The UK national debt is the total amount of money the British government owes to the private sector and other purchasers of UK gilts (e.g. Bank of England).

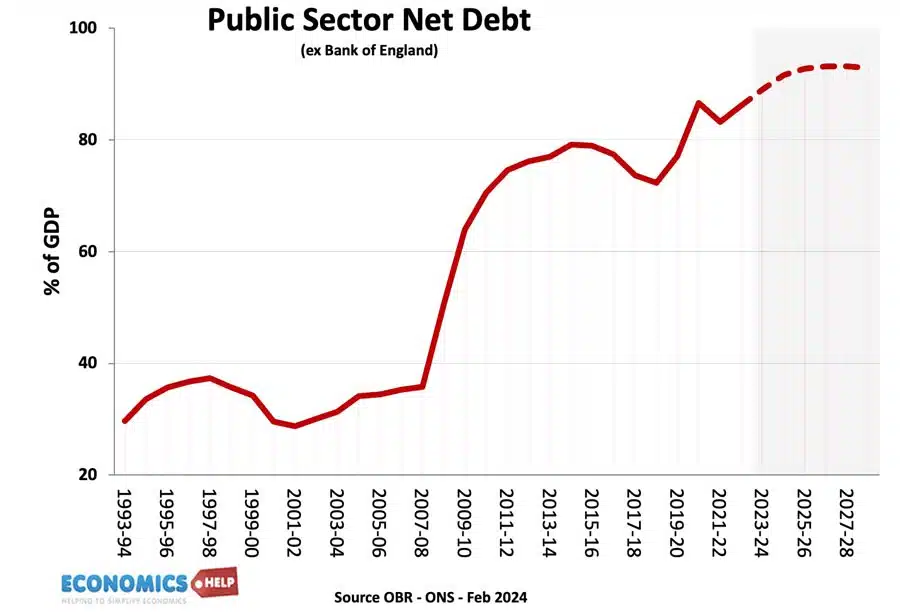

- UK public sector net debt (ex public sector banks) was £2,685.6 billion or 98.1% of GDP (20 Dec 2024).

- The OBR have forecast substantial rises in UK debt over the coming decade because of demographic factors, putting strain on UK spending.

- Source: [1. ONS public sector finances,- HF6X] (page updated 20 Jan 2024)

Source: ONS debt as % of GDP – HF6X | PUSF – public sector finances at ONS

Reasons for National debt

- Enables the government to spend more during periods of national crisis, e.g wars, pandemics, and recessions.

- In a recession, the government will automatically receive lower tax revenues (less VAT and income tax) and will have to spend more on benefits (e.g. more unemployment benefits) This causes a cyclical rise in debt.

- Extra government borrowing during a recession can help provide fiscal stimulus to promote economic recovery. By borrowing and then spending more, the government is injecting demand into the economy and this can help to reduce unemployment. This is known as fiscal policy and was advocated by J.M. Keynes.

- Strong market demand for government debt. Private investors buy gilts because they are seen as risk-free investments and there is also an annual dividend from the bond yield. Since 2009, there has been strong demand despite very low-interest rates, meaning the government can borrow very cheaply.

- Finance investment. The government could borrow to finance public investment projects that can lead to higher growth in the future.

- Political convenience. There is usually political pressure to cut taxes and increase government spending. Allowing debt to rise can be a way for the government to avoid difficult choices.

Forecast for the National debt?

Source: Fiscal risks and sustainability – OBR – Economic and Fiscal Outlook Oct 2024

The OBR have forecast that, on our given trajectory, UK public sector debt could reach 350% of GDP within 50 years. The pessimistic outlook for national debt is made because

- An ageing population and demographic changes will put increased pressure on government spending, notably health care and pension spending.

- A smaller working population will limit UK’s productive capacity.

- Stress on finances from geopolitical events, such as frostier relations with China, Russia and the Middle East.

- Higher energy prices

- Costs of climate change.

- Declining tax revenues from petrol in a decarbonising economy.

- Low productivity growth of UK since the financial crash of 2009

- Recent boost to debt from the financial crisis and one-off cost of Coronovirus pandemic, which cut tax revenues and required government support for lockdown measures.

UK debt in context

Predicting debt for the next 50 years is difficult since we don’t know what kind of productivity improvements may come, e.g. continued gains in renewable energy may reduce the burden of higher oil and gas prices. Equally, the costs of environmental change could be worse.

History of the national debt

Main article: History of UK national debt

UK national debt since 1900

Source: Reinhart, Camen M. and Kenneth S. Rogoff, “From Financial Crash to Debt Crisis,” NBER Working Paper 15795, March 2010. and OBR from 2010.

These graphs show that government debt as a % of GDP has been much higher in the past. Notably in the aftermath of the two world wars. This suggests that current UK debt is manageable compared to the early 1950s. (note, even with a national debt of 200% of GDP in the 1950s, UK avoided default and even managed to set up the welfare state and NHS.

Debt reduction and growth

The post-war levels of national debt suggest that high debt levels are not incompatible with rising living standards and high economic growth.

- The reduction in debt as a % of GDP 1950-1980 was primarily due to a prolonged period of economic growth. See: how the UK reduced debt in the post-war period

- This contrasts with the experience of the UK in the 1920s when in the post First World War, the UK adopted austerity policies (and high exchange rate) but failed to reduce debt to GDP. Debt in Post-First World War period.

Budget deficit – annual borrowing

This is the amount the government has to borrow per year.

- Government

- borrowing in the financial year to December 2024 was £129.9

Annual borrowing since 1950. Figures for 2023-24 are forecasts (and rather optimistic!)

Debt and bond yields

Bond yields a the interest that the government pay bond/gilt holders. It reflects the cost of borrowing for the government. Lower bond yields reduce the cost of government borrowing.

Between 2007 and 2020, UK bond yields fell. Countries in the Eurozone with similar debt levels saw a sharp rise in bond yields putting greater pressure on their government to cut spending quickly. However, being outside the Euro with an independent Central Bank (willing to act as lender of last resort to the government) means markets don’t fear a liquidity crisis in the UK; Euro members who don’t have a Central Bank willing to buy bonds during a liquidity crisis have been more at risk to rising bond yields and fears over government debt.

See also: Bond yields on European debt | (reasons for falling UK bond yields)

Since 2021, bond yields have risen due to pick up in inflation

Cost of Interest Payments on National Debt

The cost of National debt is the interest the government has to pay on the bonds and gilts it sells. According to the OBR in 2023-24, debt interest payments will be £108 billion. (3.2% of GDP) or 5.2% of total spending. It is lower than in previous decades because of lower bond yields.

See also: UK Debt interest payments

The era of low interest rates post 1992 helped to reduce UK debt interest payments as a ratio of government revenue. However, with interest rates and borrowing increasing – debt interest cost have increased significantly.

Potential problems of National Debt

- Interest payments. The cost of paying interest on the government’s debt is very high. In 2011 debt interest payments will be £48 billion a year (est 3% of GDP). Public sector debt interest payments will be the 4th highest department after social security, health and education. Debt interest payments could rise close to £70bn given the forecast rise in national debt.

- Higher taxes / lower spending in the future.

- Crowding out of private sector investment/spending.

- The structural deficit will only get worse as an ageing population places greater strain on the UK’s pension liabilities. (demographic time bomb)

- Potential negative impact on the exchange rate (link)

- Potential of rising interest rates as markets become more reluctant to lend to the UK government.

However, government borrowing is not always as bad as people fear.

- Borrowing in a recession helps to offset a rise in private sector saving. Government borrowing helps maintain aggregate demand and prevents a fall in spending.

- In a liquidity trap and zero interest rates, governments can often borrow at very low rates for a long time (e.g. Japan and the UK) This is because people want to save and buy government bonds.

- Austerity measures (e.g. cutting spending and raising taxes) can lead to a decrease in economic growth and cause the deficit to remain the same % of GDP. Austerity measures and the economy | Timing of austerity

Who owns UK Debt?

The majority of UK debt used to be held by the UK private sector, in particular, UK insurance and pension funds. In recent years, the Bank of England has bought gilts taking its holding to 25% of UK public sector debt.

Source: DMO Debt Management Report 2022/23

- Overseas investors own about 28% of UK gilts (2022).

- The Asset Purchase Facility is purchases by the Bank of England as part of quantitive easing. This accounts for 26% of gilt holdings.

Total UK Debt – government + private

- Another way to examine UK debt is to look at both government debt and private debt combined.

- Total UK debt includes household sector debt, business sector debt, financial sector debt and government debt. This is over 500% of GDP. Total UK Debt

Private sector savings

When considering government borrowing, it is important to place it in context. From 2007 to 2012, we have seen a sharp rise in private sector saving (UK savings ratio). The private sector has been seeking to reduce their debt levels and increase savings (e.g. buying government bonds). This increase in savings led to a sharp fall in private sector spending and investment. The increase in government borrowing is making use of this steep increase in private sector savings and helping to offset the fall in AD. see: Private and public sector borrowing

Comparison with other countries

Although 107% of GDP is high by recent UK standards, it is worth bearing in mind that other countries have a much bigger problem. Japan, for example, has a National debt of 256%, Italy is over 157%. The US national debt is over 132% of GDP. [See other countries debt].

How to reduce the debt to GDP ratio?

- Economic expansion which improves tax revenues and reduces spending on benefits like Job Seekers Allowance. The economic slowdown which has occurred since 2010 has pushed the UK into a period of slow economic growth – especially if we consider GDP per capita growth. Therefore the further squeeze on tax revenues has led to deficit-reduction targets being missed.

- Government spending cuts and tax increases (e.g. VAT) which improve public finances and deal with the structural deficit. The difficulty is the extent to which these spending cuts could reduce economic growth and hamper attempts to improve tax revenues. Some economists feel the timing of deficit consolidation is very important, and growth should come before fiscal consolidation.

- See: practical solutions to reducing debt without harming growth

Other countries debt

See also:

Can I ask why our of my tax comes a national Al debt interest payment? I never signed any agreement saying I was liable for interest. I have not seen the agreement. I am not sure if PPI was included in that agreement.

The government bailed out RBS in 2007, but was this because RBS held a substantial amount of Government debt, and if the bank failed the treasury would have to repay that money to the liquidators. Do we know how much government debt RBS holds?

You say this, “In the current climate, the UK would struggle to borrow the same as in the past. ”

However, this is not true. Indeed UK Government gilts are 100% guaranteed safe, the government will always be able to repay any amount – it owns the currency after all!. Indeed in this uncertain climate today, investors are so desperate to move cash to something safe, they are willing to accept just fractions of a percent interest on 2 year and 5 year gilts, rather than invest it in companies.

If anything, the government can (and should be) issuing far more debt, in order to kickstart the economy and get peoples standard of living back to where it was 10 years ago.

I agree to an extent. Certainly, they can borrow more than the current 80% of GDP. What I really meant is levels seen in 1950s of over 200% of GDP.

What I want to know is simply how much of the ‘National Debt’ is owned by people or organisations outside of the UK and how much within…

Look under

>>Who owns UK Debt?<<

I think our national debt is quite simply staggering but at £1.7 trillion? and rising at £5500 per second! it obviously isn’t going to be paid off anytime soon.

You say that reducing government spending isn’t going to reduce our national debt much if at all? Well I can see that because it reduces the amount that people spend in the economy producing government revenue such as VAT. But it also seems more likely that the huge increase in the money supply since the eighties has made it much harder for governments to keep proper control over national debt much of which is fuelled by rapid increases in investment. The trouble is that the credit crunch of 2008/9 has quickly proved how vulnerable ours and other economies are in relation to borrowing too much for investment. It looks as though some of our future plans may have to change regarding this and focus on more manageable priorities to deal with this. There are many ” catch 22s ” involved in the situation but, if the next financial crisis involves a collapse in property prices then that would probably involve much less money being circulated and spent which equally would mean that the national debt would still take many years to pay off and could actually increase it probably. But it still looks as though the world economy cannot go on sustaining such high levels of debt. We cannot also probably relate our current economy to what happened before in any meaningful way.

I love how MMT’ers are putting things right in this page 😉

Anyone who believes that a debt over a £trillion is sustainable in the long run ,and to be paid by future generations not born yet…does not understand economics

Money created by banks from nothing with interest charged for each $£ etc..is not democracy,is immoral,un-ethical..should be made illegal…as is counterfeiting money…which is what modern money is…governments need to create money..debt free and interest free to pay for public services and public infrastructure

Agree. And they can.

But the entire mechanism of money creation & money trading needs an overhaul. However, there is no political party proposing this. Is there a single politician who understands what is required?

You are all missing the point.What will bankrupt Britain is this.

We are coming to the end of a 31 year cycle of low interest rates and cheap money.

We have gone well past the point of no return.

Interest rates are rising.Inflation has returned.

Even if Britain stopped public spending tomorrow,we could never pay the higher interest on our current £1.7 trillion debt pile.

Britain is doomed.Within 5 years it will be poorer than Bangladesh.

It doesn’t matter what interest rates are as amalgam Greenspan said in 2005 solvency is not an issue when the debt is in the same currency that the government can create.

Government debt income is well below any private household debt income ratios but the government has far longer timescales than private households and can create as much money as it needs to buy any goods and services that are for sale in its currency.

As a matter of fact the Bank of England has bought £453 billion of government debt and could easily buy up the rest and then there would be no interest to pay at all.

It has been govt education policy throughout the West to withhold teaching basic economics & How Money Works to unsuspecting students – all the better to screw them throughout the rest of their lives (e.g. Student Debt).

The problem with that is that even those running the economy have little idea how it works, and billionaire bankers are setting their agenda, for no other objective than their own bank balances.

In the past, govts could get wise & correct these trends but banks have now been consolidated, in just one generation, into a small number of enormous institutions, larger & more powerful than most countries. And of course, unrestrained by nuisances such as representative democracy.

Yes, we’ll all get relatively poorer, as we are willingly being taken for a ride and reacting exactly as planned.

To be foretold is to be forewarned.The great evil of the socialost welfare state started foolishly by Lloyd George is over.

the entire fiat monetary system is a scam to its core. created by the criminal elite, to transfer the wealth of the world from the masses to the few at the top. and they have done a very good job of it. the system was designed to fail many years after its creation whilst in the meantime the criminal elite could steadily consolidate its power and wealth. we are coming very close to the point where the system completely fails and a new system, of their design, can be introduced. and its all been part of the plan all along. there is no fix other than to not recognize the existence of any monetary system

One question I have – as National Debt accumulates due to the deficit adding to it, I assume that at the same time that National Debt is slowly been paid back via bonds or gilts maturing, or have I got that wrong. ?

As bonds mature the principal money or capital is repaid but government debt is simply rolled over by issuing new bonds or national savings products, for that matter. The nominal debt keeps increasing unless government tax flows exceed government spending which is a relative brake on the economy compared to the government running a deficit.

The US Federal Reserve Bank is a group of private banks enabled by a law passed by Congress in 1913. The fact that it a cartel of private banks is probably not well understood. My belief is that the increasing US national debt is beneficial to the Fed. When it was created we are told it was modeled on the Bank of England. I understand that our national bank is also a private cartel and not owned by us, the people at all. Thus it is not in Mark Carney’s interest for us to reduce debt.

I’ve read an awful lot about economic theory, and how government debt is sustainable, etc; but most theories miss the vital point. Interest repayments. As it happens this article happens to touch on it, but simply says it is quite affordable. Yes it is, but the more fundamental and moral question one has to ask themselves is why on earth would you want your governments 4th largest spending to be on interest payments. I realise that interest rates are low and that much government debt is long term, which can be inflated away. But the moral question is why would you want to do this? Wouldn’t you want to have a balanced budget with minimal debt. I realise that we are where we are, but why this isn’t even an aspiration is astounding to me?

hi Pierre

Some debt is useful for the economy as a whole. For example, annuity pensions depend upon UK gilts to make their payments to pensioners: they need a risk-free index-linked return and UK index-linked gilts provide that. The government has a responsibility for the economy as a whole and the debt serves a purpose.

The key is whether the debt is affordable, and what the debt is used for. For the first point we need to monitor the debt interest payments to GDP – but also consider how that may change in the future. Because gilts pay fixed interest, the impact of higher base rates drip into the equation over time (as new gilts are issued to cover those maturing).

The second point (what debt is used for) is really important. Borrowing to just maintain services is bad, because it leads to exactly the problems you mention (debt increases; interest payments increase and the UK would get into a vicious circle of ever having to borrow more). However borrowing to invest (spending the money on something that would have a positive effect on the economy) is not (within the limits of affordability). It’s questionable whether governments always invest wisely – but that’s another question entirely.

I meant to add – the UK is no longer borrowing just to maintain services (announced last week for 2017 fiscal year). This is fantastic news and another milestone to full recovery. I’m surprised the news hasn’t been more widely reported.