Readers Questions: is this the worse time to be a young adult in the UK?

I will answer this question primarily from the economic point of view.

The first thought that springs to mind is that if you look at the long history of the UK, this is probably a good time to be young in the UK.

Median incomes are close to an all time high (even despite the fall since since the 2008 crisis), educational opportunities are arguably better than before (even if more expensive), unemployment is relatively low and likely to fall (even if there is greater insecurity in the new job market).

It is always tempting to think that every thing was rosy in the past. But, living standards have consistently risen in the past few decades. It is true, that for the past five years, real incomes have stagnated even fallen, throwing into greater contrast rising living costs, especially housing. However, were the previous generation really better off?

Economic problems facing young people

There are several reasons to be concerned about prospects for young people.

Firstly, housing is a real problem. There is a serious shortage of affordable housing – especially in London and the south. This means that many young people simply can’t afford to buy a house like their parents generation could. Home ownership rates are falling – especially amongst people under 30.

House prices are rising faster than incomes. See more at UK housing market stats – including house price to income ratios. For many young people, buying a house is just an impossibility.

Readers Question. Just saw a video called ‘How to waste £375 billion? (The Failure of Quantitative Easing)’ by Positive Money. I’ve recently started reading your blog and find your posts very informative. I wonder what you make of the ideas in this video and of this group in particular?

(I haven’t seen the video. For some reason I never like watching videos only reading articles.)

I would say Quantitative easing has been a quantified success. Or perhaps a better way of evaluating quantitative easing is that – it could have been worse, if we hadn’t pursued quantitative easing.

A simple comparison is to compare the UK and US (who have both pursued quantitative easing) with the Eurozone (which hasn’t). In the past couple of years, the economic recovery has been stronger in the US and UK, the Eurozone is in danger of a double dip (or triple dip) recession. The Eurozone is heading towards a dangerous period of deflation. The UK and US have at least a better inflation rate.

Eurozone inflation

Therefore, I wouldn’t say we wasted £375 billion. Firstly, ‘wasting’ implies an opportunity cost – for example, finding it from higher taxes or lower spending. It was entirely created. For all its faults and limitations, the quantitative easing we pursued was better than nothing – especially given the degree of fiscal tightening pursued since 2010.

Problems with UK Quantitative easing

Perhaps a better description of UK quantitative easing is a wasted opportunity. True, we avoided some deflationary effects, but there are reasons to be disappointed and perhaps it could have been better.

Banks largely used the newly created money to make a profit from selling bonds to the Bank of England and improve their balance sheets; because of the recession, little of this extra money fed through into the real economy through higher bank lending (see: M4 lending stats). The side effect was some banks and the bond market did very and interest rates are at very low rates. True, low rates are part of the aim behind Quantitative easing, but low interest rates are of limited benefit, if firms are unable / unwilling to borrow and make use of cheap borrowing.

Parts of the financial services industry has benefited very well from quantitative easing. It is perhaps a little galling to see many of those culpable for aspects of the credit crisis gaining bonuses from the benefits of quantitative easing.

However, to say it solely benefited the rich is to ignore the contribution it may have made to reducing unemployment. UK unemployment has fallen for many reasons – the small economic stimulus is an important factor – never forget reducing unemployment is one of the most important factor in reducing relative poverty. The UK unemployment rate is now 50% lower than many areas in the Eurozone.

Would a better form of quantitative easing have been to print a smaller amount of money, but directly use this to finance government budget deficit, and / or fund public sector investment?

Some argue this would have directly led to higher demand and a stronger economy.

The UK grocery market has become increasingly competitive in the past few years. It is a good example of an oligopoly becoming more competitive. Certainly, the growing strength of discount giants like Aldi and Lidl have really shaken up the market and diluted the cosy oligopoly previous enjoyed by the likes of Tesco and Sainsbury. …

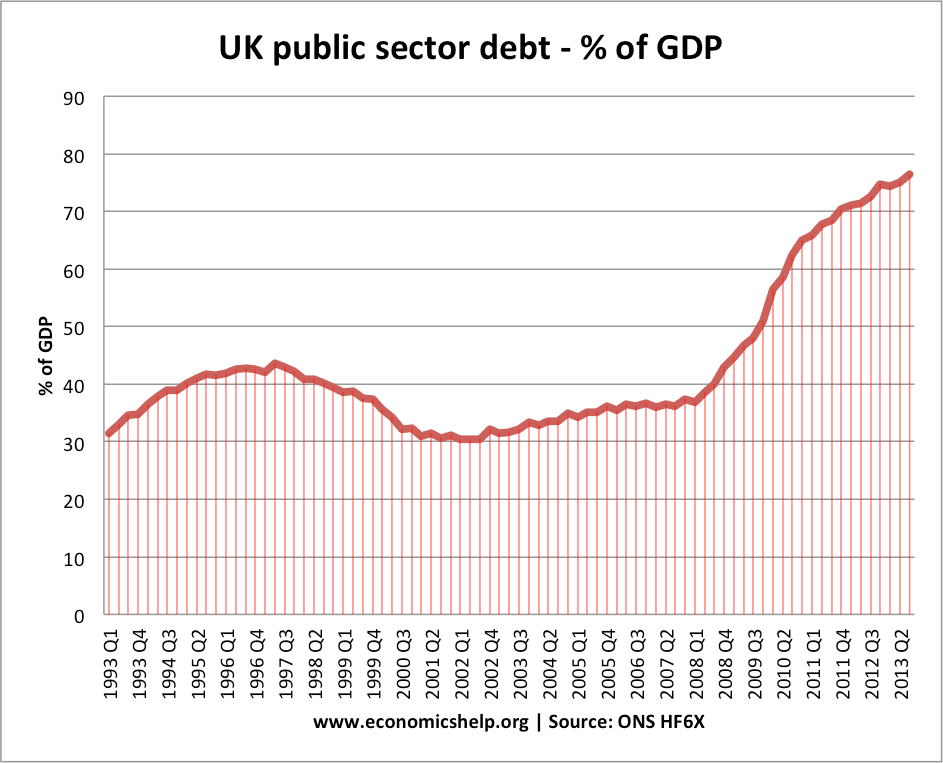

Readers Comment from UK debt under Labour. In 13 years from 1997/8 to 2009/10, the Labour Government increased debt by about £420 billion. In the 5 years from 2010/11 to 2014/2015, the Coalition Government will increase debt by about £600 billion. These are the facts.

Yes, though I’m always nervous about extracting facts like this.

It is true that under the Coalition government of 2010 onwards public sector debt has increased significantly. Debt to GDP has increased at a rapid rate. But, that doesn’t mean it is a reason to blame the coalition government for rising debt. Rising public sector debt was both inevitable and desirable given the poor global economic performance, shrinking tax base and expansionary fiscal policy of the previous government.

I would argue, that 2010-2014 – it’s a shame government borrowing didn’t increase a little more. In a recession, with a fall in private sector spending, and rapid rise in private sector saving – you want to see an increase in government borrowing to help maintain overall demand, especially with Q.E, low inflation and low interest rates,.

Comparing debt levels from 1997 to 2010 and comparing debt levels during the great recession is a very difficult comparison. The economic situation is so different, that the required response needed is also very different.

However, the point about UK debt under Labour. was to make the point that (contrary to many people’s opinion) UK government borrowing had fallen to a near record post-war low in the run up to the credit crunch. Excessive government borrowing was definitely not a cause of the crisis of 2008 onwards.

Economic growth

Another thing that can make me suspicious is when people point to very recent quarterly economic growth figures and claim that as vindication or otherwise of a particular economic policy.

Tight monetary policy implies the Central Bank is trying to reduce the demand for money and limit the pace of economic expansion.

A tightening of monetary policy, could involve an increase in interest rates. – Higher interest rates increase the cost of borrowing and discourage investment and consumer spending. A tightening of monetary policy would be appropriate in a period of positive economic growth and rising inflation, above the inflation target.

Europe has neither. The Eurozone is facing an inflation rate of 0.4% and weak economic growth. However, monetary policy has been relatively tight.

Two graphs from Antonio Fatas help to illustrate this.

Therefore, with base rates of 0.5% and inflation of 4%, the US would have a real interest rate of -3.5% – This negative interest rates, in theory, should be more encouraging for people to spend rather than save.

By contrast, the ECB have had higher real interest rates. This is partly because they increased nominal interest rates in 2013, but mainly because European inflation has been lower. The decline in Eurozone inflation to 0.4% has had the effect of increasing real interest rates.

UK real interest rates have been similar to the US. UK inflation has been higher than Eurozone inflation.

The increase in real interest rates in Europe are a serious cause for concern and a good illustration of one of the problems of deflation / low inflation.

With deflation, monetary policy can become unsuitable. Because you can’t cut base rates below zero, monetary policy can become tighter than market conditions allow.

Unfortunately the higher real interest rates and the tightening of monetary policy makes deflation more likely. It is a vicious circle.

Q2: Why are there millions of people unemployed even when the economy is booming? During periods of strong economic growth, we can often experience high rates of unemployment. Firstly, there may be structural unemployment. This occurs when the unemployed are unsuited or unable to fill job vacancies. For example, a booming economy may have a …

Readers Question: You have partially explained the answer to my question in your reply to my other question, “What will we do when we can’t pay back the money owing to the government bond holders when they reach the end if their term”. While I appreciate the convenient use of the debt to GDP ratio I feel that it tends to sidestep the truth about the remaining debt. This is almost like the government using the reduction in the deficit rather than the reality of remaining, possibly increasing debt.

For some reason, the first thing that comes into my mind is the famous quote from Dr Strangelove – “how I learned to stop worrying and love the bomb (debt)”

I guess we can blame Charles Dickens and Wilkins Micawber from David Copperfield.

“Annual income twenty pounds, annual expenditure nineteen pounds nineteen and six, result happiness. Annual income twenty pounds, annual expenditure twenty pounds nought and six, result misery.”

No matter how much you talk about government debt, people won’t feel comfortable until we have a zero budget deficit and zero government debt. – (even though, I don’t think any modern economy has ever had such a situation – nor would one be particularly desirable.) Many issues are addressed here: The political appeal of austerity.

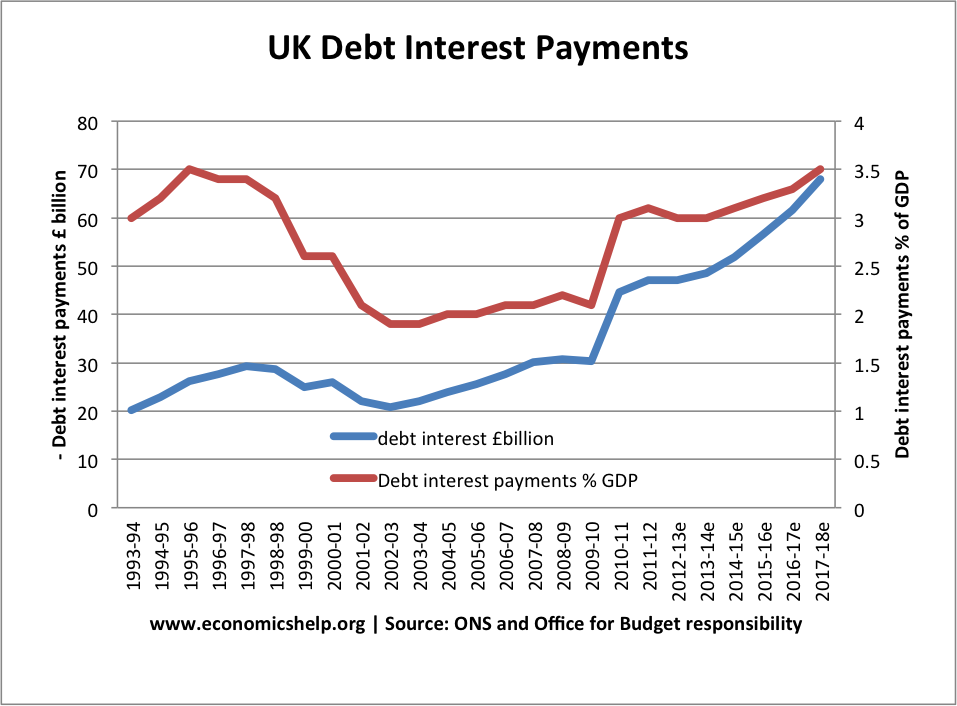

What does debt cost?

Another way of thinking about government debt is the annual cost of servicing the debt. What percentage of GDP is spent on debt interest payments? What percentage of tax revenues is spent on servicing the debt? You could have an increase in the real value of debt, but a smaller percentage spent on paying interest on the debt. Would you worry about a mortgage – if every year the monthly mortgage payments were becoming a smaller percentage of your disposable income?

The cost of servicing UK debt has risen in the past few years, due to rise in debt. But, by historical standards, it is still quite low and certainly quite manageable. More on Cost of borrowing

Of course, the cost of debt interest payments also depend on interest rates. A rise in interest rates will cause higher borrowing costs. But, with low interest rates predicted, we are unlikely to see a jump in borrowing costs – at least in the medium term.

The German economy has been one of the world’s strongest economies in the post-war period. There are many aspects of the German economy which deserve praise and emulation – not least strong productivity growth, a booming export sector and prolonged low inflationary growth. In the post-war period Germany has played an important role in promoting economic stability and prosperity within Europe.

But, in recent years, the German economy has seen several cracks appear and German economic thinking is now causing a major drag on Eurozone economic growth and prosperity.

The false goal of a balanced budget

An very important issue in German politics is the desirability of seeing a balanced budget (government spending = government tax revenue). Many German finance ministers have made balancing the budget their primary economic objective. In the UK and US, we see that austerity has a strong political appeal – but in Germany the appeal of ‘responsibility’ and avoiding debt is perhaps even greater. A German friend told me that there is a certain guilt attached to the idea of holding on to debt. (though this guilt is especially felt with government debt – mortgages and business loans are somehow different)

On the objective of reducing budget deficits Germany has been successful. It is also keen to enforce EU rules and the idea of encouraging a balanced budget for its struggling European neighbours.

Angela Merkel recently stated to the EU Parliament, that EU rules must be met:

“All, and I stress again all, member states must respect in full the rules of the strengthened stability and growth pact,” she said. “These rules must be applied credibly to all member states — only then can the pact fulfill as a central anchor for stability and above all for confidence in the eurozone.” (US Today)

Although, Merkel did not name France, the implication was that France must do more to meet the EU Stability and growth pact.

Why is a balanced budget a false goal?

1. Lack of investment

A successful business does not have its objective to borrow nothing. A successful business knows that it needs to invest to make progress and retain its prosperity. Years of cutting government spending has meant that Germany has cut back substantially on public sector investment. There are widespread reports that Germany has a lack of investment in roads, bridges and other forms of transport. There is a fear that important infrastructure, such as roads and bridges are reaching the end of their 70 year cycle, but there is no money to successfully replace them. The economic problem is growing congestion, time wasted and damage to the long term productive capacity of the economy. The Guardian notes

Its (German) investment rate in 2013 was the fourth lowest in the EU; only Austria, Spain and Portugal spent less. Fratzscher, who is head of the German Institute for Economic Research, calculates there is an “investment gap” of €80bn (£63bn).

The Economist reports that German public sector investment is —a paltry 1.6% of GDP— one of lowest in Europe and has fallen since 2009.