The UK recovery paints an unusual situation. We have both positive economic growth and falling real wages. How can we have economic growth with falling real wages?

Real wages are not the only source of economic growth. We can see growth from other components of AD –

I (Investment), G (Government spending) plus net exports (X-M)

Also, it is possible for consumer spending to rise despite falling real wages (at least in the short term). For example, if spending is financed by borrowing or declining savings ratio. Consumer spending could also be financed through re mortgaging houses (equity withdrawal) against the backdrop of rising house prices.

Economic growth in the UK

Since 2013 Q1, we have seen a decent rate of economic recovery. In the past 12 months – between Q2 2013 and Q2 2014, GDP in volume terms increased by 3.2%

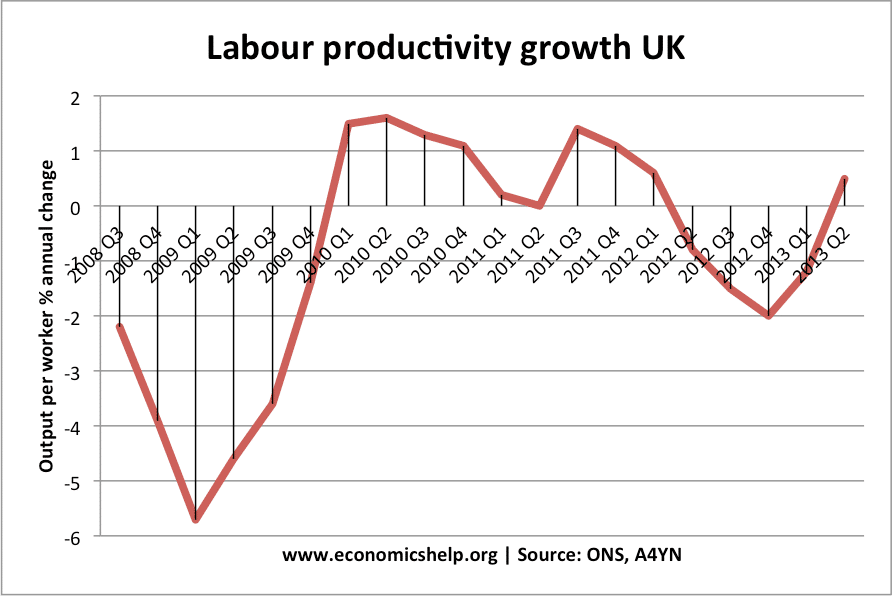

Real wages

Real wages have been falling since the start of the great recession in mid 2008. In a recessing falling real wages are to be expected, but since the recovery, we might have expected real wages to match the growth in real GDP.

Why are real wages falling despite economic growth?

1. Flexible labour markets creating low paid employment. In this recovery, unemployment has fallen more rapidly than previous recessions. Evidence suggests the economy has been successful in creating new employment (often temporary / part-time/ self-employment). These new jobs are not particularly well paid. The recovery is good for job-seekers, but less good for those already in work. The relatively elastic supply of labour willing to take low paid jobs is keeping any wage growth low.

Readers Question: Seeing the recent releases of positive UK data come through, I’ve been thinking whether these are signs of a recovery or it is too soon to say. To what extent is the recent run of positive data across sectors a sign of a balanced & sustained recovery in the UK? (question 7th. Nov)

It is a good question. If we look back to 2010, there were signs of economic recovery, but this was not sustained – with the economy going back into recession. In 2013, the evidence is mixed though a little more hopeful. In summary, the UK economy recovery is being primarily driven by consumer spending, the service sector and a vibrant housing market (especially in London). There is weaker growth in manufacturing, exports and investment. The economy is also being helped by ultra-loose monetary policy (Q.E. and zero interest rates). Fiscal policy is more neutral, though over the next few years, the government plans to restrict the growth in government spending so this is liable to be a drag on growth.

These blog posts are also relevant to this question:

A key feature in the nature of the recovery will be the health of the banking sector. The sharp fall in bank lending was a major factor behind the prolonged recession of 2008-12. Signs of improved bank lending will help the economy. However, although mortgage lending shows signs of growth, this is less helpful than bank lending to business. For sustained recovery, increased mortgage lending and squeezing house prices higher is not particularly helpful. Squeezing house prices higher through increased mortgage lending is not increasing productive capacity. If anything rising house prices in London are reducing geographical mobility and the cost of housing in London will adversely hurt the London labour market. Also, house price to income ratios (especially in the south) are close to historical highs; some fear house price growth is unsustainable. Any fall in house prices would knock consumer confidence and spending.

Real Wage growth

In 2013, there has been growth in consumer spending, but this has come despite slow growth in real wages. A feature of the prolonged recession has been very low / zero nominal wage growth. This means, combined with inflation above the government’s target, many consumers have seen a prolonged fall in real wages. With stagnant real wages, there is a limit to how much consumer spending can lift the UK economy. A sustained recovery will need a return to real wage growth. This may come if inflation falls and firms feel more profitable and able to increase wages. Real wage growth will also require a change in the UK’s very poor productivity growth rate over the past five years.

GDP statistics

Firstly, the latest GDP statistics (preliminary from Q3 2013) were promising:

In particular, data from Q3 suggested growth across the main industrial sectors of the economy.

In output Q3 compared to Q2, output increased by 1.4% in agriculture, 0.5% in production, 2.5% in construction, and 0.7% in services. This was a rare sign of a more balanced growth. Future growth figures are also looking more optimistic, with analysts predicting strong growth in the next quarter.

But, we always need to add a disclaimer to be wary of quarterly statistics. Firstly, we have to be careful about inferring too much from quarterly economic statistics (especially provisional figures which could be revised up or down later) If one swallow doesn’t make a summer, one or two positive quarterly growth figure don’t overcome a prolonged economic stagnation.

Growing current account deficit and weak exports

Ironically, one day after asking this question, data on exports and the current account deficit was disappointing – raising concerns that the UK recovery was still fragile and unbalanced.

There are different ways of looking at the UK recovery. Firstly, we can look at the damage done to the economy since the peak in 2008. The black lines suggests a possible pre-crisis trend rate of economic growth. A rough rule of thumb, suggests that had economic growth been maintained at the pre-crisis trend rate …

The UK economy has experienced the most prolonged decline in real GDP on record. GDP is still lower than before the start of the great recession in 2008. This unprecedented recession has been prolonged – despite a sharp depreciation in the Pound, and a raft of unconventional monetary policies. However, recent statistics suggest there are some reasons to be more hopeful and the UK economy is starting to recover. Yet, despite the recovery, many analysts still worry that the economy is unbalanced and could be vulnerable to a further economic downturn in Europe and the rest of the world.

The UK recovery since 2009 is best described as ‘patchy’ The important thing is to maintain recovery for a prolonged period and not slip back down into recession. The governor of the Bank of England recently talked about the need for the UK economy to reach ‘escape velocity’ – this means a recovery strong enough for the recovery to be self-maintaining – without the artificial props of quantitative easing e.t.c.

Where is the recovery coming from?

1. Retail spending. Although real incomes remain depressed, retail spending has shown renewed strength. Compared with a year ago (July 2013 compared with July 2012) the quantity bought in the retail industry increased by 3.0% (ONS). Consumer spending accounts for approx 65% of UK GDP and so is the most important component. A rise in consumer spending is good because it shows a renewed confidence about the economy. However, at the same time, it raises concerns. The growth in consumer spending is partly financed by a fall in the savings ratio, it isn’t being met by growth in real incomes. Therefore, there is a danger the UK recovery is falling into the old trap of being unbalanced and relying on consumers dipping deeper into their pockets (and credit cards)

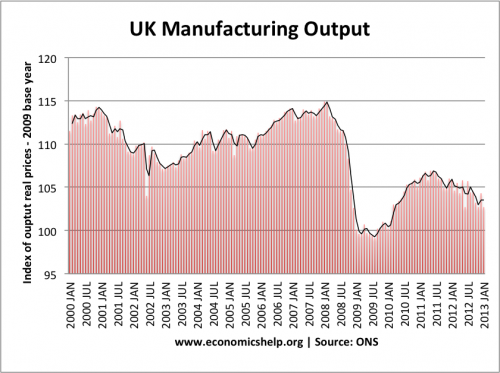

2. Manufacturing. For a long time, manufacturing has been the struggling sector of the UK economy. The weakness of manufacturing is one factor behind the UK’s persistent trade deficit, but recent evidence is more promising. This week, the PMI survey for the manufacturing sector found the strongest growth in activity for two and a half years, with output and new orders rising at their fastest rate for 19 years. However, although this sounds impressive, it needs to be remembered manufacturing output is still 11% lower than it pre- 2008 peak.

– a long way to recovery.

Construction has also seen growth in the first part of 2013, but, this is from a very weak base, and construction output is still down 0.5% on a year ago. (ONS)

3. Exports to emerging economies. In 2013, we have seen strong export growth to emerging economies. Exports to BRIC countries have performed well. Exports to China have risen nearly sixfold since 2002.

In one sense, these export growth to new markets is encouraging. With Europe stuck in recession, it is good news the UK exporting sector has been able to diversify into emerging markets, which perhaps have greater potential in the long term. However, there have been increasing concerns that the long boom years for China and India may be coming to an end. This would dampen growth in these new export sectors. Also, it is still a small share of GDP for the UK economy.

4. Housing Market. Another staple of the UK economy. A renewed rise in house prices is a mixed blessing. The rise in prices will encourage consumer confidence and improve the balance sheets of banks. It has also encouraged renewed activity in the construction sector. However, house prices are already stretched, with house price to income ratios close to all-time high. Rising house prices as the main source of economic recovery is another sign of an unbalanced economy.