Readers Question: Do you think the help to buy scheme is fuelling a housing bubble? Only about 3% of houses are bought through this method but do you think that it is likely that a bubble will develop?

In a way, I think you answer the question yourself in stating that only 3% of houses are bought through this method

With such a small percentage of homes bought through this scheme, it is not going to be a major cause of a housing bubble; however, in a relatively significant way, it will add to housing demand. Given the inelastic nature of housing supply, it will make a contribution to pushing up house prices.

Without the help to buy scheme would people have bought houses anyway? I’m not sure. I think the scheme will definitely help some to get a mortgage, and therefore buy rather than renting. In that regard it is adding to housing demand, and therefore pushing up prices, but only a small amount.

Will a housing bubble develop?

This is a more difficult question. There are different types of housing bubbles.

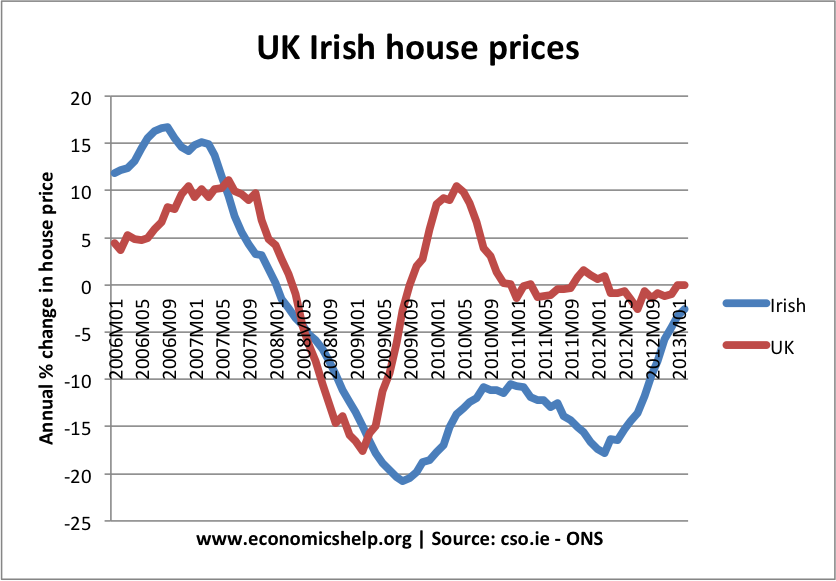

One is the housing bubble experienced by US, Ireland and Spain – where property prices rose substantially above average earnings, and then fell by up to 50%. This is because house prices in these countries became divorced from the fundamentals of housing supply and demand. When the mortgage market experienced difficulties, demand fell and prices fell significantly. The crucial thing about US, Ireland and Spain was that after the housing bubble and bust, there was a large excess supply of housing. Therefore, when demand fell, prices fell considerably.

See: Ireland Housing bubble and bust

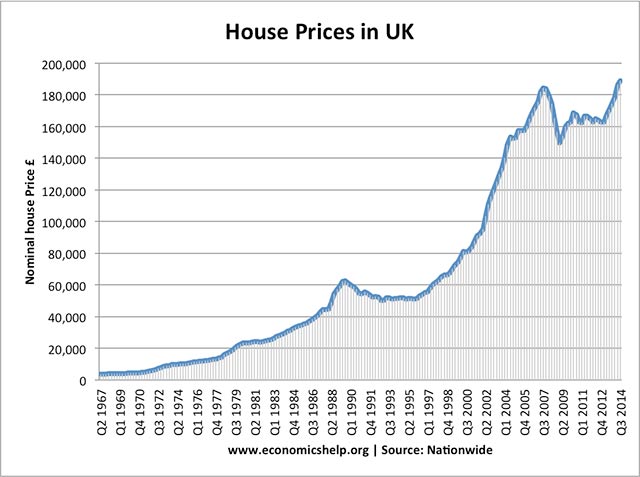

The UK housing market behaved differently. When demand fell in 2007/08 because of the credit crunch, prices did drop by 20%. But, house prices stabilised much quicker, and then – defying many predictions – began to rise quite rapidly. Meaning that in the UK, house prices in many areas are higher than before the crash.

The main difference is that in the UK, there was no excess supply of housing; there was no boom in home building. Therefore, when the crash came, there was still this fundamental shortage of housing, which keeps prices ‘artificially’ high.

Why UK property prices may be overpriced

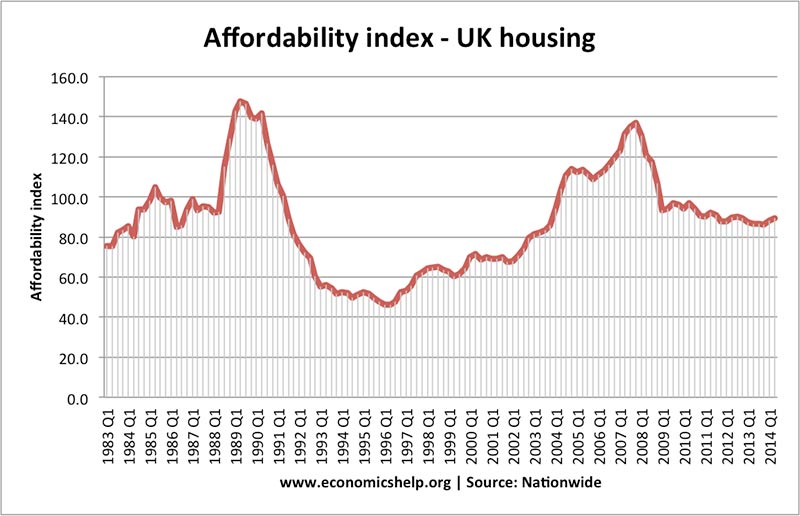

- Interest rates set to rise. UK interest rates have stayed at zero since early 2009; this period of ultra low interest rates has benefited the property market and kept mortgages affordable. If interest rates rise back to ‘normal’ rates (e.g. around 5% – many homeowners will see a sharp rise in the cost of mortgages, causing demand to fall. The Bank of England recently did a survey and found a two-percentage-point rise in mortgage interest rates would likely raise the proportion of mortgagors with a debt service ratio (DSR) of at least 40% from its current level of 4% to about 6% (360,000 to 480,000 households)

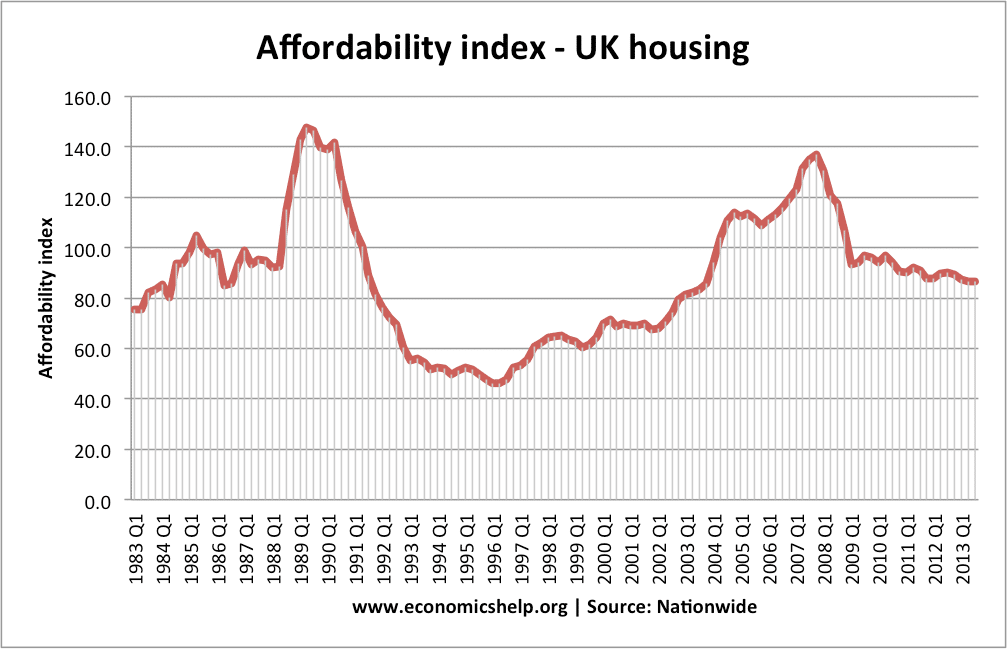

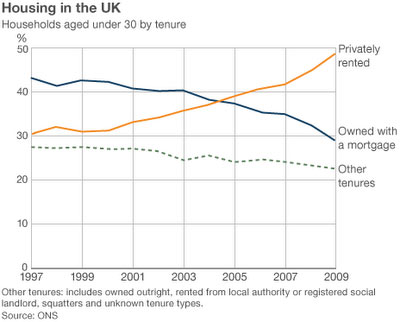

UK housing – prices kept affordable by low interest rates. - House price to income ratios. House prices have risen much faster than incomes, meaning the younger generation are not able to get a mortgage. The average age of mortgage holders has increased, and the deposit required has also gone up. Because house prices are so expensive, there are many who cannot consider buying.

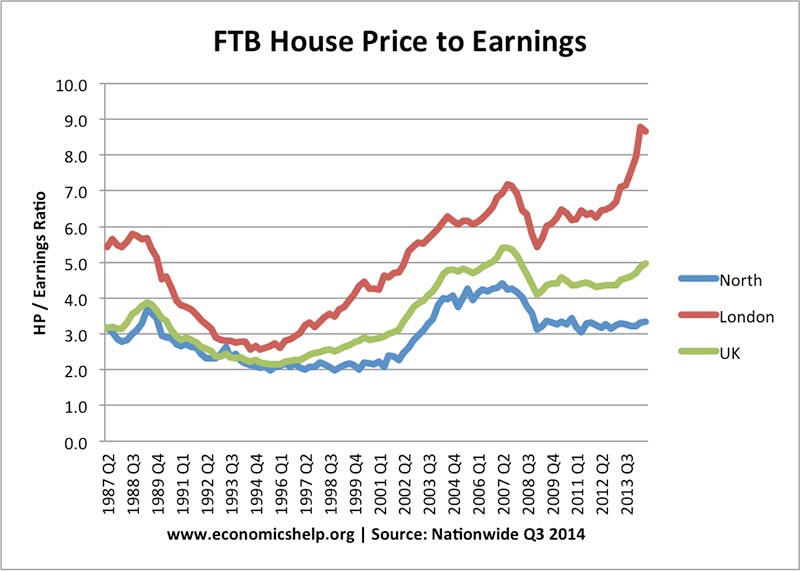

House price to earning ratios for first time buyers. The ratio is 5.0 significantly higher than previous decades.

- Buy to let market. With home ownership rates falling, the growth in demand for housing is coming from investors.

These investors are more likely to be sensitive to changing house prices. If there is a sustained drop in prices, this may be magnified by investors leaving the UK housing market.

- Economic growth is still fragile. Although the UK recovery is reasonably strong, the Eurozone looks weak with anaemic growth and the threat of deflation; there is a strong possibility that a weak EU economy could act as a drag on UK growth.