

The great recession of 2008-2014 saw a marked rise in the numbers eligible for housing benefit. The numbers claiming housing benefit peaked at just over 5 million in early 2014. In Aug 2014, 4.93 million received housing benefit.

The rise in numbers claiming housing benefit is due to factors such as:

Fall in real wages causing more people to be eligible for income related means tested benefits.

Rise in unemployment during the great recession, which significantly reduces income.

Readers Question: What policies could be used to ease pressure on housing market?

Firstly, the main pressure in the UK housing market is the persistent and continued above inflation price increases. Back in 2004, Kate Barker’s report into housing market trends found that the UK would need to build 250,000 houses to reduce the house price inflation rate to 1.1%. But, since 2004, the UK housing market has fallen short of this target. In the middle of the recession, the number of home starts fell to just over 100,000. (Housing supply)

The Home Builders Federation claim to catch up, we would need to increase home building to 320,000 a year – something not seen in the UK since the 1950s.

Policies to ease pressure on housing market

1. New Garden cities The building of new cities, in the mode of Milton Keynes, can enable a significant increase in homes. Currently there are plans for a new city in Ebbsfleet, Kent on the high speed railway line to London.

However, from planning to completion this will take a long time. It also means building on greenbelt land, which is likely to raise objections.

2. Government subsidy / council homes. Additional government spending to subsidise the building of ‘social’ housing could help increase supply. In the past decades, council housing has fallen out of vogue as the government have sought to sell off council housing and cut back on the building of council housing. But, it was council houses which provided a significant boost to the UK’s housing stock in the post war period.

Clement Attlee’s post-war Labour government built more than a million homes, 80% of which were council houses. In recent years, local authority building of new houses has virtually ceased. It is notable that since local authorities ceased to build homes, the UK housing shortage has become more acute. Housing associations have never been able to replace the large numbers built by local authorities.

It would require a change in political commitment and the willingness to spend extra money. Also, since the Thatcher era, the notion of council housing has gained a form of social stigma. However, it could make a big difference to the number of homes built.

3. Greater flexibility in planning. Planning restrictions are quite strict in the UK. Loosening the number of restrictions and making it easier for builders will make supply more elastic. This could involve reducing the amount of protected greenbelt land. It could also involve streamlining the regulations home-builders have to meet.

However, this could lead to significant local objections as people protest about the increased building, congestion and loss of green fields. One other solution would be to provide grants for turning derelict brown field sites into new homes.

4. Incentives for local authorities

Home building is a local issue. Local authorities have to deal with opposition to home building, so there is often local political pressure to stop house building. However greater financial incentives, such as allowing the council to keep council tax receipts from new housing developments, could give them a greater motivation to allow home building.

5. Introduction of a Planning-gain Supplement scheme

At the moment, building new houses tends to give the greatest benefit to landowners. Local residents feel they just lose out – depressed house prices, loss of unique village e.t.c. One solution is to make sure local residents near new housing schemes gain some compensation in return for accepting more houses. For example, a new housing development could be accompanied with a bypass or better public transport links. This is interesting from an economic perspective as it is seeking to provide a pareto improvement (one where everyone benefits).

The difficulty is that in the real world, it can be difficult to ensure people are compensated. Some local residents may feel there is nothing to compensate for the loss of a beautiful view. People may also exaggerate how much they lose from a new housing scheme.

6. Government’s Help to to buy

The government’s help to buy scheme is controversial because it is seeking to ease the problem through helping homeowners borrow more money. Critics argue this merely fuels demand and keeps prices artificially high.

However, to some extent, the Help to Buy scheme has provided some incentive for private builders to increase supply. In particular the first part of the scheme which offers buyers an interest-free loan worth up to 20% of the value of a new-build home. This increased demand for new build homes, encourages house builders because they are more confident there will be demand for the new homes.