Between 2009 and 2015, the Bank of England has been authorized to create £375bn of assets by the creation of central bank reserves. This new money was used to purchase government gilts.

The Bank of England’s holding of gilts. More on Bank of England’s asset purchase scheme at B of E

The theory is that by creating extra money and buying gilts from financial institutions, there would be an increase in the money supply and increase economic activity.

Quantitative easing is an unorthodox monetary policy aimed at stimulating economic growth and preventing a fall in the money supply. Just to recap, Q.E. involves:

Central Bank creating money electronically.

Using this extra money to purchase government bonds (and other securities) from banks and financial institutions.

Q.E aims to:

Increase bank liquidity. When commercial banks sell bonds to the Central Bank, they have an increase in their cash reserves. This increase in cash deposits should, in theory, encourage commercial banks to lend to businesses.

Reduce interest rates. Through buying government bonds, the market price of bonds rises, leading to a reduction in long-term interest rates. Lower interest rates should, in theory, encourage greater economic activity in the economy.

What happens when quantitative easing ends?

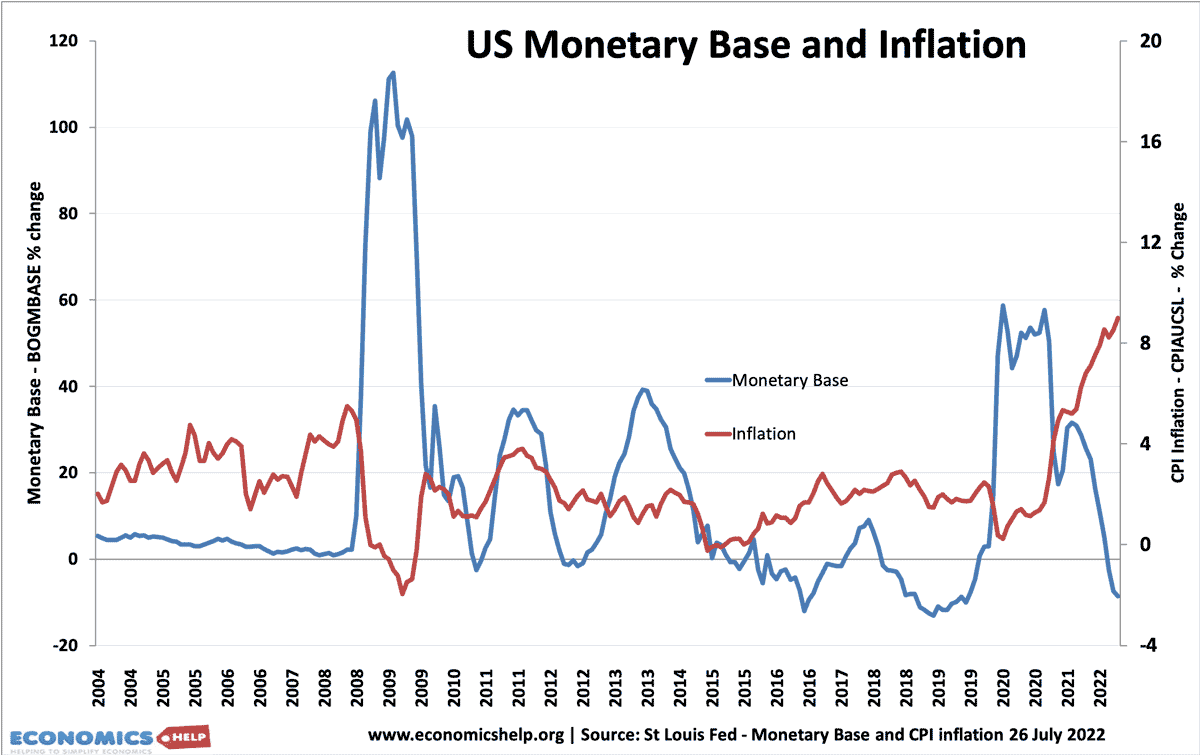

There will come the point when increased economic activity means the Central Bank no longer feels the need to buy more securities. At this stage, the increased money supply from quantitative easing may be inflationary because, with increased confidence, the banks now start to lend the cash that they have previously been hoarding (saving). (though there is no sign of this occurring yet)

Reversing Quantitative Easing

At some point, the Bank of England will reverse the policy of quantitative easing. This involves selling the government bonds it holds on the open market. This will cause:

A fall in the price of bonds, due to increased supply on the market.

As bond prices fall, the bond yield will increase. Therefore, we will see rising interest rates.

A decrease in cash reserves in banks. If banks buy government bonds, they will have a fall in their cash reserves; this could lead to a fall in the money supply, lower growth and possibly even deflation.

So will we get inflation or deflation when quantitative easing ends?

We don’t really know.

If the Central Bank extends too much extra money and allows this extra money to stay in the economy during a strong recovery, then it is likely to contribute to inflation.

If the Central Bank reverse quantitative easing too early – if they reverse quantitative easing when the economy is still in a liquidity trap / stagnant growth, then it could cause the economy to stagnate further. If quantitative easing is reversed when the economy is still weak, we could see deflationary pressures.

Therefore, the timing of quantitative easing becomes important. The hope is that the process of quantitative easing can be gradually reversed during a sustained economic recovery. Obviously, the Bank will not want 10-year. But, if it can sell £20bn every couple of months, the policy may be reversed without causing too much impact on the macroeconomy. If the economy is growing strongly, then the reduction in money supply and higher interest rates from Q.E, will be absorbed.

The other reason why it is hard to know what happens when quantitative easing ends is that it’s hard to know if quantitative easing has had much impact on stimulating the economy in the first place.

Readers Question. Just saw a video called ‘How to waste £375 billion? (The Failure of Quantitative Easing)’ by Positive Money. I’ve recently started reading your blog and find your posts very informative. I wonder what you make of the ideas in this video and of this group in particular?

(I haven’t seen the video. For some reason I never like watching videos only reading articles.)

I would say Quantitative easing has been a quantified success. Or perhaps a better way of evaluating quantitative easing is that – it could have been worse, if we hadn’t pursued quantitative easing.

A simple comparison is to compare the UK and US (who have both pursued quantitative easing) with the Eurozone (which hasn’t). In the past couple of years, the economic recovery has been stronger in the US and UK, the Eurozone is in danger of a double dip (or triple dip) recession. The Eurozone is heading towards a dangerous period of deflation. The UK and US have at least a better inflation rate.

Eurozone inflation

Therefore, I wouldn’t say we wasted £375 billion. Firstly, ‘wasting’ implies an opportunity cost – for example, finding it from higher taxes or lower spending. It was entirely created. For all its faults and limitations, the quantitative easing we pursued was better than nothing – especially given the degree of fiscal tightening pursued since 2010.

Problems with UK Quantitative easing

Perhaps a better description of UK quantitative easing is a wasted opportunity. True, we avoided some deflationary effects, but there are reasons to be disappointed and perhaps it could have been better.

Banks largely used the newly created money to make a profit from selling bonds to the Bank of England and improve their balance sheets; because of the recession, little of this extra money fed through into the real economy through higher bank lending (see: M4 lending stats). The side effect was some banks and the bond market did very and interest rates are at very low rates. True, low rates are part of the aim behind Quantitative easing, but low interest rates are of limited benefit, if firms are unable / unwilling to borrow and make use of cheap borrowing.

Parts of the financial services industry has benefited very well from quantitative easing. It is perhaps a little galling to see many of those culpable for aspects of the credit crisis gaining bonuses from the benefits of quantitative easing.

However, to say it solely benefited the rich is to ignore the contribution it may have made to reducing unemployment. UK unemployment has fallen for many reasons – the small economic stimulus is an important factor – never forget reducing unemployment is one of the most important factor in reducing relative poverty. The UK unemployment rate is now 50% lower than many areas in the Eurozone.

Would a better form of quantitative easing have been to print a smaller amount of money, but directly use this to finance government budget deficit, and / or fund public sector investment?

Some argue this would have directly led to higher demand and a stronger economy.