Readers Question: to what extent did the EU recession cause the UK recession?

In economics often several factors occur at the same time, and it is difficult to give a weighting to the importance of each factor. To some extent, people will emphasise the factors which best suits their outlook / beliefs.

It is no surprise that the government prefer to blame the double dip UK recession on ‘unavoidable weakness in the European economy’. It is similarly no surprise the opposition blame the government’s austerity approach adopted in 2010.

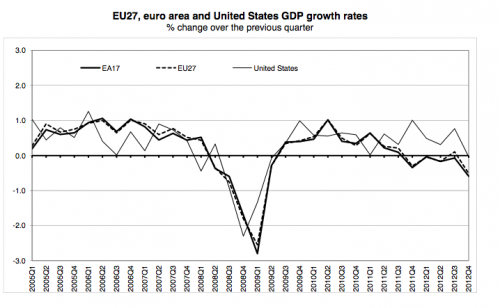

Source: EU GDP

In theory, the European recession of 2012, will effect the UK economy in the following ways:

- Lower export demand. With Europe entering recession, they will buy less goods and services, including less demand for UK exports. UK exports to Europe account for around 13% of GDP and so it is reasonably significant. Lower export demand to Europe can have a knock on effect to other related industries, and a possible negative multiplier effect – causing a bigger final fall in real GDP.

- Reduced confidence. Europe sliding into recession will harm business and consumer confidence. With our main trading partner struggling, firms are less likely to invest in increasing capacity. Also the financial instability in Europe is making banks more nervous and reluctant to lend.

- Lower inward investment. A recession in Europe will create a disincentive for European firms to invest in the UK leading to lower growth.

Evaluation

But, how important a factor is the European recession?

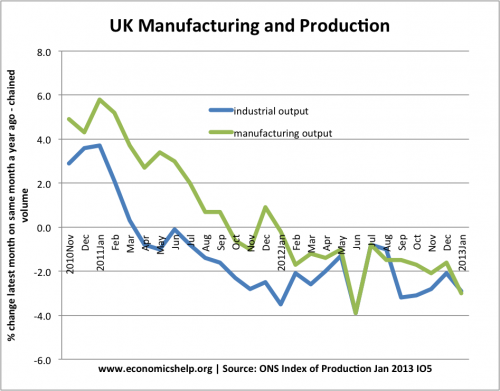

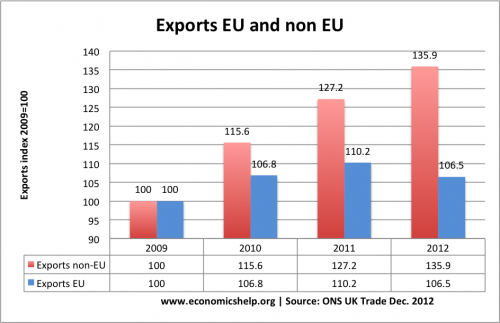

1. Exports to Europe have not fallen significantly

UK exports to the EU increased between 2009 and 2012 by 6.5%. Exports to non-EU countries increased at a faster rate. During this period, the UK current account deficit increased – because demand for imports increased at a faster rate, and if Europe had not gone into recession, we may have seen a bigger increase in exports. But, overall this still suggests that falling exports to Europe were not the main cause of the recession.