Why didn’t the UK Join the Euro? Joining the Euro would give the UK various advantages: predictability of exchange rates with Europe Easier for consumers to compare prices (price transparency) Lower transaction costs Encourages investment because of greater stability in trade. However, despite these potential benefits the UK decided not to join and shows no …

Bank of England base interest rates are currently 0.5%. Economists are divided about when interest rates will rise. Some point to the evidence of a strong economic recovery to suggest interest rates could rise by mid 2015. Others argue that the strong global deflationary pressures mean that UK inflation is likely to stay very low (currently 0.5%) and therefore interest rates will stay at 0.5% until even 2016.

When interest rates were cut to 0.5% in 2009, few would have predicted that interest rates would have stayed so low for so long. In the past few years, expectations of rising interest rates have often proved a false dawn. The reasons for a rise in rates have later evaporated. Will 2015 be a similar experience with the long-awaited rise in interest rates delayed again?

Projections for interest rates (Nov 2014)

2015 – 0.8%

2016 – 1.4%

2017 – 1.7%

The Bank of England inflation forecast from Nov 2014, suggests inflation is expected to continue to fall until 2017. They see no immediate rise in inflation.

However since the latest Bank of England inflation report in Nov 2014, inflation has fallen more sharply than expected, and this could delay the time of rising interest rates.

Why are interest rates likely to stay at 0.5% until 2016?

Firstly, there are different types of debt to consider

Government debt – See: public sector debt (often referred to as National debt)

Private sector debt – indebtedness of householders, finance sector and non-financial companies.

External debt – the amount we ‘owe’ to other countries

In addition, you might take into account – future liabilities, e.g. pension fund commitments. Also, equally important, is future economic growth, tax revenue and the ability to meet the current debt burden.

Debt burden as % of income

The most useful way to consider the debt burden. Is to consider:

Debt as a % of income.

Also, the % of income / taxes spent on debt interest payments

Government debt

Source: Reinhart, Camen M. and Kenneth S. Rogoff, “From Financial Crash to Debt Crisis,” NBER Working Paper 15795, March 2010. and OBR from 2010.

UK government borrowing fell to record levels in the early 1990s, but since the financial crisis, national debt as a % of GDP has increased to 78% of GDP (2015).

A related to concept to total national debt is the budget deficit. The budget deficit is the annual amount the government is borrowing.

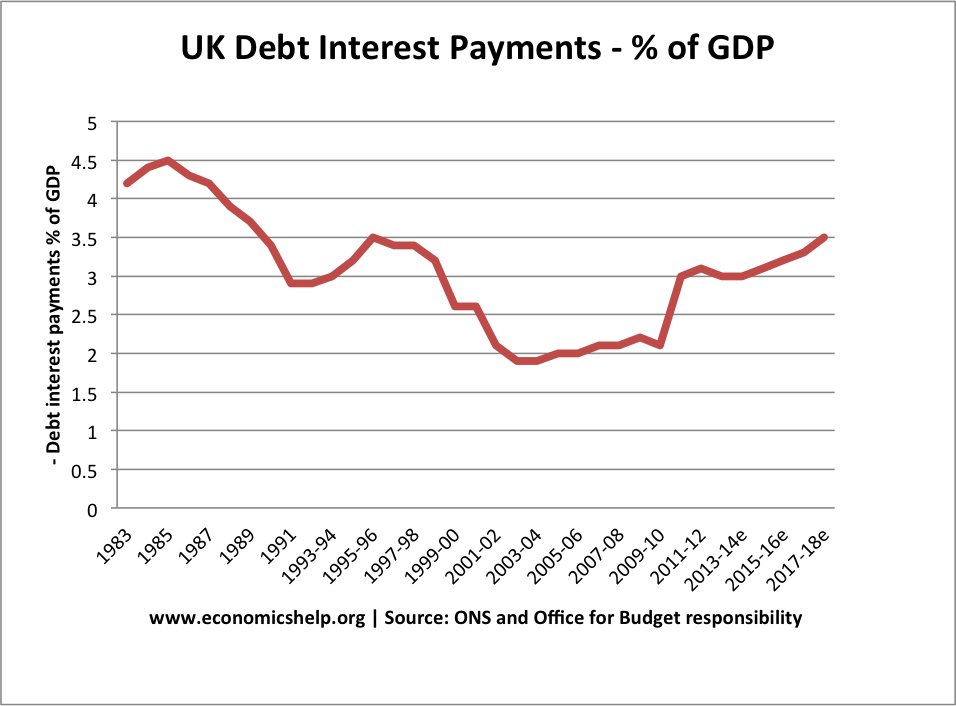

Debt interest payments as % of GDP

Another important consideration is how significant are debt interest payments.

With low interest rates, the cost of servicing the UK government debt is lower than we might expect. Many economists suggest that when interest rates are low, the government should take advantage and borrow to finance investment.

The amount spent on debt interest payments is important for understanding the ‘debt burden’ If you take out a mortgage, the crucial thing is not the total amount outstanding, but the percentage of your income that is spent on mortgage monthly payments.

The majority of UK public sector debt is owned by the UK private sector / Bank of England.

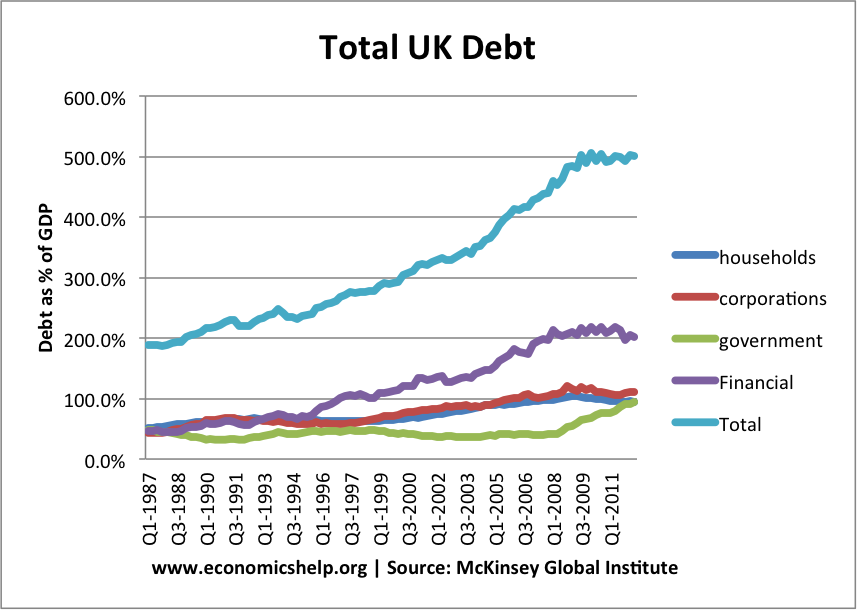

Private sector debt

In addition to government debt it is also important to look at private sector debt. In particular household debt / company debt. For example, at the start of the recession, household debt fell because householders sought to increase savings and pay off their debts, due to low confidence. In this case the government borrowing is partly offsetting the rise in private sector saving.

Financial debt is more complicated. The UK tends to have a large share of financial debt as a % of GDP because it has a large finance sector. But, these large liabilities are offset by high financial sector assets. Financial sector debt becomes a problem if assets fall in value. (e.g. during credit crunch)

You are welcome to ask any questions on Economics. Though you might also like to try google custom search (top right) to see if the topic has been covered before. I am looking to explain economic principles / ideas/ recent developments in economics. I can’t promise to answer, but will try if it meets the …

Question from the Economist. – It is easy to understand the case that European austerity is self-defeating. But it is also easy to see that one cannot run large deficits year after year without limit and that some countries (Greece, Portugal) have exhausted the willingness of private investors to finance them. Is Austerity self-defeating? Austerity …

The original European Union (then called the EEC European Economic Council) was composed of 6 founder members. Belgium France Germany Italy Luxembourg Netherlands The EEC came into existence with the Treaty of Rome 1954. Since then the EU has expanded its borders taking in most European Countries. Enlargement has generally been seen as a positive …

I’ve just got back from my Christmas holidays. I spent two weeks in Croatia (the EU’s newest member, 2013). It was very beautiful by the coast, if somewhat cold. Just like students find it hard to write the first essay after a three week holiday, I also struggle to get into the flow of economics …

A missing market is a type of market failure. A missing market means that there is some obstruction to an efficient free market which would enable a Pareto efficient distribution of resources but for various reasons this market doesn’t exist.