The German economy has been one of the world’s strongest economies in the post-war period. There are many aspects of the German economy which deserve praise and emulation – not least strong productivity growth, a booming export sector and prolonged low inflationary growth. In the post-war period Germany has played an important role in promoting economic stability and prosperity within Europe.

But, in recent years, the German economy has seen several cracks appear and German economic thinking is now causing a major drag on Eurozone economic growth and prosperity.

The false goal of a balanced budget

An very important issue in German politics is the desirability of seeing a balanced budget (government spending = government tax revenue). Many German finance ministers have made balancing the budget their primary economic objective. In the UK and US, we see that austerity has a strong political appeal – but in Germany the appeal of ‘responsibility’ and avoiding debt is perhaps even greater. A German friend told me that there is a certain guilt attached to the idea of holding on to debt. (though this guilt is especially felt with government debt – mortgages and business loans are somehow different)

On the objective of reducing budget deficits Germany has been successful. It is also keen to enforce EU rules and the idea of encouraging a balanced budget for its struggling European neighbours.

Angela Merkel recently stated to the EU Parliament, that EU rules must be met:

“All, and I stress again all, member states must respect in full the rules of the strengthened stability and growth pact,” she said. “These rules must be applied credibly to all member states — only then can the pact fulfill as a central anchor for stability and above all for confidence in the eurozone.” (US Today)

Although, Merkel did not name France, the implication was that France must do more to meet the EU Stability and growth pact.

Why is a balanced budget a false goal?

1. Lack of investment

A successful business does not have its objective to borrow nothing. A successful business knows that it needs to invest to make progress and retain its prosperity. Years of cutting government spending has meant that Germany has cut back substantially on public sector investment. There are widespread reports that Germany has a lack of investment in roads, bridges and other forms of transport. There is a fear that important infrastructure, such as roads and bridges are reaching the end of their 70 year cycle, but there is no money to successfully replace them. The economic problem is growing congestion, time wasted and damage to the long term productive capacity of the economy. The Guardian notes

Its (German) investment rate in 2013 was the fourth lowest in the EU; only Austria, Spain and Portugal spent less. Fratzscher, who is head of the German Institute for Economic Research, calculates there is an “investment gap” of €80bn (£63bn).

The Economist reports that German public sector investment is —a paltry 1.6% of GDP— one of lowest in Europe and has fallen since 2009.

It is not just infrastructure spending, but also education where Germany spends lower than the EU average. German productivity has been the envy of the rest of Europe, but there is a danger of complacency and falling behind in the increasingly fast moving technological world.

Economic growth

There is a danger that Germany’s impressive record on economic growth is seriously faltering. After a brief, export led recovery in 2010/11, the German economy has slipped back into recession. Some don’t worry about a temporary setback – a result of lower growth around the world. But, others see this negative growth as a serious concern.

Source: Guardian

German growth is strongly influenced by exports – but if the rest of the world is slowing down, growth may need to come from elsewhere. In the enthusiasm for a balanced budget, the German federal budget has a raft of future austerity measures to come into force. – but this will slow down economic growth.

Usually, deflationary fiscal policy need not lead to lower growth. But, Germany is likely to face relatively tight monetary policy, an unwillingness to engage in any Euro wide quantitative easing, very low inflation, a strong exchange rate and low export growth. It is a cocktail of deflationary factors which could lead to a period of economic stagnation.

Balanced budget and Debt to GDP

As discussed many times, if you want to reduce debt to GDP ratios. It’s no good just focussing on debt. You need to grow GDP. It is growth in GDP which is the best method for reducing debt to GDP in the long term – see: UK In post war period. A German balanced budget combined with prolonged economic stagnation may give the false goal of a balanced budget, but with zero GDP growth there will be little, if any improvement in Germany’s debt to GDP ratio.

Eurozone needs growth

To state the obvious, the Eurozone desperately needs economic growth and lower unemployment.

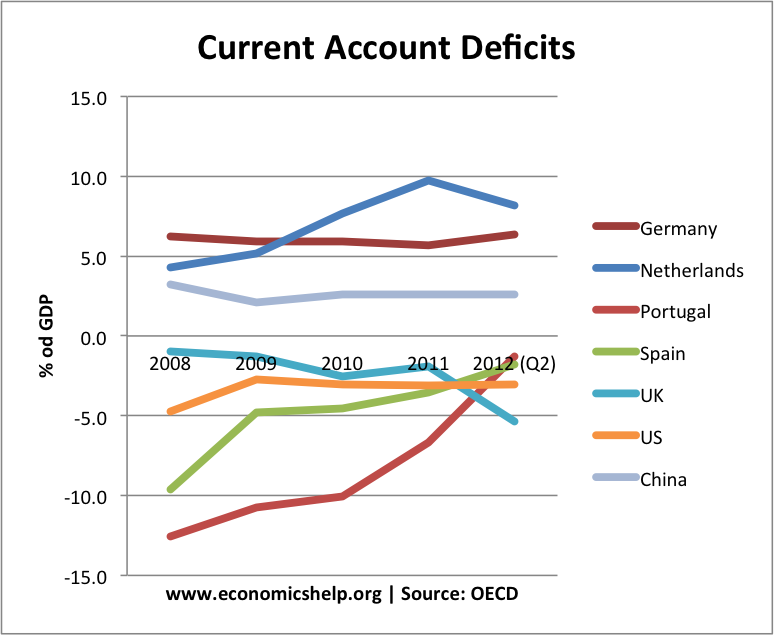

With a large current account surplus, Germany is a key to enabling higher growth. Higher spending and investment from Germany would do a lot to increase overall demand in the EU and help rebalance an unbalanced continent. If German growth is weak and spending curtailed, it will be even harder for embattled nations in the south to escape the cycle of debt, deflation and low growth.

Fiscal policy is not the only tool to improve economic growth. Germany definitely needs to rethink monetary policy. But, ending its false commitment to a balanced budget could be an important step.

Bond yields are at record lows

German 10 year bond yields are at record lows of 0.82%. This shows that European investors want to buy German bonds and they fear an economic slowdown. Germany is not facing a bond crisis with rising bond yields. Maybe this could have been a reason for austerity in Ireland and Italy. But, the opposite is true in Germany – there is very high demand for buying bonds and lending money to the German government. Rather than feel guilty for borrowing, the German economy could feel lucky to be able to borrow at 0.5% to finance public sector investment which could give a very high rate of return.

Inequality

In addition, the future spending cuts are going to be hitting the hardest. The Economist reports that spending cuts involves policies such as removing heating subsidies for the old and poor, and stopping paying welfare beneficiaries’ contributions into the pension system. Tax rises for the well off were vetoed.

On the positive side, German unemployment is low at 5%, but there is no guarantee this will remain.

Conclusion

There is nothing wrong in aiming at a balanced budget – in the course of a normal economic cycle, it makes sense to limit borrowing, but equally it is mistake to give it undue importance. Borrowing is not immoral or the fundamental economic objective. – Ask any homeowner with a mortgage or firm who takes out a loan to finance investment. The biggest threat facing the German (and EU) economy now is the threat of deflationary pressures and low growth. We know Germany has a good reason to dislike the threat of hyperinflation. But, you can’t allow economic policy to be dictated by events of the 1920s – a certain flexibility is needed. And inflation really is the least of Europe’s concerns.

Given the limited room for manoeuvre in monetary policy, it is important to consider the demand side implications of prolonged austerity. Also, it is important to bear in mind that if you can borrow at 0.5% and finance much needed investment in education and infrastructure – this is not being irresponsible. In fact, refusing to invest for the false goal of a balanced budget is the real irresponsibility.

Related

Why compare govt finances as a percentage of GDP? The GDP is not owned/ earned by the govt. The govt only earns from taxes and public sector companies. So why count all private sector earnings as the denominator to calculate deficits? This somehow assumes that all earnings actually belong to the govt aphorism then mercifully allows the rest of the economy to retain whatever they can perhaps out of kindness

I agree with you Dr Tejvan. Balancing the budget is a means to an end and not the end itself. Like many means are prioritised than the end in public and private sector management which is a reflection of economic and financial illiteracy among planners and analyst. Once a word is coined (Balancing the budget (BTB)) and spread, then many politician and bureaucrats imply that BTB is the end….