The European Union is facing the prospect of a serious bout of deflation (or at least, very low rates of inflation / disinflation) Deflation occurs when prices fall. But, very low rates of inflation are considered to raise problems associated with deflation.

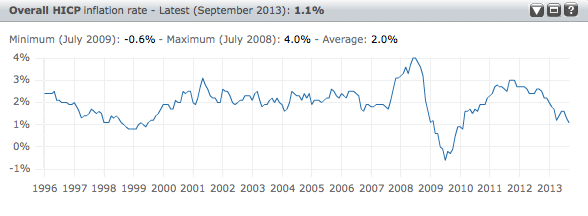

In the Eurozone, the main index of inflation has fallen to 0.7% – This is well below the ECB’s inflation target of 2%. Some regions and countries in the Euro, such as Greece are already experiencing deflation. In Greece prices fell 1.8% last year and the consumer price index reached the lowest level for 51 years (FT Link). Spain and Italy in particular, are nervous about the prospects of experiencing deflation in the future.

Inflation ECB – Inflation has since fallen to 0.7%

Causes of deflation in Europe

1. Unemployment. Unemployment in Europe has increased significantly since 2008, with the unemployment rate now reaching 12.2%. High rates of unemployment put downward pressure on wages, as the unemployed are more likely to accept lower wages.

2. Internal devaluation. A striking feature of the Euro is that countries which became uncompetitive in the boom period, can not devalue their currency to regain competitiveness. Therefore, the only option is for them to pursue internal devaluation. This means reducing prices and costs in the economy – primarily cutting wages. By reducing costs, they can make their exports more competitive and regain competitiveness. But, with weak external demand, it is proving a difficult and slow process for southern Europe to restore competitiveness compared to northern Europe.

3. Weak demand. The fundamental cause of deflation is weak demand within the Eurozone. Firstly, several Eurozone economies are pursuing fiscal austerity to try and reduce budget deficits. These spending cuts and tax increases are causing a significant drop in demand. Because of the relatively tight monetary policy, and strong Euro, demand is not coming from other sectors of the economy.

4. Fear of inflation in Germany. With inflation falling to 0.7% and unemployment of 12%, you would expect economists to be unanimous in the desire to overcome the threat of deflation and promote growth in Europe. But, in Germany the prevailing economic orthodoxy is still to worry about inflationary pressures and a possible loss of ‘confidence’ – should the ECB promote monetary loosening. Recently The ECB cut interest rates by 25 basis points, after the fall in inflation rate from 1.1 to 0.7%, but several Germany economists dissented arguing that it is wrong to cut interest rates given the possibility of ‘inflationary’ pressures in Germany. In the past, Angela Merkel has argued that Germany would need an interest rate increase if the German economy was taken in isolation. (FT link) The underlying fear of inflation means there is tension within the ECB and a reluctance to loosen monetary policy to target deflation.

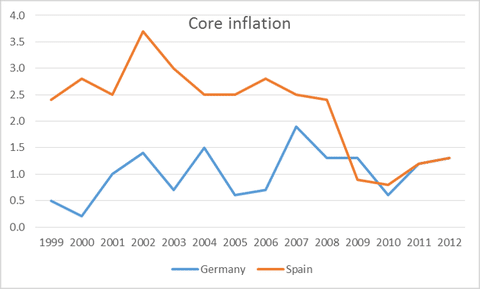

Source: Eurostat: via Krugman

This graph shows that since the introduction of the Euro, inflation in Germany has been nearly always less than an inflation target of 2%. It also shows that when Germany grew strongly in the early 2000s and increased it’s current account surplus, it benefited from strong demand in the south of Europe (who experienced higher inflation). Now southern Europe is trying to recover, but without a corresponding loosening of monetary policy and higher demand in the north.

5. Imbalance in demand

In recent years, Germany has increased its current account surplus because it has had lower inflation and growing competitiveness. Southern Europe, by contrast, are trying to regain competitiveness. But, German domestic demand is still weak. This means southern Europe are finding it difficult to increase their exports. By maintaining a large current account surplus, Germany is effectively, limiting overall demand in Europe. There are other factors behind the German current account surplus, but some within the EU are concerned at the lack of German demand for the rest of Europe. (Turning German Current account surplus into win win for EU)

6. Rising real interest rates. With inflation falling, the real interest rate is rising. Although the ECB cut interest rates by 25 basis points, this is smaller than the fall in inflation. The net result is that effective real interest rates have risen. This will depress investment and spending further, creating a negative downward spiral. Also, in many European economies, effective bank rates are significantly higher than the ECB base rate. Firms are finding it expensive and difficult to get credit – despite official rates being very low. (See: credit policy)

7. Relatively strong Euro. Because the ECB are taking a hawkish view on inflation and being reluctant to take more aggressive monetary action, the Euro is strengthening. The approach of the ECB contrasts with the UK, US and Japan, who have all taken action to increase their money supply – which has the side-effect of reducing their currencies. It means that the Euro has attracted capital flows. This strengthens the Euro and makes Euro exports relatively more expensive.

8. Global inflation is falling. In recent months, global inflation has fallen due to weaker commodity price growth. Also there are signs of over capacity in many large manufacturing sectors. Chinese and investment has increased capacity, but given weak global growth, there is now growing spare capacity, which is putting downward pressure on the price of goods. (see: tablet market for one example of falling prices)

9. Debt deflation dynamics

With very low inflation, and economies stuck in recession, nominal GDP in the EU is growing very slowly or even falling. This means that countries are facing rising debt to GDP ratios – despite the austerity measures. Therefore, there is a strong deflationary pressure coming from rising debt burdens in both private and public sector.

Related

2 thoughts on “Causes of Europe’s deflation problem”

Comments are closed.