A look at the nature of the UK economic recovery. Is the recovery sustainable? Who has benefited the most from recovery? Which groups of people have not benefited from the recovery?

In the past two years, the UK economy has posted relatively impressive growth figures.

The UK posted annual growth of 2.6% between Q3 2014 and Q3 2013. ONS

It is impressive compared to Europe, which is stuck in recession. However, the recovery is less impressive when compared to the lost output since the start of the recession and the long delay that occurred before the economy started to catch up the lost ground.

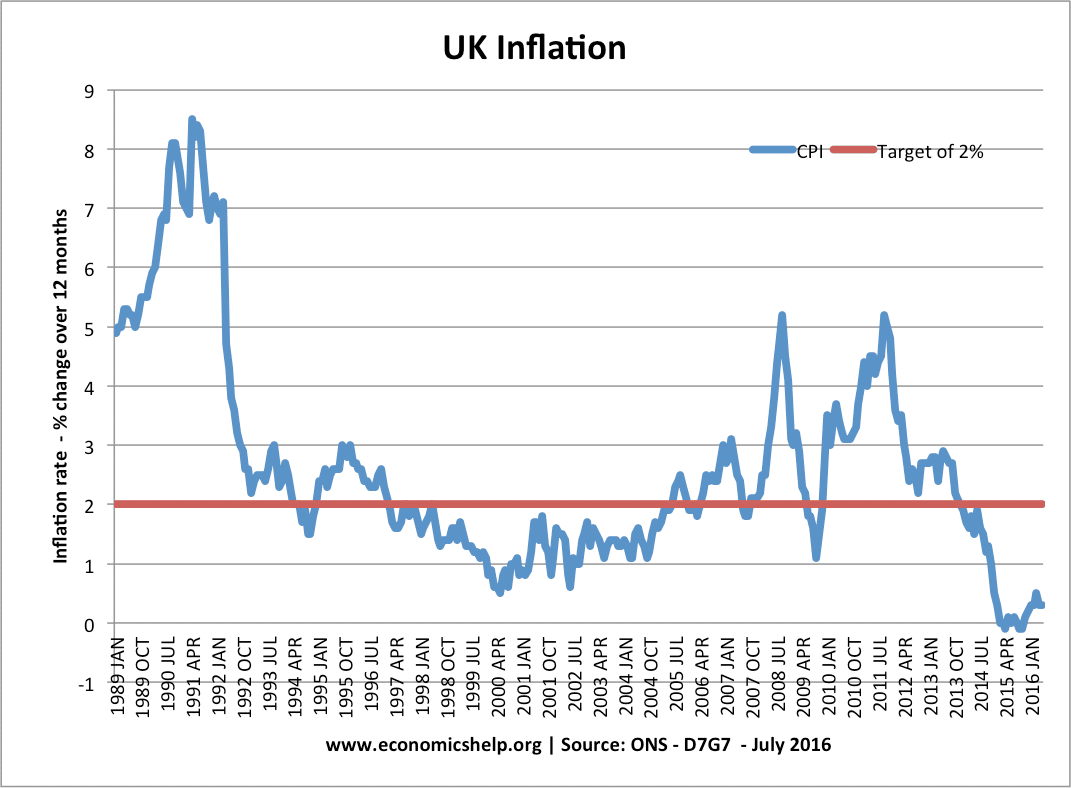

The recovery has led to a significant decline in unemployment, whilst at the same time leading to low inflation (CPI = 0.5%).

From one perspective this looks very good – the main three macro-economic objectives (growth, unemployment, inflation) are posting good statistics.

However, the UK recovery is still unbalanced and there are uncertainties about its sustainability. The main areas of concern about the UK economic recovery are:

In the UK, there are quite a few different measures of inflation. All measures seek to show the annual change in living costs. However, different measures of inflation give different inflation figures. For example, RPI can often give a higher rate of inflation than CPI. CPI can also be misleading. For example, an increase in VAT would cause CPI to increase, but a core inflation measure like CPI-CT, would stay lower

It is important to be aware of different measures of inflation because the rate of inflation has an important bearing on monetary policy.

Usually, an inflation rate of CPI 4.5% would encourage the Bank of England to raise interest rates. But, if this inflation rate was due to cost-push factors, such as higher taxes, the inflation rate may not be due to overheating in the economy.

Inflation is calculated by:

Finding out the most commonly bought goods (e.g. Family expenditure survey)

Measuring the change in prices and then applying the weight of the good to the price change.

Different Measures of Inflation

1. Consumer Price Index (CPI) – official measure. Based on the EU HCIP (Harmonised Consumer index prices)

Includes taxes.

Excludes mortgage interest payments and housing costs

Includes some financial services not included in RPI

Readers question: explain benefits of increasing rate of unemployment benefit – for the unemployed , society and any cost that may result from such policy. Current Weekly Rates of Job Seekers Allowance in UK Contribution-based JSA Age JSA weekly amount 18 to 24 up to £57.90 25 or over up to £73.10 Contribution based …

Readers question: what are perfectly flexible wage? Perfectly flexible wages are job contracts where the wage can frequently be changed. For example, if wages are determined by the income firms get – then wages are flexible – they directly change depending on price of goods. This means the wage a farm worker gets will vary …

Readers Question: Endangered rain forests, wild fish, elephants and more are examples of the tragedy of the commons. What would economists recommend to save, rain forests or fish stocks?

Pic Rainforest – CC

Firstly, the tragedy of the commons is a situation where there is overconsumption of a particular product / service because rational individual decisions lead to an outcome that is damaging to the overall social welfare.

The problem with rain forests is that people may feel an economic incentive to chop down trees in order to make a business, e.g. farming, wood for furniture. On their own – a decision to cut down a few trees don’t seem to make much difference. If you buy a table made with wood from a rainforest it doesn’t make that much difference. But, if everyone takes these decisions, we end up with overconsumption and eventually this precious resource is lost.

Economic policies to save the Rainforest

1. Laws and regulations by governments to make areas of rainforest protected.

This is the simplest and easiest. The Brazilian government can simply disallow firms from cutting down more trees, and legally protect rain forests. The problem is that governments may not want to do this because they see it as viable economic resource they need to make use of.

2. Global co-operation. If we ban cutting down rain forests, some countries may lose economically – Brazil, Indonesia e.t.c. But, the world will benefit from reduced global warming and the benefits of saving rain forests. In an ideal world, all major economies could make a financial contribution to countries who promise to save their rain forests. Therefore countries like Brazil and Indonesia don’t feel like they are losing out. All countries are paying a small amount to gain the bigger long-term benefit of saving the rain forests.

Primarily these rely on trying to change consumer behaviour. But, how could an economist make the changes more widespread and not optional?

1. “Palm oil, found in half of all processed foods in the US, is a key contributor to rainforest deforestation”

In this case we could tax palm oil which is taken from land which used to be rainforest. Increasing the price of Palm Oil, would discourage consumption and encourage consumers to buy other oils.

The problem is that individual taxes on palm oil will have administration costs. It may also be difficult to know whether Palm oil has come from former areas of rainforest. but, in theory a tax will reduce demand. The money raised could be used to buy rainforest land to protect it.

Readers question: In all the media coverage of the UK deficit / debt / recovery, two aspects are rarely highlighted / quantified / contextualized.

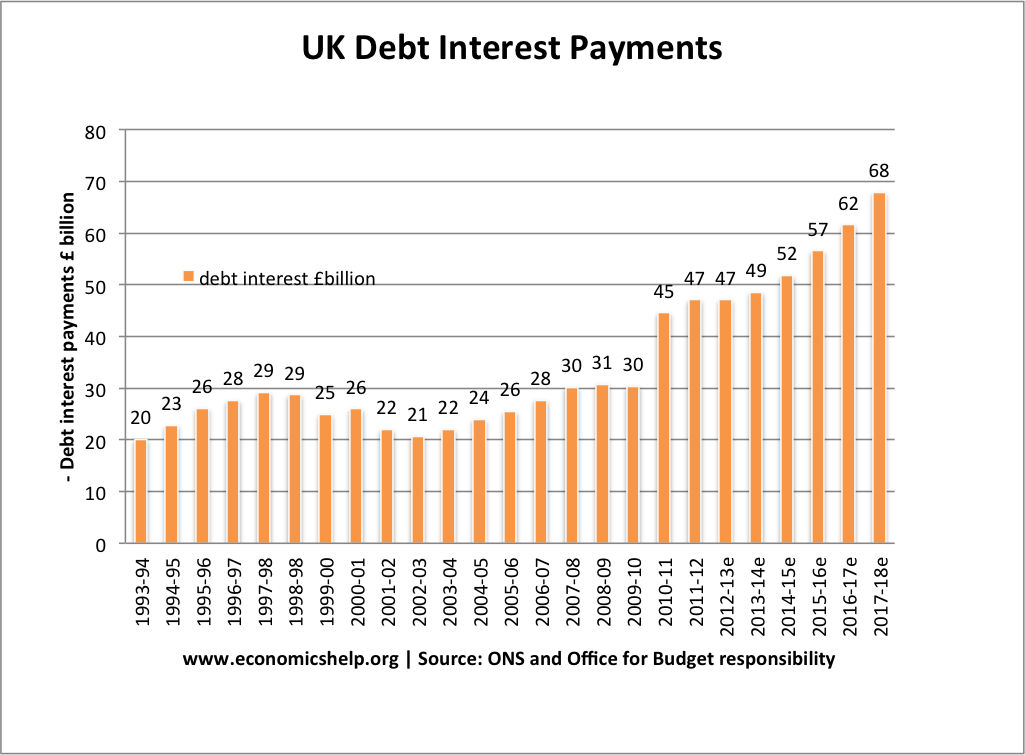

1. The £50bn interest payments on the debt (opportunity cost / %) 2. UK productivity (output per head / sector / history)

I think interest payments on debt are an important metric. The interesting thing is that they have been relatively stable as a % of GDP in the past few decades – and lower than say late 1970s.

It is not just how much you borrow, but also the cost of borrowing – and the % of national income (or tax revenues) that are used to pay the debt interest payments

For example, in a recession, when borrowing goes up – quite often bond yields fall. Bond yields fall because there is greater demand for saving and greater demand for buying government bonds, which are seen as a relatively safe investment.

Just a short post, inspired by this article by Hamish McRae in Independent – Would it Matter if Greece left the Euro? So often governments have fought ‘tough and nail’ to stay in an exchange rate system. But, when they finally leave – it is the best thing they ever did, and you’re left thinking …

Readers question: should the government focus on achieving a particular macroeconomic objective over the others? This is a good question. There is a lot that can be said because it encompasses so many different topics. Firstly, the three main macro-economic objectives: Higher economic growth Low inflation Low unemployment There are also less important objectives Reducing …