Readers Question: There just seems to be many paradoxical actions taking place in markets and economies at the moment. How do we explain?

Paradoxes of UK economy

- Low interest rates have not increased spending / economic growth

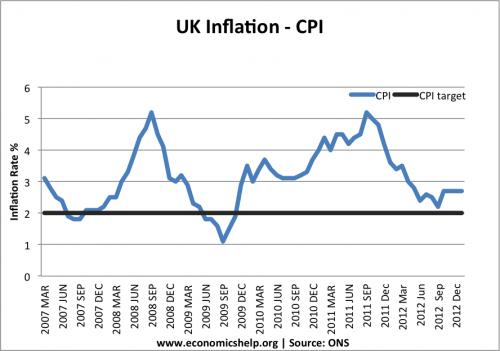

- Despite recession, inflation has been above target.

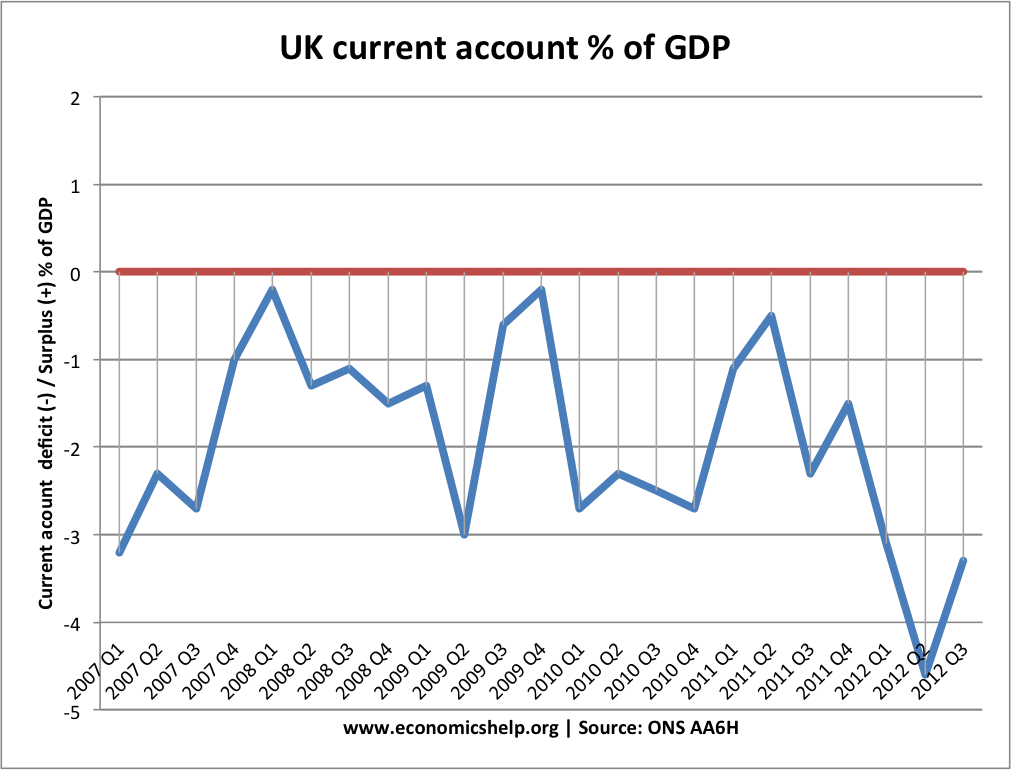

- Despite recession and depreciation of Pound, current account deficit increased in size in 2012

- Spending cuts failed to reduce the budget deficit as the government hoped.

- Despite a longer recession than great depression of 1930s, unemployment is lower than in other more moderate recessions.

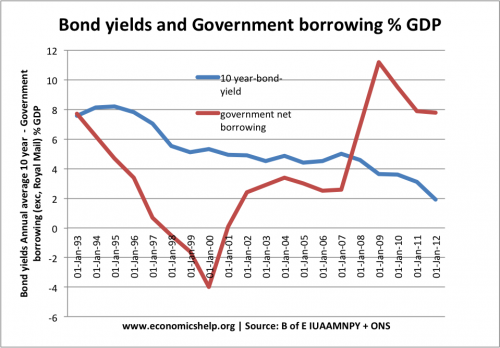

- Record levels of government borrowing have led to a record fall in government bond yields (the opposite of what some people predicted)

- Quantitative easing (increasing money supply) has not actually increased the money supply !

How to explain these paradoxes

1. Zero interest rates have not increased spending

For the past few years, we have been experiencing an unusual combination of circumstances where many ‘ordinary’ rules of economics are not occurring. The economy is currently experiencing a liquidity trap. A liquidity trap involves:

Low-interest rates failing to increase demand. Usually, lower interest rates boost spending because it is cheaper to borrow; but in this current economic situation, even interest rates of 0.5% have failed to see a rapid increase in aggregate demand. Low-interest rates have failed to increase spending and investment because

- Confidence is very low. People don’t want to invest when a double-dip recession is forecast. People are reluctant to spend when they fear unemployment

- House prices and other assets have fallen. Therefore, this creates a negative wealth effect and discourages spending.

- Banks are reluctant to lend because of their liquidity shortages. Therefore, although it is in theory cheap to borrow, it is difficult to get a loan in the first place (e.g. mortgage criteria have become much stricter)

- Banks have a funding gap. This funding gap explains why extra money supply from Quantitative easing hasn’t led to higher bank lending – they have been trying to improve their balance sheet.

- Although Central Bank base rates have fallen to 0.5%, many commercial banks haven’t passed these interest rate cuts onto consumers

- See also: expansionary monetary policy

- UK recession of 2008-13 is longest on record

2. Despite recession – inflation above target

Despite a prolonged recession, inflation in the UK has been above target. Firstly, inflation has only been moderately above target. But, with falling wages, many households have seen a fall in their real wages – inflation has been higher than income growth. Therefore, this moderate inflation has been much more noticeable than usual. If your incomes are rising, you don’t mind price increases. But, this recession has seen an unwelcome combination of rising prices and falling wages – reducing living standards.

But, usually in a recession, you would expect a lower inflation rate (lower demand leads to lower prices, higher unemployment leads to falling wages e.t.c). Why has this not occurred?

The inflation is not due to the usual causes of inflation (excess demand in the economy).

Inflation in the UK was high between 2008 and 2012 because

- Rising price of oil – causing cost push inflation

- Higher tax rates – causing one-off increases in tax

- Impact of depreciation – causing a rise in import prices

- Rising energy prices, such as gas and electricity.

When these temporary factors are stripped away, the underlying core inflation is actually quite low. See also: inflation stats

3. Despite recession and depreciation of Pound, current account deficit increased in size in 2012

In the latter part of 2012, the UK pound fell in value. Also, the double-dip recession led to lower consumer spending. Usually, this leads to an improvement in the current account. A depreciation makes exports cheaper and imports more expensive. A recession reduces spending on imports. Both should improve the current account.

The reasons the UK current account worsened includes:

- Demand for exports and imports is increasingly price inelastic. Therefore, cheaper UK exports ineffective in boosting demand

- Time lags. Firms absorb part of exchange rate movements and consumers don’t see changed prices.

- There has been a bigger recession in Europe which has hampered UK export growth.

4. Spending cuts have not improved the budget deficit

In 2010, the new government announced plans to cut the deficit and balance the budget by 2015. They embarked on a policy of austerity – modest tax increases and spending cuts. However, their budget targets have failed – In 2012/13 they will end up borrowing much more than planned when they started in 2010. This is essentially because economic growth has disappointed. With lower economic growth, tax receipts have been subdued and the government have to spend on more automatic fiscal stabilisers.

He will be borrowing £64 billion more in 2014-15 than he planned just two years ago. This is because he is choosing not to offset the forecast deterioration of £65 billion driven by a worse economic outlook. (IFS, via ITV)

The irony is that the policies to reduce the deficit contributed to the double-dip recession and so ironically policies to reduce the deficit have meant it has fallen by much less than expected. From one perspective you could argue austerity will increase the deficit.

5. Unemployment lower than might be expected

We have a longer recession than the great depression. Yet at 7.8% unemployment is considerably lower than more modest recessions of the 1980s and 1990s. See The unemployment mystery

6. Record levels of government borrowing have led to a record fall in government bond yields

Many feared / predicted high government borrowing would lead to higher bond yields. This has not occurred. Bond yields have fallen because of

- High demand from private sector wanting to save more.

- Prolonged recession meaning people prefer to hold government bonds to private sector investment.

- Q.E. Buying gilts.

Has Money Supply Actually Increased in UK?

Quantitative Easing has led to an increase in the Monetary Base (Narrow money). The Bank of England have created money to buy assets from commercial banks. This has seen an increase in bank reserves and the deposits of commercial banks at the Bank of England. However, the impact on broad money supply and inflation has been muted.

- Very low growth in M4

This suggests that you can print money without causing inflation in a liquidity trap. Q.E. isn’t exactly same as printing money, but the Bank of England have created £375bn of new money.

Has Quantitative Easing Been Inflationary?

No. Because the increase in bank reserves have not really been lent out to the wider economy. The weak growth of M4 shows that despite the increase in Monetary Base, quantitative easing has not translated into stronger Money Supply growth and underlying inflation.

The weakness of underlying inflationary pressure can be illustrated by average wage growth. In the UK average wage growth has been very weak since 2008. In fact, we have seen a fall in real wages.

Related

“…without the effects of quantitative easing, M4 money supply growth would have been negative…”. I’m sure you are right. But it would be interesting to see the actual figures (or a chart) showing this for the UK. Please, please do one.

The extent to which monetary base replaced commercial bank created credit and other forms of money is estimated in this Credit Suisse study. See charts on the first few pages.

http://faculty.unlv.edu/msullivan/Sweeney%20-%20Money%20supply%20and%20inflation.pdf

there’s a graph at FT showing contribution of Q.E.

http://ftalphaville.ft.com/blog/2010/01/27/135551/could-uk-money-supply-collapse-post-qe/