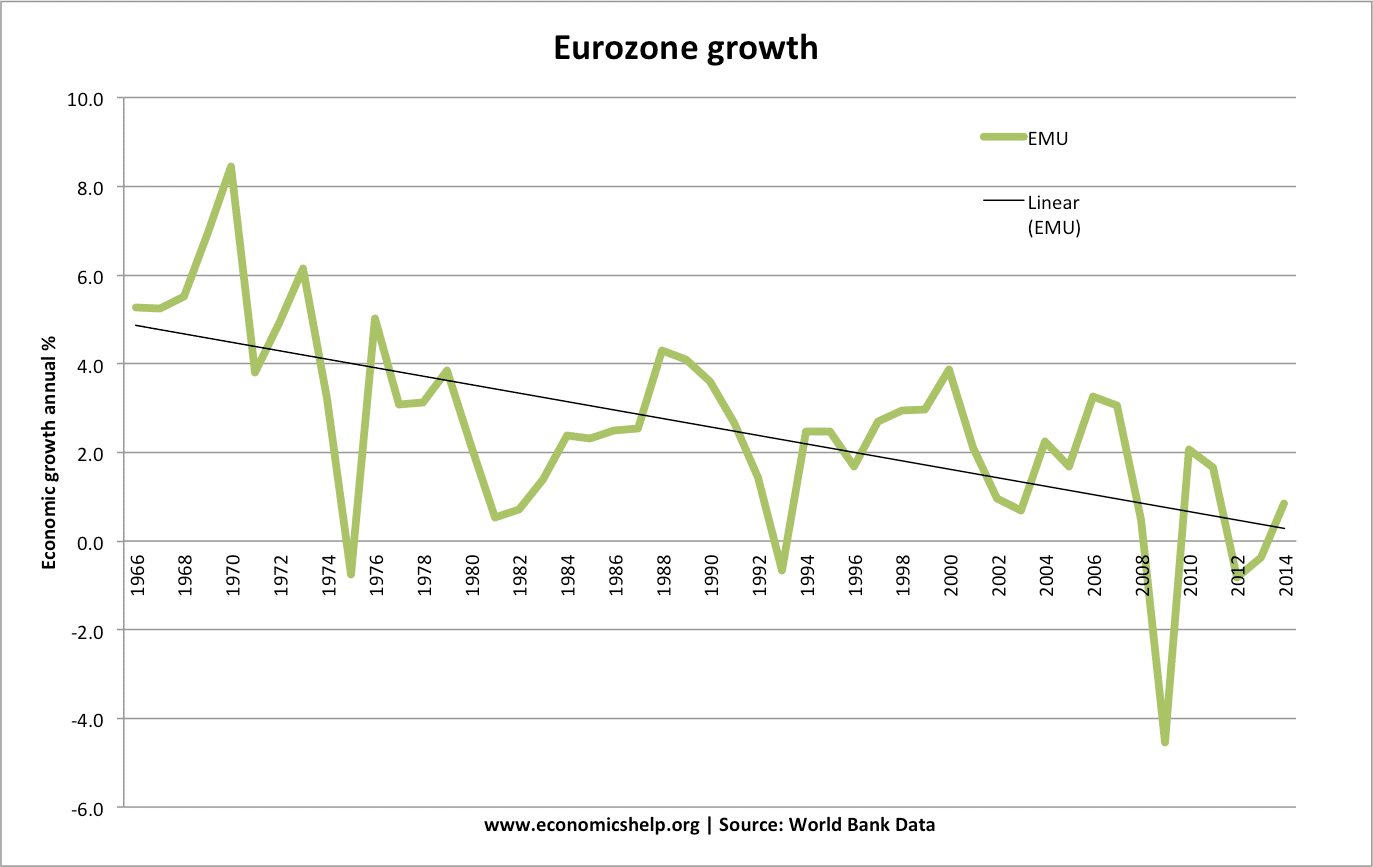

The great recession refers to the economic downturn between 2008 and 2013. The recession began after the 2007/08 global credit crunch and led to a prolonged period of low/negative growth, rising unemployment and a period of fiscal austerity. In particular, the great recession highlighted problems within the Eurozone which experienced a double-dip recession and high unemployment.

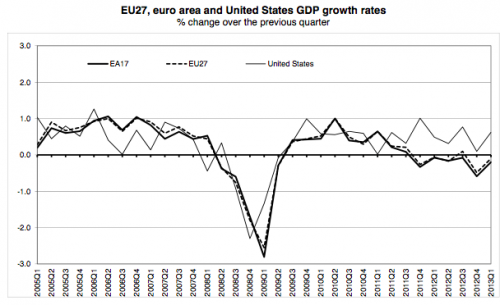

Recession in US and EU. Source: Eurostat

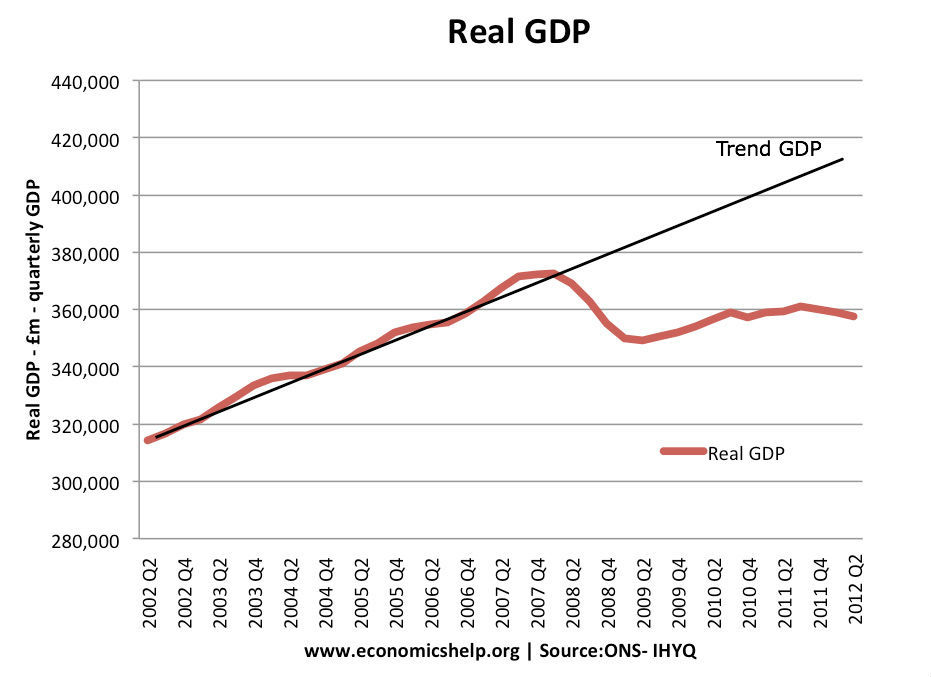

Output gap

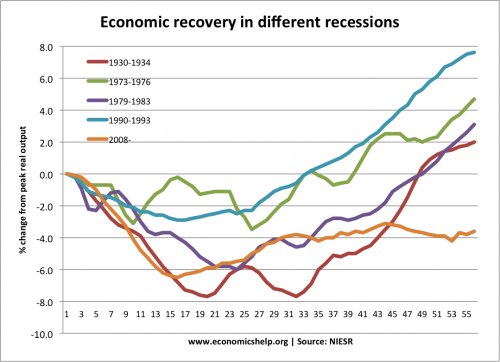

Graph showing how much real GDP fell behind the trend growth in the UK. Unlike previous recessions, the economy did not catch up the lost output.

Causes of the great recession 2007-08

The primary cause of the great recession was the credit crunch (2007-08) where the global banking system became short of funds, leading to a decline in confidence and decline in bank lending. The causes of the credit crunch were quite complicated but in summary.

- In 2000-2007, US banks made a big increase in sub-prime mortgage loans. These mortgages were very risky, but there was a good deal of ‘irrational exuberance‘ and belief house prices would keep rising.

- US mortgage companies sold these ‘risky mortgage bundles’ on to banks around the world. (Credit rating agencies gave them AAA ratings – despite the fact they were very risky.)

- Starting around 2005, US interest rates rose, and homeowners in the US began to default on these risky mortgages.

- US banks lost money, but also banks around the world later realised the ‘safe’ mortgage bundles they bought were actually useless. So many banks around the world saw a big fall in liquidity and value of their assets.

See more at: Credit crunch for a more detailed account

The recession was also caused by

- Credit crunch led to a fall in bank lending, due to a shortage of liquidity.

- Fall in consumer and business confidence resulting from the financial instability.

- Fall in exports from the global recession.

- Fall in house prices leading to negative wealth effects.

- Fiscal austerity compounded the initial fall in GDP.

- In Europe, the single currency created additional problems because of over-valued exchange rates, and high bond yields.

More details on causes of great recession

- Great Moderation. The period 2000-2007 was a time of strong economic growth, low inflation and falling unemployment. Central Banks appeared to be successful in targeting low inflation and ensuring economic stability. However, underneath the macro-economic stability, there was growing instability regarding credit and financial markets.

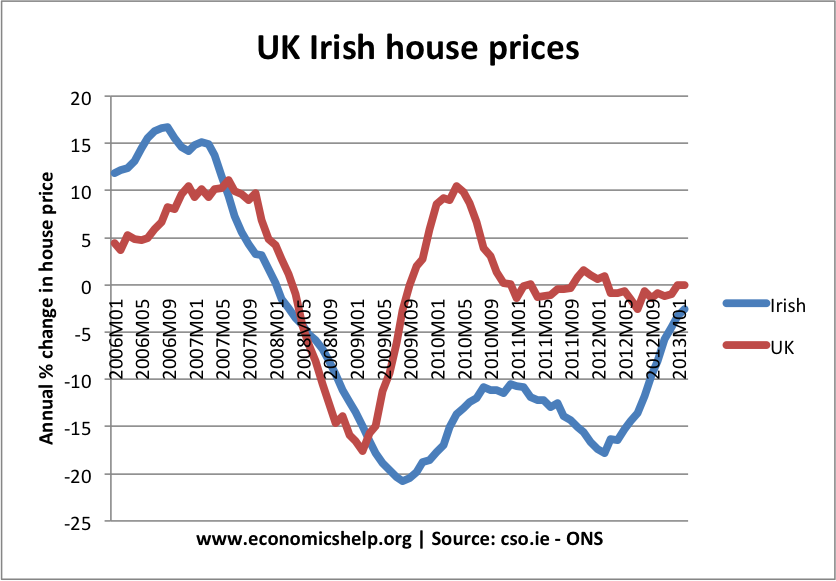

- Housing bubble. Many countries experienced a rapid growth in house prices. House price rose faster than inflation and faster than incomes. This boom in housing was encouraged by a growth in bank lending and high confidence. Several countries, such as Ireland and Spain also experienced a boom in house building.

Irish and UK housing price fall in 2008.

Irish and UK housing price fall in 2008. - Bad loans. In the period leading up to the credit crunch, banks became more aggressive and willing to take risks in lending. Especially in America, banks and mortgage companies loosened their criteria for giving mortgages. Many homeowners were given large mortgages, with limited checks on their ability to repay. However, in the economic downturn, people were left with mortgages they couldn’t afford.

- Bad loans repacked and resold. These ‘bad’ mortgage loans were sold onto other financial institutions around the world. For example, many UK and European banks bought these mortgage bundles from the US (CDOs) and so were exposed to any potential losses in the US housing market.

- Housing Bubble Burst. In 2006, the US housing market bubble burst. House prices started to fall, and there was a rise in mortgage defaults. Banks began to realise they had lost significant sums of money through the US mortgage defaults.

- Banks short of liquidity. The scale of bank losses started to increase and it became harder for banks to borrow money on money markets. This caused banks to reduce loans and mortgages. Because banks were losing money, it became challenging to get credit and liquidity. Some banks lost so much they were running out of money. In several countries, such as UK, Ireland and US, major banks had to be bailed out by the government. But, the realisation banks were short of liquidity harmed consumer and investor confidence. The fall in confidence led to lower spending and investment.

- Rise in oil prices. In 2008, there was also a peak in oil prices. This complicated matters because it caused cost-push inflation. This cost-push inflation made Central Banks more reluctant to cut interest rates. Also, higher oil prices reduced discretionary income and led to lower spending. Usually, in a recession, oil prices fall. However, because of rising demand in China and India, we saw rising oil prices – even as Europe and the US went into recession. High oil and commodity prices was another factor reducing demand.

The impact of the credit crunch and recession

- In 2008, all major economies experienced a very sharp drop in real GDP. The banking crisis severely curtailed normal bank lending. The result was a fall in investment and consumer spending leading to a sharp drop in real GDP.

- The fall in house prices was another factor leading to recession. In the boom years, rising house prices (and wealth) underpinned higher consumer spending. When house prices dropped, many homeowners faced negative equity. Therefore, they cut back on spending and could no longer rely on re-mortgaging to gain equity withdrawal.

- The global nature of the crisis meant that there was also a drop in world trade. Countries saw a drop in exports as the global downturn led to lower demand.

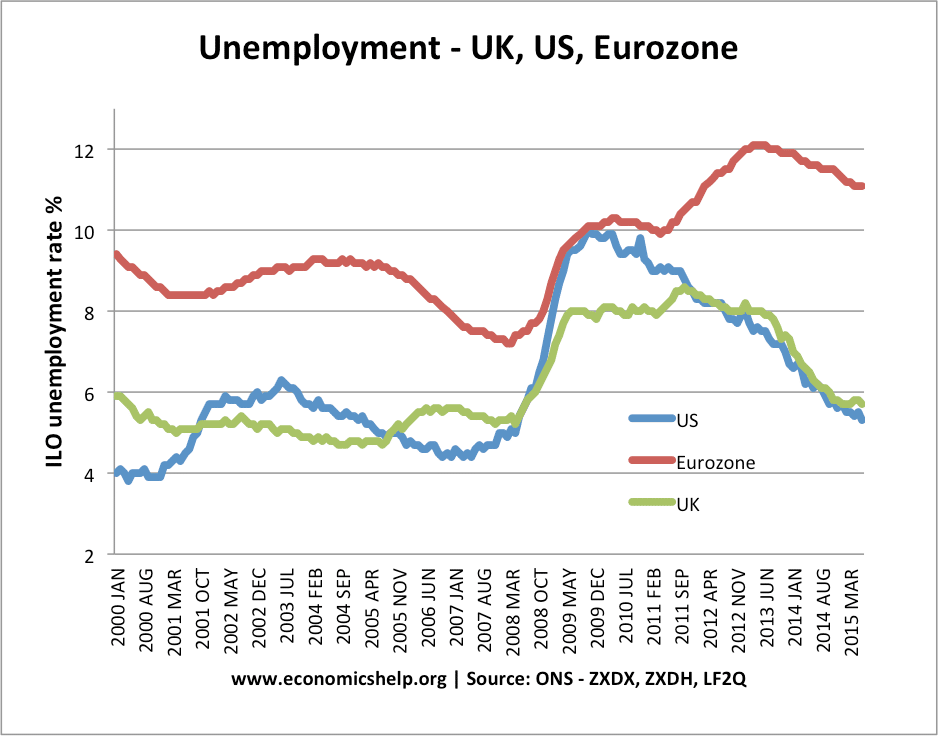

- Unemployment. Unemployment rose in US and Eurozone.

- Government debt. Government debt rose sharply due to the recession. This ushered in a period of ‘austerity’ with many governments in Europe seeking to cut spending.

- Euro crisis. The Eurozone saw a rise in bond yields in 2010-12 – partly due to recession, and also due to lack of Central Bank willing to intervene.

Response to the great recession

- Bank rescues. Firstly, governments felt obliged to intervene in the banking sector to avoid banks and financial institutions going bust. However, there was some reluctance to bailout those who were blamed for causing the crisis. In 2008, the US decided to allow Lehman Brothers to go bust. This caused a major loss of confidence. After the panic this created, governments realised they couldn’t allow a repeat of this experience. In the UK, the government intervened to bailout out major banks, such as Northern Rock, and Lloyds TSB.

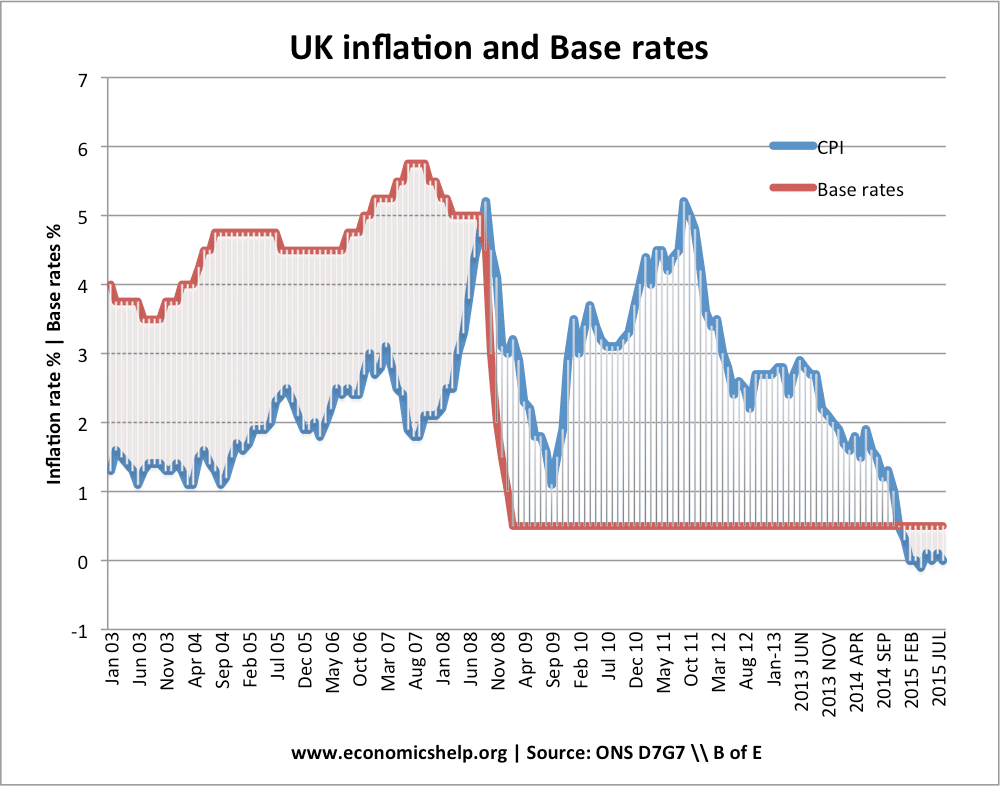

- Cuts in interest rates. Towards the latter half of 2008 and early 2009, Central Banks cut interest rates to record low levels. The UK cut base rates from 5% to 0.5%. Usually, a major cut in interest rates would make borrowing cheaper and encourage consumption and investment. (e.g. in 1992, when the UK cut interest rates, the economy recovered fairly quickly.) However, cuts in interest rates were less effective in this period.

- Expansionary fiscal policy. The deep recession saw a sharp rise in budget deficits because government tax revenues evaporated. This was particularly noticeable for countries who relied on stamp duty and tax from the finance sector. However, in the UK and US, there was a moderate degree of fiscal expansion. The UK introduced a temporary cut in VAT. In the US, there was also a moderate fiscal stimulus.

- It is worth noting that in comparison to the great depression of the 1930s, two things were avoided in the great recession.

- Large number of banks going bankrupt was avoided (In the 1930s, in the US over 500 commercial banks went bankrupt)

- There was no major trade war. In the 1930s, a tariff war developed as countries tried to protect domestic industries.

Why did normal policy fail to achieve a proper economic recovery?

The UK had the slowest recovery on record. See: Comparing different recessions

- Balance sheet recession. Firstly, the recession was very deep. Because firms, banks and consumers were highly indebted, they decided they needed to pay down debt. Therefore, this led to a significant fall in spending as they concentrated on paying off debt. In the UK, the saving rate rose from 0% to 7% in a short space of time. This can be referred to as a balance sheet recession.

- Shortage of credit. Lower base rates didn’t increase bank lending. Although Central banks cut interest rates, this didn’t translate into higher lending and investment. (an example of a liquidity trap)

- Commercial banks didn’t pass these interest rate cuts onto their consumers. Especially in the Eurozone periphery bank rates didn’t fall. In the UK, bank rates fell, but less than the cut in base rates. (bank and base rates)

- Credit remained tight. Although credit was, in theory, cheap, it was difficult to get any loan. Banks were short of cash so discouraged lending. It became very difficult to get a mortgage, so demand for housing remained low.

- Eurozone crisis. In Europe, the crisis highlighted the fact that the Greek public sector debt was much higher than previously thought. Before 2007, bond yields in the Eurozone had been very low. But, after the credit crisis and realising the true levels of Greek debt, bond yields in Europe rose rapidly. People became nervous about holding Eurozone bonds. The rise in EU bond yields created a new panic. European governments felt the necessity of cutting budget deficits (‘austerity’). This involved cutting government spending and higher taxes. However, in a recession, this fiscal austerity led to lower aggregate demand and worsened the recession. See more at Euro debt crisis

- Productivity crisis. The UK economy experienced unexpectedly low productivity growth (2007-2017). This was due to various reasons – low wage growth, flexible labour markets, limited technological innovation and investment. It suggests there is a fall in the underlying trend rate of economic growth.

Investment problems specific to the Eurozone

- In the lead up to the recession, Europe experienced a trade imbalance. Germany and some northern countries ran a large current account surplus. (The UK and US also had large current account deficit, suggesting an imbalanced economy)

- Countries in the south, such as Portugal, Spain and Greece ran a very large current account deficit. This meant the south was uncompetitive, leading to lower exports. After the crisis, these countries needed to restore competitiveness through internal devaluation – essentially lower wages. This caused lower demand and lower growth.

- No Central Bank. In the UK and US, bond yields fell during the crisis. With their own currency, they have a Central Bank willing to intervene and buy bonds if necessary, this avoids any liquidity shortages. But, in the Eurozone, this didn’t occur (at least not until late 2012). Therefore, bond yields rose, and countries felt a need to cut budget deficits quickly. The UK and US only pursued very moderate austerity in 2011/12. But, some countries in Europe, cut government spending very significantly.

- Fiscal austerity. Combined with falling private sector spending, government spending cuts caused aggregate demand to fall sharply.

- Weak monetary policy. The ECB is responsible for the whole Eurozone and is unable to target higher growth in depressed areas. The UK and US adopted quantitative easing, but the ECB is much more reluctant.

- Housing markets vulnerable. Countries like Spain and Ireland saw a boom in house building, which created a large surplus of housing. This has meant the fall in house prices was more sustained than say the UK.

- Unemployment. In southern European, countries like Spain, Greece and Portugal have experienced depression-level unemployment and falls in GDP. In Spain, Greece and Portugal, unemployment is close or above 20%. Youth unemployment is even higher.

The rate of unemployment fell quicker in the US and UK than the Eurozone. The higher unemployment in Eurozone was due to greater fiscal austerity and lower economic growth. It has also been attributed to less flexible labour markets.

The UK in the great recession

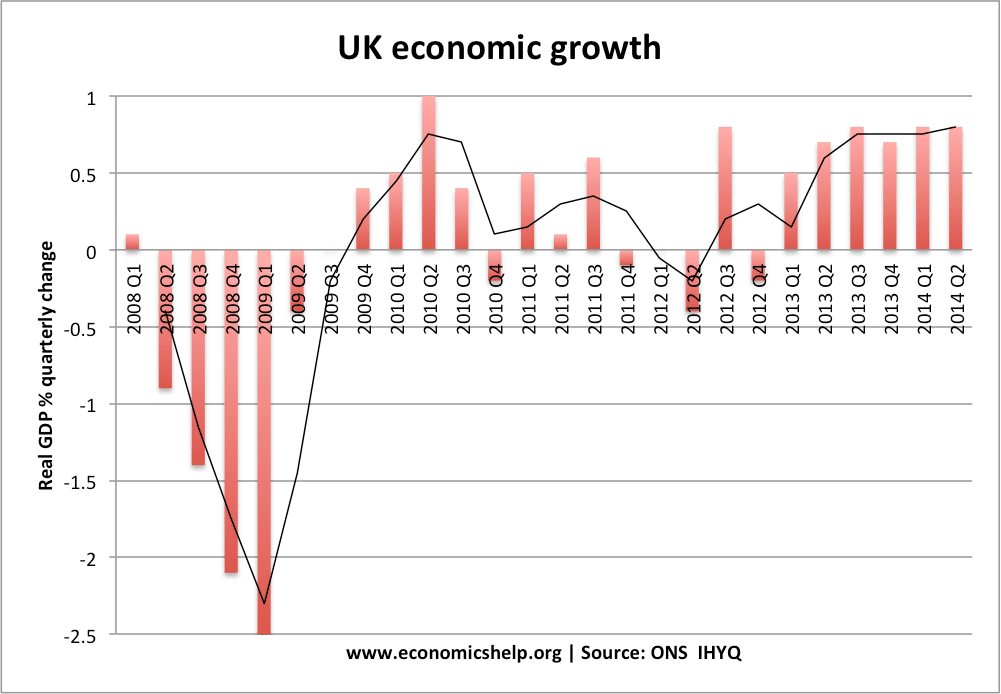

The initial recession hit the UK hard because of our relative reliance on the finance sector. The drop in GDP was longer-lasting than in the 1930s.

Despite, cuts in interest rates and large sums of quantitative easing, the UK economy stalled in 2011 and went into a double-dip recession. Some felt that the government’s austerity drive of 2010-12 was a significant factor in causing this double-dip recession. Although spending cuts were relatively mild, there was also an adverse impact on confidence. However, unemployment rose less than might have been expected (UK unemployment mystery) Most economists feel that the UK experience would have been worse, had we been a member of the Euro.

- Bond yields would have been higher. No Central Bank to act as lender of last resort.

- There may have been pressure for much deeper austerity.

- We couldn’t have benefited from 20% devaluation in Pound.

- Interest rates would have fallen more slowly.

- Less scope for quantitative easing and funding for lending scheme.

However, the UK economy is still reliant on exports to Europe and a continued EU recession is a factor in slowing UK growth.

See: Economic record of UK 2010-16

Related

As always a very clear and useful article.

Do we know what the position of UK banks actually is? Also how important is the loan deposit ration (Greg Pytel makes much of this). Is it correct that banks are still lending more than 100 percent of deposits? Is it not a simple mathematical fact that this cannot be sustained?

Not really. It’s hard to find data on things like that.

….and the loan – deposit ratio?

You are more than welcome to read my research

The great recession of 2008 caused a significant impact on economies across the globe. The recession associated itself with high rates of unemployment, reducing Gross Domestic Product of economies, and posing high inflation rates. During a decline in economic performance and a drop in the stock market accompanied by unemployment and a reduction in the market for houses, a country experiences a recession. During the recession period, much blame is put on the governance and the administration as a whole. Heads of federal reserves also become responsible in these scenarios. The underpinning effects of the economic recession of nations’ productivity play a critical role in reducing the ability to utilize resources and hence creates high inflation rates adequately.

Fiscal policies involve applying government spending and tax policies to impact the country’s economy over some time. These policies provide a declarative structure that the government uses to calculate expenditure costs and the demand for resources. During a recession, fiscal policies enable governments to prioritize their capital projects and plan sustainable spending policies in the nation.

Fiscal policies for expansion enhance aggregate demand for commodities by increasing the government’s spending rate or only reducing taxes. The system can either cause an increase in consumption through raised disposable incomes obtained after reducing personal taxes, raising after-tax profits to increase investment costs, or increasing the government’s purchases through federal spending on finished products and services.

During the 2008-2009 economic recession period, the U.S. increased its government spending. The graphical results indicated that the quantity of output was below the GDP. The increased aggregate demand resulting from the introduction of the expansionary fiscal policy moved the economy creating new equilibrium levels of the GDP(Arestis, 2012). Hence, during the 2008 Great Recession period, the U.S. incurred a loss of 3.1% of its economy, with its unemployment rate doubling from 5% to 10% in just a year(Blanchard, Jaumotte & Loungani, 2014). The expansionary fiscal policy triggered productivity by reducing taxes and increasing government spending.

On the other hand, monetary policies influence the supply and demand for money obtained by collecting interest rates. They also involve open market operations as well as quantitative easing. The country’s central bank usually creates monetary policies. Monetary policies have a significant effect on lending and mortgages(Summers, 2015). When applying the financial system, homeowners incur high-interest rates, unlike those who benefit from the savings. The above policy has a limited impact on the supply-side of the economy.

Monetary policies used in the Great Recession period of 2008 involved cuts in interest rates and stimulated nations’ spending and investment. Upon its application, the system weakened the exchange rate to aid exporters in responding to the rising demand for commodities during this period. The step enabled the economy to stir up growth. According to the Keynesian model, money supply in the economy and the aggregate GDP have an indirect link(Hammes, 2015). He asserts that when an expansionary monetary policy is in place, the banking system increases the supply for payable funds, resulting in a fall in interest rates.

Conclusion

The global recession of 2008 was unique with the initial classical view of addressing unemployment through the labor market being challenged with the Keynesian model that emphasizes the impact of demand-side policies to spur economic growth. As outlined in the model, the fiscal policies demonstrated the ability to influence economic growth during the Great Recession. These policies acted as a stimulus package to prevent the economy from dropping during the 2008 period. Lowering interest rates and increasing government spending enabled many nations, including the U.S., to increase their GDP and reduce employment rates during the recession.

References

Arestis, P. (2012). Fiscal policy: a strong macroeconomic role. Review of Keynesian Economics, (1), 93-108.

Blanchard, O. J., Jaumotte, F., & Loungani, P. (2014). Labor market policies and IMF advice in advanced economies during the Great Recession. IZA Journal of Labor Policy, 3(1), 2.

Hammes, J. J. (2015). Political economics or Keynesian demand-side policies: What determines transport infrastructure investment in Swedish municipalities?. Research in Transportation Economics, 51, 49-60.

Summers, L. H. (2015). Demand side secular stagnation. American Economic Review, 105(5), 60-65.