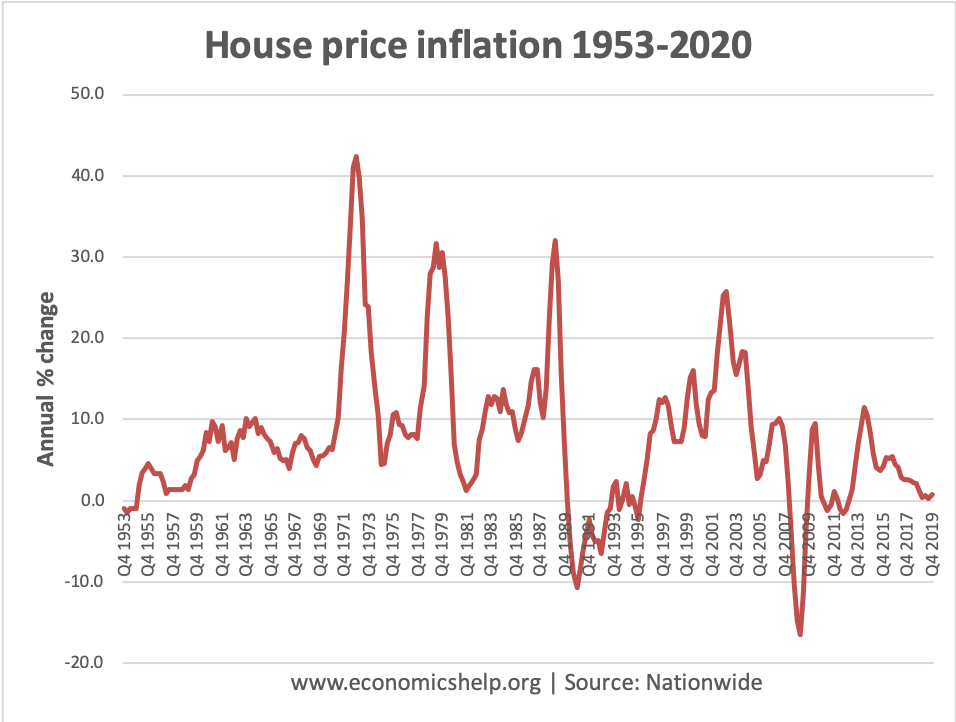

Annual house price inflation has slowed down since the Brexit referendum.

There has been a slight uptick in 2020 since the clear result of the election.

How did we end up with a broken housing market in the UK?

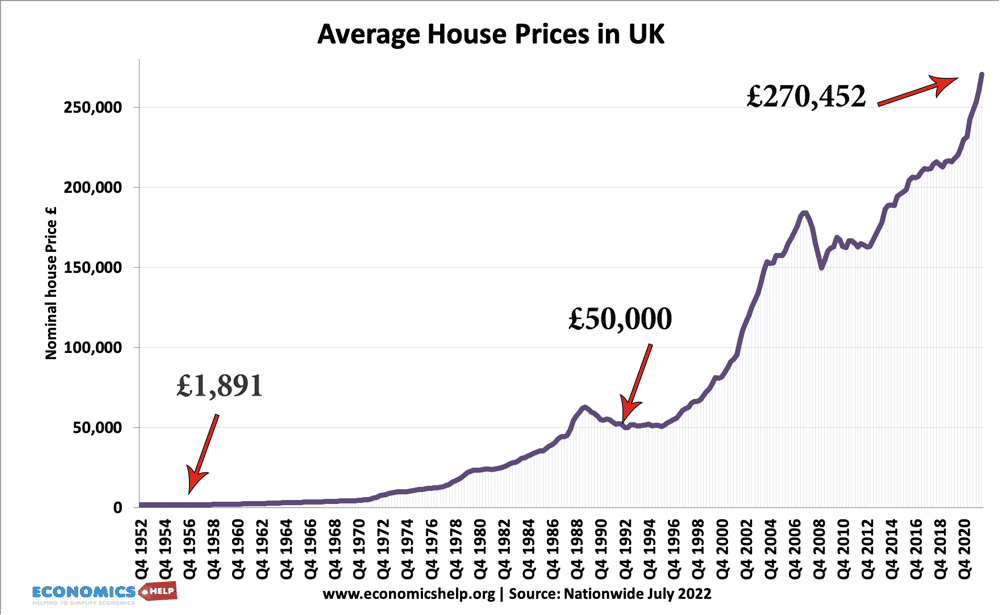

UK House prices in the past few decades

In 1969, average house prices were: £4,312

In 1975, average house prices were: £10,388.

In 1980, average house prices were: £22,676

In 2016, average house prices – £198,564.

In 2022, average house prices – £270,452

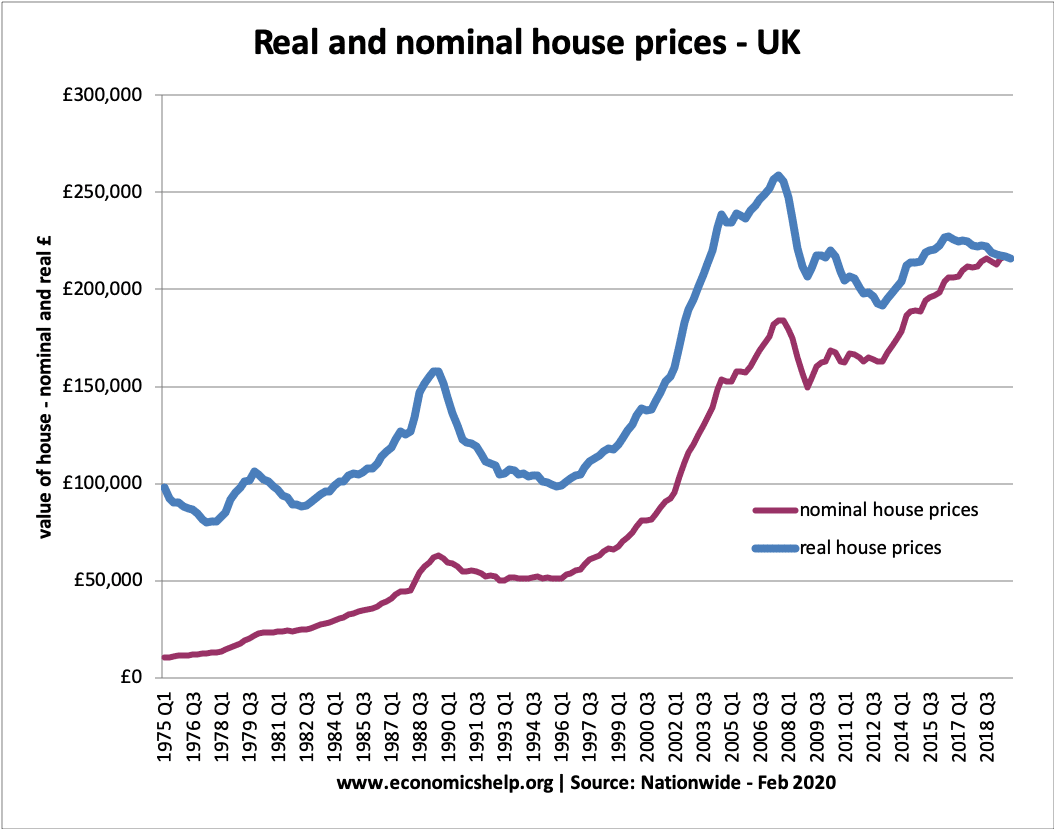

Real house prices

Real house prices are adjusted for the effects of inflation. This gives a more meaningful guide to how house prices have increased compared to typical prices in the economy.

This shows the real increase in house prices – rising faster than inflation.

In 1975 – average house prices (at 2014 prices) was £83,126.

In 2022 – average house prices – £270,000

225% increase in real house prices.

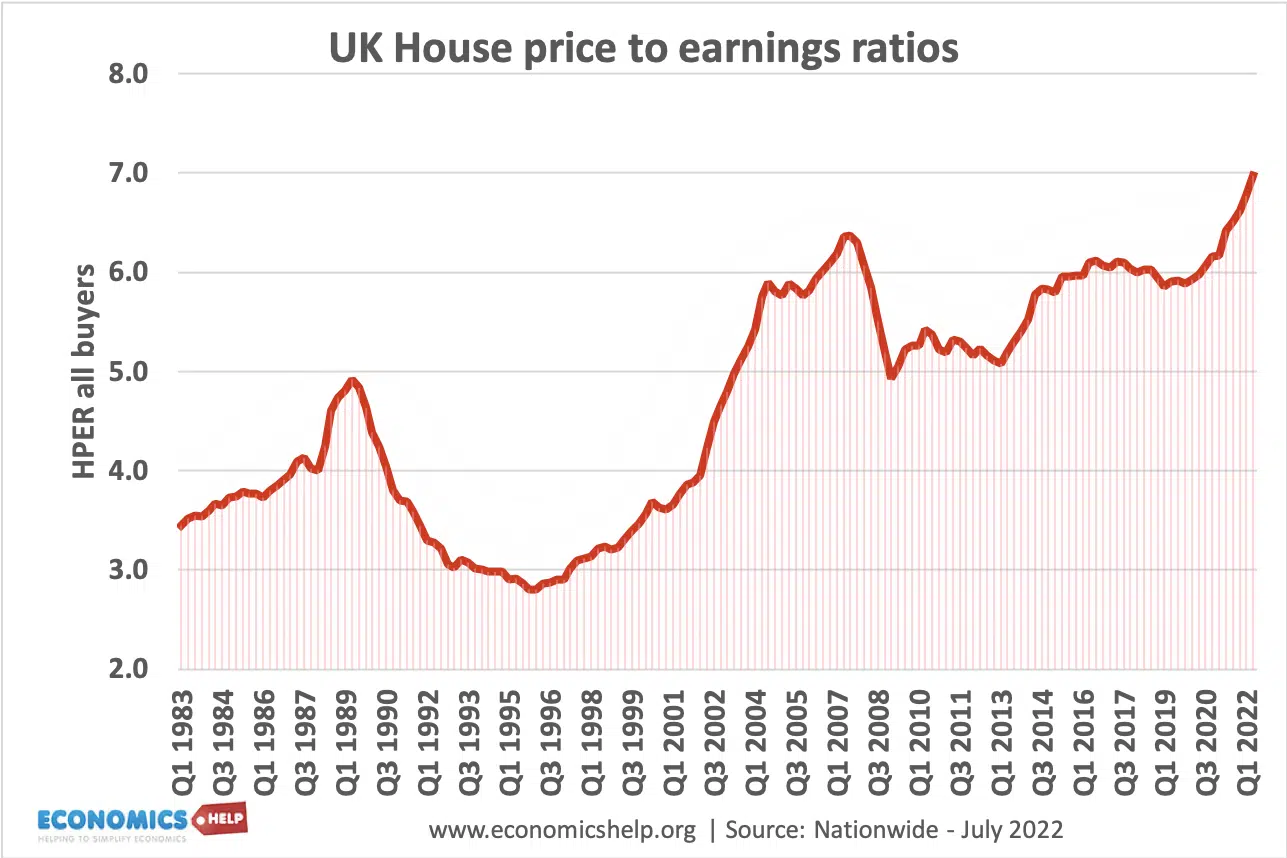

2. Affordability of Housing

First Time Buyers – House Price to Earnings Ratio

For UK first time buyers, the average house price is 5 times average earnings. In London, house prices are 9 times average earnings, whereas, in the north, house prices are only 3.2 times average earnings.

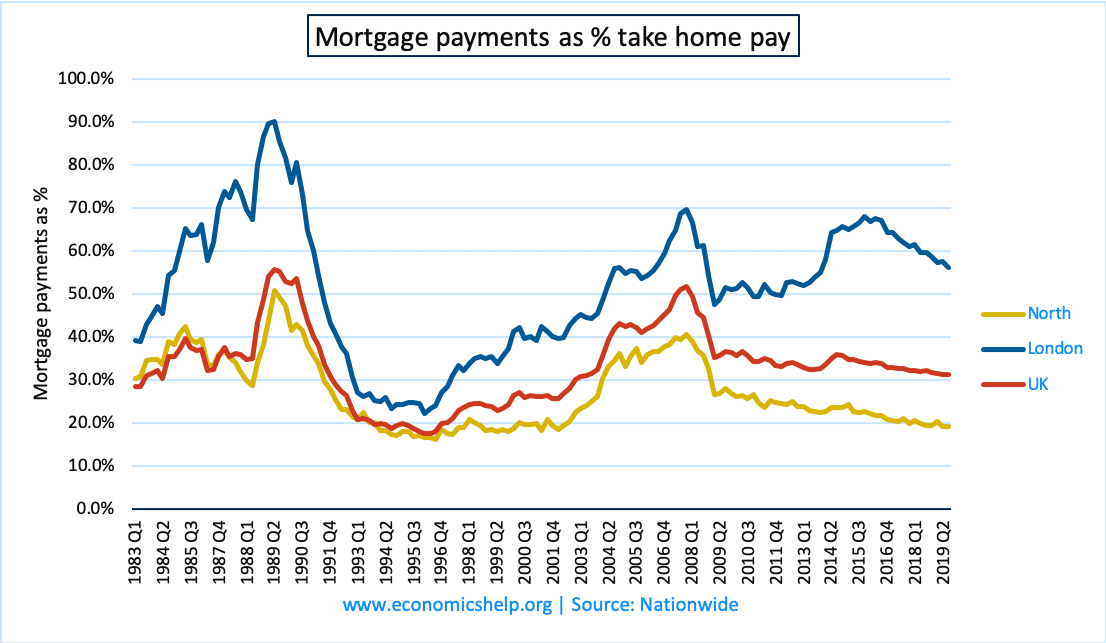

Affordability of Mortgage Payments

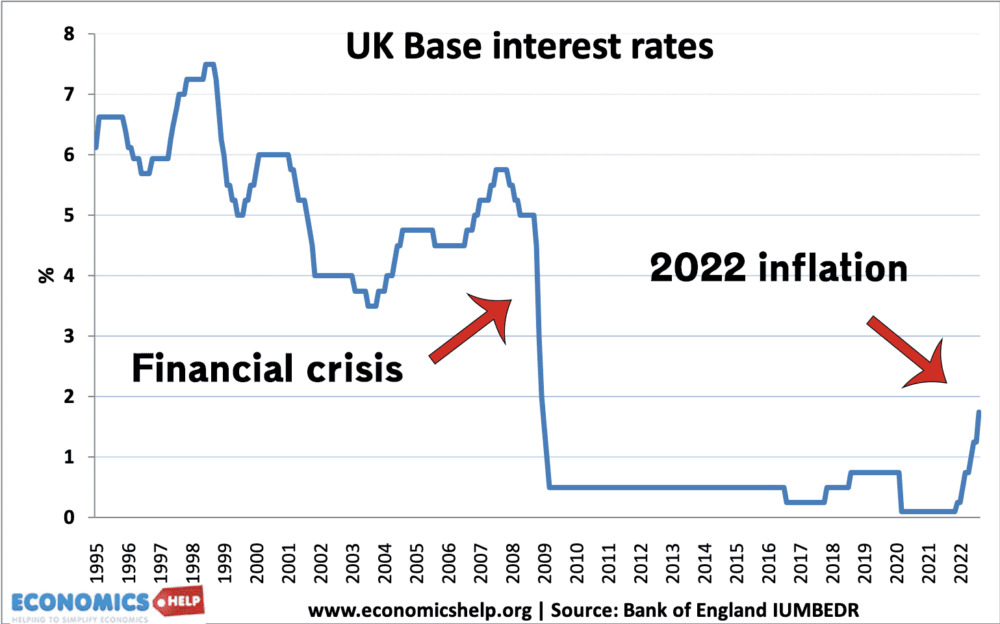

Mortgage payments as % of income reached a peak in late 1989/90 due to record high-interest rates. Rising house prices meant that the % of mortgage payments grew in the 2000s. However, in 2009, interest rates were cut to 0.5% leading to lower mortgage payments for homeowners.

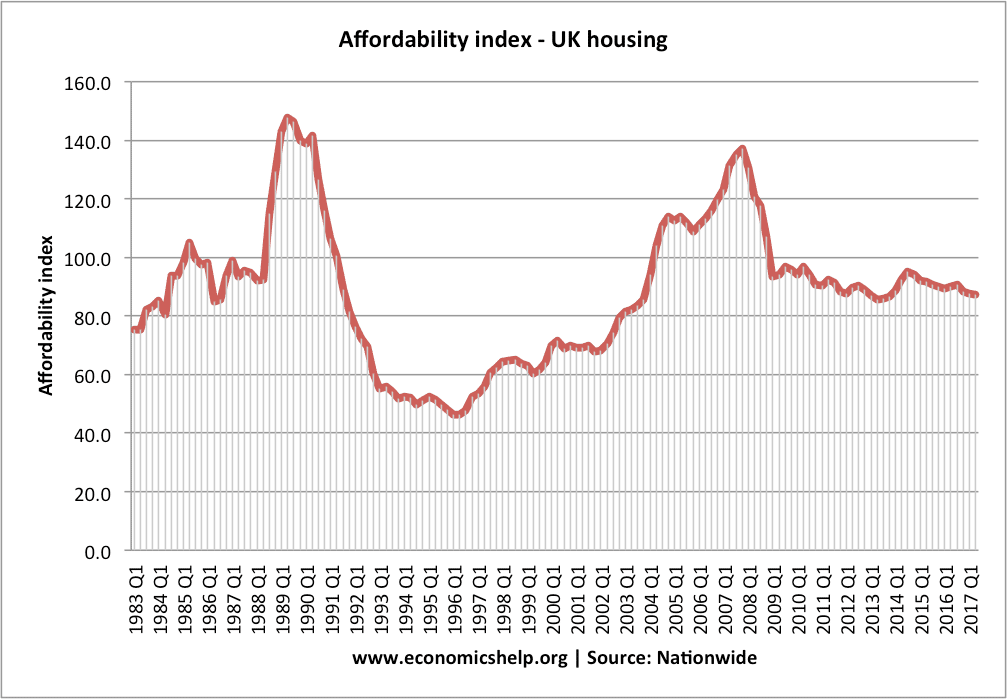

Affordability index

The nationwide also produce an affordability index. Index base year 1985=(100)

There has been a dramatic fall in Bank of England base rates (which has continued to remain at 0.5%) but the bank’s standard variable rates have fallen at a much lower rate. See more at explaining the gap between base rates and commercial lending rates.

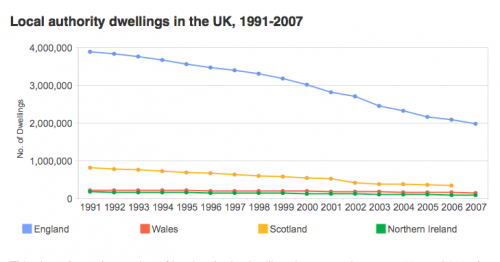

During the post-war period, construction of local government housing increased supply. Home builds reached over 400,00 a year in the late 1960s. However, from the 1980s, the government retreated from building houses, leaving it to the private sector and a small contribution from housing associations. Due to strict planning legislation, the supply of housing has failed to meet government targets.

For example, in 2007, the government estimated they would need to build 240,000 homes a year until 2016, to keep up with growing demand. However, after the credit crunch, housing completions fell to 100,00 a year.

Between 1950 and the early 1980s, the percentage of homes which were bought steadily increased, and the renting sector fell. Mrs Thatcher encouraged this trend in the 1980s, with a policy of encouraging home ownership and selling off council homes. Mrs Thatcher allowed the sale of council properties to their tenants. The stock of social housing has fallen since the early 1980s.

However, the trend in homeownership has been reversed in the last decade, due to the declining affordability of homeownership.

source: JRF Housing & Neighbourhood studies

local authority housing stock has plummeted due to the popular right to buy scheme and transfer of housing stock to housing associations.

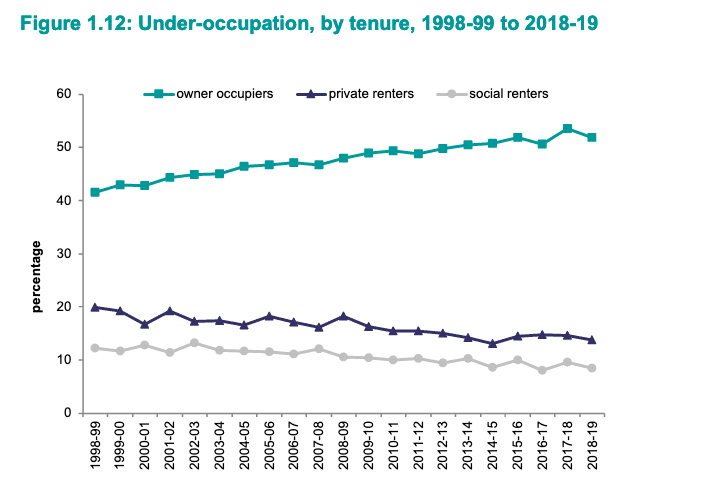

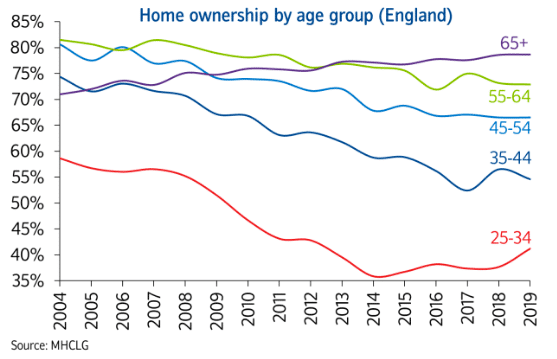

Inequality by age

Source: English Housing Survey 2018/19

The high house prices have led to a drop in homeonwership rates for young people.

The volatility of UK house prices. Though it should be noted these statistics show nominal house price changes. In the 1970s, high inflation rates magnified the nominal house price rises.

House prices adjusted for inflation

Even adjusted for inflation, we have seen strong growth in house prices. Real house prices

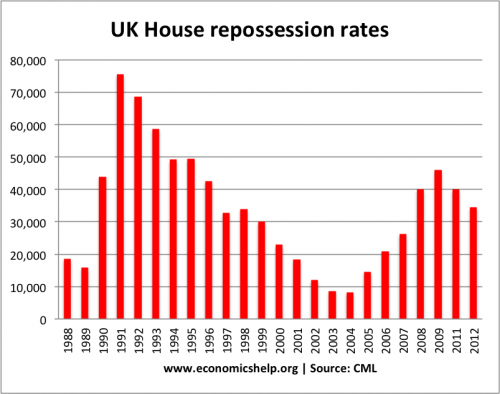

Mortgage defaults and arrears

Mortgage default rate statistics are produced by Council of mortgage lenders (CML). See repossession rates

Housing Benefits

Just under 5 million receive housing benefit, at an average of £93 a week. This is a rough annual cost of £23 billion.

Those housing price to earnings ratios are unsustainable. Anything over about 4 means that buying a house will be economically crippling. 6.0 is ridiculous.

We are sitting at between 7 and 8 times in Australia. It is possible but certainly stymies any decent short term growth until income catches up.

Excuse me for pointing out the obvious, but why are those ratios unsustainable if interest rates stay low?

It’s the ratio of house-price-multiplied-by-interest-rate to earnings that determines affordability, not ratio of house price to earnings.

If rates fall as prices rise, then the first ratio remains affordable. If earnings rise, the ratio remains affordable.

Interest rates have been on a downward trend for 25 years and inflation has been tamed, there’s no reason for that trend to change..

I just don’t think interest rates will stay at 0.5%. Even if rates increased to an historical low of 3%, it would increase mortgage cost.

“Interest rates have been on a downward trend for 25 years and inflation has been tamed, there’s no reason for that trend to change.” ….. so you expect interest rates to continue to decline even into negative territory for ever? I think you should take a look at interest rates over a longer period that just 25 years. The UK has records going back to 1694!

The UK as a whole will consist of hotspots and areas severely hit by economic woes. I believe that UK house prices as a whole will fall again in 2013 . Average house prices of course should be taken with a pinch of salt, there is no such animal. As a visual roadmap, I see price falls rippling out from London suburbs in concentric circles, getting worse as they spread. There will be hots spots of stable economy towns and these along with very desirable properties will be somewhat protected.

well paul, you were wrong. nobodey can see the future…

No-one could have forseen the governments funding for lending scheme. That alone collapsed rates for savers, and pumped 42 billions into UK housing.

National disgrace.

” I believe that UK house prices as a whole will fall again in 2013 .”

An instructive post. People to really know who they want to reach and why or else, they’ll have no way to know what they’re trying to achieve. People need to hear this and have it drilled in their brains.. Thanks for sharing this great article.

Although I am no economist; I hope to learn a great deal from your recently discovered site; I have the great advantage, both of experiencing and implementing housing policies since the 1940s. Without a political input, it is difficult for economists to see the trees for the wood (intended reversal).

Macmillan’s Grand Design for Housing (1953) mapped the motivations of policy for half a century, during which Conservatives served three times longer in government than Labour. The repeated mantras were ‘a property owning democracy’ and the intention ‘to restore the private rented sector as it was before the war’. Macmillan restored deregulation and reduced the standard of council houses to serve only a welfare need. Heath believed he could use the buried equity of the rented stock to fund rent subsidies that would allow him to raise all rents to the levels of the private sector. In 1971, He announced that his Housing Finance Act 1972 would double council rents. House prices doubled before he had time to implement his rent increases – an unrecognised and unreported economic event of the 1970s, I have many more. Thatcher realised that private rents could not compete with any form of investment for the provision of housing, so she abolished the low cost rented sector. The right to buy law gave away huge sales discounts. Effectively, she removed the growth of equity in the rented stock and prevented it from being used to reduce rents. This is still an unrecognised and unreported health warning of the RTB law, which implements the high rent policy that creates unaffordable unstable house prices and unaffordable rent subsidies.

Whenyou post charts and say uk house prices are going up, would it not be better if you posted charts from region to region, this would give a true picture on the housing market, Also why not post a chart on how buy to lets have effected the market after all with out buy to lets house prices would have fallen considerably, with buy to lets the banks in effect own most of the properties in the uk

Sirs – Are you able to supply me with figures that denote rates payable on residential property in 1975?

In a decade owner-occupied homes fell by 0.3m from a historical high that was deliberately engineered by Thatcher to create long term Tory voters. In that same decade private rental properties have increased by 2.2m. Far from stealing properties from first time buyers, the private rental sector has funded the majority of construction over the period.

As Figure 4.2 shows, the private sector has been consistent. It will build but at profitable rate; if the market is flooded prices will fall and the entire industry fails. Governments are not constrained by needing to make a profit but they have failed to stepped in to increase supply despite continually stating that supply needs double.

Governments have consistently distorted the markets by artificial intervention and are now crying over spilt milk.

“Between 2004 and 2013 the number of owner-occupied homes in Britain dropped from 18m to 17.7m. Over the same period private-rental properties rose from 3m to 5.2m.”

Home ownership increased from 55% of households in 1980 to 69% in 2002. But since then it has fallen back. It is predicted that home ownership will decrease to 60% of households by 2025.

Wages are not rising as fast as house prices. This is not sustains able. Market is flooded with BTL and people remortgaging. Surely interest rates need to go up to calm the market. Only people who can afford houses is investors, creating a two tier society of rich and poor

Also banks only lend 4 times income? Average wage is £27,000 and more people are borrowing into retirement on 35 year mortgages. The housing market is heading for a crash surely?

Those housing price to earnings ratios are unsustainable. Anything over about 4 means that buying a house will be economically crippling. 6.0 is ridiculous.

We are sitting at between 7 and 8 times in Australia. It is possible but certainly stymies any decent short term growth until income catches up.

Excuse me for pointing out the obvious, but why are those ratios unsustainable if interest rates stay low?

It’s the ratio of house-price-multiplied-by-interest-rate to earnings that determines affordability, not ratio of house price to earnings.

If rates fall as prices rise, then the first ratio remains affordable. If earnings rise, the ratio remains affordable.

Interest rates have been on a downward trend for 25 years and inflation has been tamed, there’s no reason for that trend to change..

I just don’t think interest rates will stay at 0.5%. Even if rates increased to an historical low of 3%, it would increase mortgage cost.

“Interest rates have been on a downward trend for 25 years and inflation has been tamed, there’s no reason for that trend to change.” ….. so you expect interest rates to continue to decline even into negative territory for ever? I think you should take a look at interest rates over a longer period that just 25 years. The UK has records going back to 1694!

http://www.theguardian.com/business/interactive/2008/nov/05/interest-rates-history

http://www.bankofengland.co.uk/statistics/Documents/rates/baserate.xls

The UK as a whole will consist of hotspots and areas severely hit by economic woes. I believe that UK house prices as a whole will fall again in 2013 . Average house prices of course should be taken with a pinch of salt, there is no such animal. As a visual roadmap, I see price falls rippling out from London suburbs in concentric circles, getting worse as they spread. There will be hots spots of stable economy towns and these along with very desirable properties will be somewhat protected.

well paul, you were wrong. nobodey can see the future…

No-one could have forseen the governments funding for lending scheme. That alone collapsed rates for savers, and pumped 42 billions into UK housing.

National disgrace.

” I believe that UK house prices as a whole will fall again in 2013 .”

LOL

lol hahah love this

An instructive post. People to really know who they want to reach and why or else, they’ll have no way to know what they’re trying to achieve. People need to hear this and have it drilled in their brains..

Thanks for sharing this great article.

Post-war house prices were stable within about 10% for 25 years.

http://ukhousingpolicy.com/images/Price_Inflation.gif Cut and paste to a browser

Although I am no economist; I hope to learn a great deal from your recently discovered site; I have the great advantage, both of experiencing and implementing housing policies since the 1940s. Without a political input, it is difficult for economists to see the trees for the wood (intended reversal).

Macmillan’s Grand Design for Housing (1953) mapped the motivations of policy for half a century, during which Conservatives served three times longer in government than Labour. The repeated mantras were ‘a property owning democracy’ and the intention ‘to restore the private rented sector as it was before the war’.

Macmillan restored deregulation and reduced the standard of council houses to serve only a welfare need. Heath believed he could use the buried equity of the rented stock to fund rent subsidies that would allow him to raise all rents to the levels of the private sector. In 1971, He announced that his Housing Finance Act 1972 would double council rents. House prices doubled before he had time to implement his rent increases – an unrecognised and unreported economic event of the 1970s, I have many more.

Thatcher realised that private rents could not compete with any form of investment for the provision of housing, so she abolished the low cost rented sector. The right to buy law gave away huge sales discounts. Effectively, she removed the growth of equity in the rented stock and prevented it from being used to reduce rents. This is still an unrecognised and unreported health warning of the RTB law, which implements the high rent policy that creates unaffordable unstable house prices and unaffordable rent subsidies.

Whenyou post charts and say uk house prices are going up, would it not be better if you posted charts from region to region, this would give a true picture on the housing market,

Also why not post a chart on how buy to lets have effected the market after all with out buy to lets house prices would have fallen considerably, with buy to lets the banks in effect own most of the properties in the uk

Sirs – Are you able to supply me with figures that denote rates payable on residential property in 1975?

In a decade owner-occupied homes fell by 0.3m from a historical high that was deliberately engineered by Thatcher to create long term Tory voters. In that same decade private rental properties have increased by 2.2m. Far from stealing properties from first time buyers, the private rental sector has funded the majority of construction over the period.

As Figure 4.2 shows, the private sector has been consistent. It will build but at profitable rate; if the market is flooded prices will fall and the entire industry fails. Governments are not constrained by needing to make a profit but they have failed to stepped in to increase supply despite continually stating that supply needs double.

Governments have consistently distorted the markets by artificial intervention and are now crying over spilt milk.

“Between 2004 and 2013 the number of owner-occupied homes in Britain dropped from 18m to 17.7m. Over the same period private-rental properties rose from 3m to 5.2m.”

Home ownership increased from 55% of households in 1980 to 69% in 2002. But since then it has fallen back. It is predicted that home ownership will decrease to 60% of households by 2025.

http://www.economist.com/news/britain/21693730-many-homes-sold-under-right-buy-are-now-privately-let-london-renting-will-soon-be-more

Wages are not rising as fast as house prices. This is not sustains able. Market is flooded with BTL and people remortgaging. Surely interest rates need to go up to calm the market. Only people who can afford houses is investors, creating a two tier society of rich and poor

Also banks only lend 4 times income? Average wage is £27,000 and more people are borrowing into retirement on 35 year mortgages. The housing market is heading for a crash surely?