Summary of UK Economy at the Start of 2013

The UK economy starts 2013 after one of the longest periods of economic stagnation on record. GDP has been flat for the past two years, and real GDP is still way below the 2008 peak.

Despite the depressing picture of economic growth, unemployment (7.9%) is much lower than might be expected given the sluggish nature of economic growth. However, if we count under-employment (e.g. working fewer hours than would like) and disguised unemployment, then the picture is much less promising.

Consumer confidence remains low as most people have been affected by the unwelcome combination of high inflation and low wage growth. Inflation fell in 2012, but in 2013, we again may see some unwelcome return of cost-push inflation – prices rising despite the output gap.

The government have placed great importance on reducing government borrowing; to reduce borrowing they have limited increases in government spending, and in some areas cut spending.. Some blame these austerity measures for causing the double dip recession. Austerity in the UK has been relatively mild compared to Europe, but it has still affected demand and confidence. Unfortunately, due to the lower growth, government borrowing has fallen more slowly than expected. The bad news is that it’s hard to see beyond years of austerity and sluggish growth.

If you are an optimist, you can see small shoots of economic recovery in the UK. The Euro-crisis is temporarily in abeyance, bank lending costs have fallen, the housing market has shown signs of life, and consumer spending is slowly starting to increase. However, there have been many ‘green shoots’ of recovery in the past five years – and all these green shoots have had a habit of being sniffed out. In fact, economic forecasters have frequently over-estimated the UK economies capacity for recovery and growth. Government forecasters, seem to be permanently revising down forecasts for growth. But, they are not alone. It is a similar story in Europe, where more intense austerity has caused a sharp fall in demand and GDP in southern Europe.

Forecasts for 2013

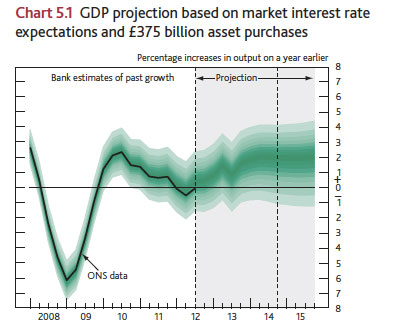

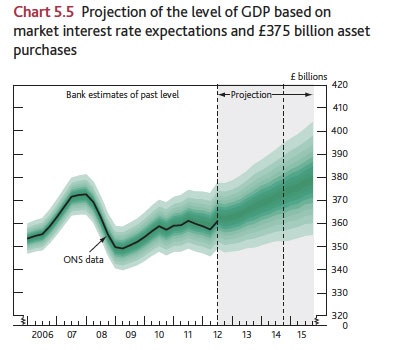

The Bank of England predict very modest growth for 2013, with the potential for a fall in output before the economy recovers towards the end of 2013.

Median economic growth forecast for 2013 around 1%.

Inflation Forecasts 2013

In 2013, inflation is again forecast to be stubbornly high and above the government’s inflation target; as the past few years, this inflation will be due to a combination of cost-push factors – rising university fees, energy prices, food prices. The bank is getting used to being detached about cost-push inflation. But, it means the squeeze on real incomes and living standards will remain – another factor making economic recovery difficult.

In the longer term, the Bank still expect inflation to fall back down to 2%. But, cost-push inflationary pressures can be hard to predict.

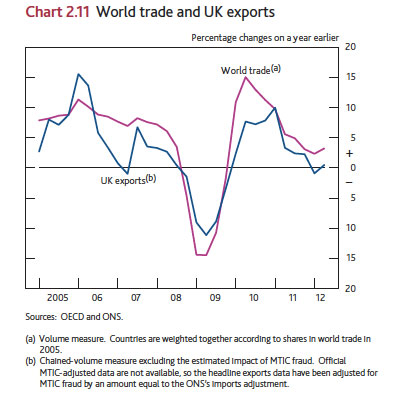

Talk of leaving the EU has become quite prominent in political circles, but politics aside, the UK economy is closely tied to the fortunes of the Eurozone whether we like it or not. Towards the end of 2012, falling bond yields suggested there was some hope that the Eurocrisis was abating. However, falling bond yields are only really a side show to the main problem of mass European unemployment and falling GDP. It is quite likely that the optimism in the Eurozone evaporates when the more fundamental problems re-emerge. It is still hard to see how Europe will get away from the debt-deflationary spiral of prolonged austerity. The Eurozone could yet drag the UK economy into a more serious downturn. Even the US, which has one of most promising economies, shows signs of unnecessarily imposing self-defeating austerity as a result of the fiscal cliff.

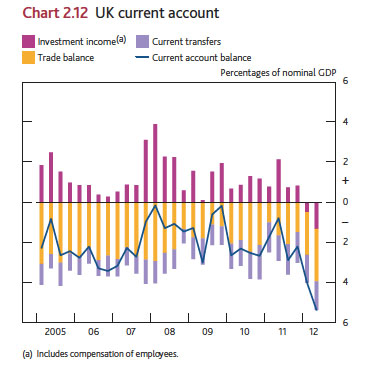

Current Account Deficit

The UK has a large current account deficit (nearly 5% of GDP) – the highest for many years. This is unusual at this stage of the economic cycle. Usually in recession, low consumer spending on imports helps improve the current account. But, the deficit has actually widened rather than narrowed. The extent of the deficit implies the UK needs to do more to rebalance the economy towards net exports. But, this will be difficult if the world economy remains stagnant.

Unemployment

One fortunate aspect of this economic crisis is that UK unemployment is lower than you might expect. Compared to countries in the Eurozone like Portugal and Spain, UK unemployment is low. The lower unemployment is due to the fact the UK labour market has proved more flexible than expected, helping to keep unemployment low. However, the downside is that there has been a rise in under-employment. Also the prospects for 2013 are less promising, a sluggish recovery could see firms become more brutal in getting rid of workers in an attempt to increase productivity.

Investment

Investment both public and private have been hard hit by the recession. Falling bank lending costs may be insufficient to boost investment in 2013.

Productivity

UK Productivity has proved disappointing for the past five years. You expect a dip during a recession, but this fall in productivity is much longer than usual. A challenge for 2013, will be for firms to overturn this fall in productivity.

Conclusion for 2013

2013 will be another difficult year for the UK economy. There is still reasonable hope that we will be able to manage positive growth; even sluggish growth would be welcome after such a prolonged recession. But, the UK economy may yet be held back by recession in Europe. It is disappointing that the government doesn’t have more optimism. It hardly inspires consumer confidence when you warn austerity and hard times will last for the next several years. Unfortunately, the current recession has shown the limitation of monetary policy in a serious balance sheet recession.

Related

Source of B of E graphs for inflation and economic growth forecasts.

Unfortunately it would appear you have hit the nail on the head. Just proves austerity is self-defeating due to it’s reduction in Aggregate Demand and the lack of confidence that follows. Firms are currently sat on spare cash and capacity trying to weather the storm; this is very damaging in aggregate.

As Keynes said; the boom is the time for austerity