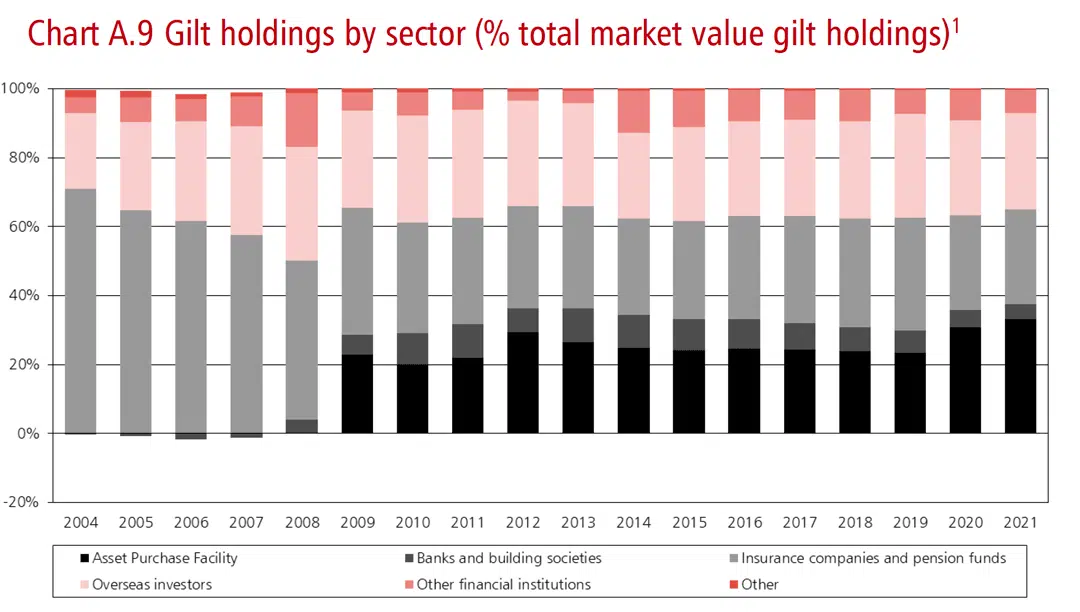

One of the most common questions asked is, who owns UK National Debt?

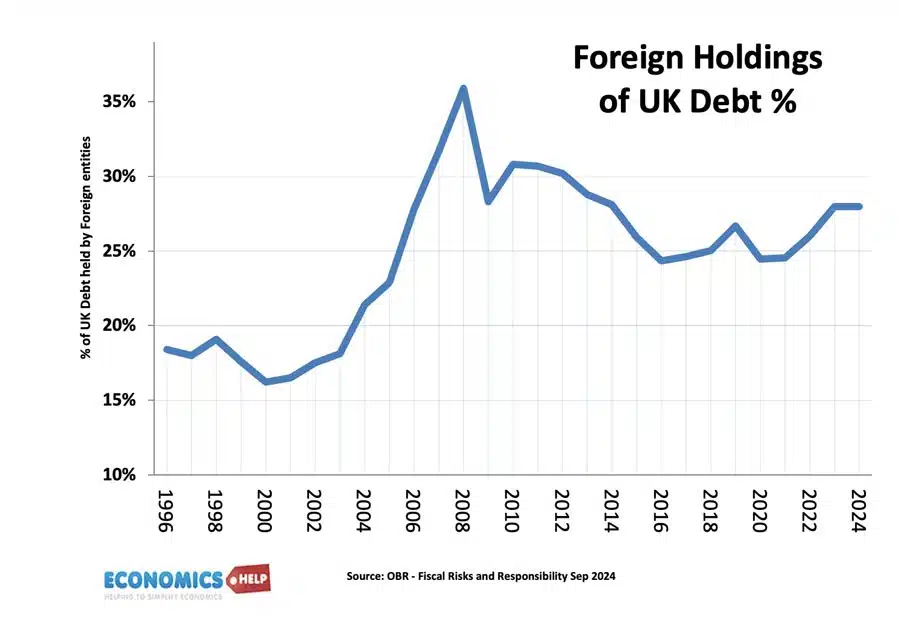

Often people assume that UK government debt is owned by foreign investors. However, foreign investors only hold about 25-30% of UK government debt. The rest is held by the UK private sector (pension funds, insurance companies e.t.c). Recently, the Bank of England has also been purchasing Gilts under the Asset Purchase Scheme.

In the past few years, the proportion of UK government debt held by overseas investors has been about 30%.

Source: HM Treasury

For 2021, debt held by Overseas investors is 28% of GDP

The Asset Purchase Facility is purchases by the Bank of England as part of quantitive easing. This accounts for 26% of gilt holdings.

A different, but similar, concept is external debt. This is the total amount of UK debt (both private sector and public sector) held by overseas agents.

In 2000-01, several years of government spending restraint combined with rising economic growth, saw government spending shrink to under 35% of GDP. Between 2001 and 2007-08, spending rose to over 40% of GDP due to sustained increases in spending on health, education and welfare spending.

In 2007/08 the financial crisis and subsequent recession led to higher spending as ratio of GDP – even though the new Conservative government pursued austerity and sought to cut government spending or limit spending in many areas.

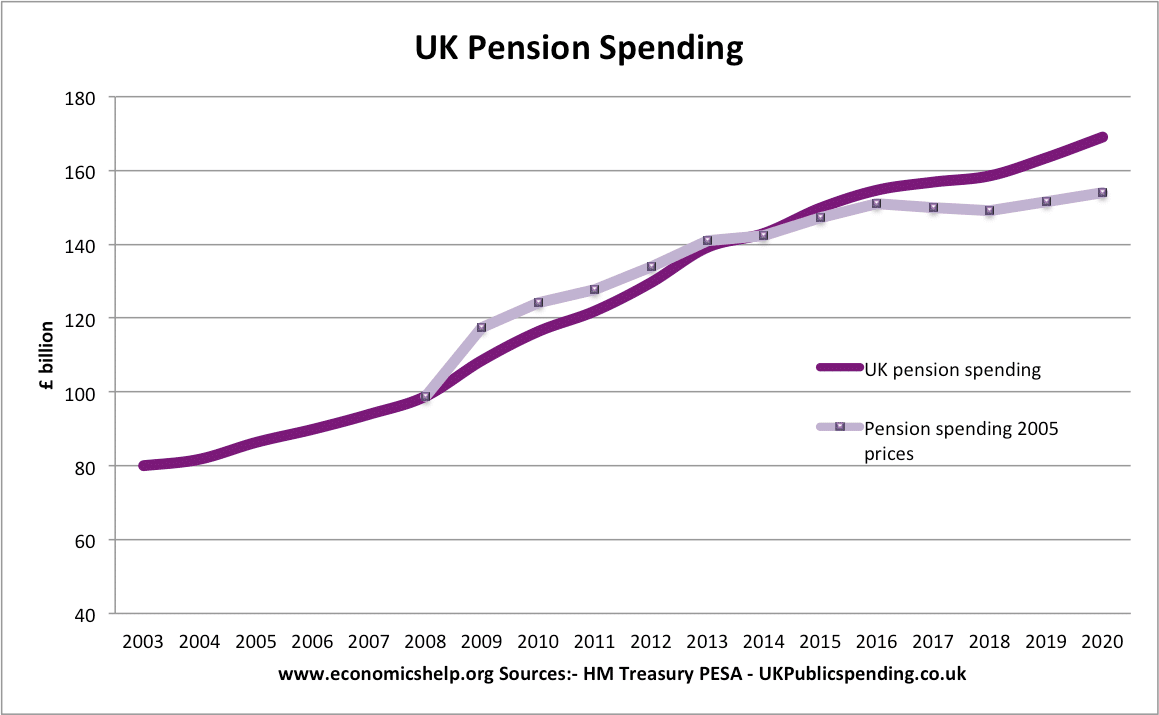

Real term trends in public spending

Health care has been the biggest source of growth since 2010. Social protection, which includes pensions has been flatter since 2010 because of low real income increases in welfare benefits.

Source HMT Public spending statistics (May 2022) UK Pension spending

Between 2008-09 and 2009-10, the UK saw a large drop in real GDP of 6%, but due to automatic stabilisers government spending increased (e.g. higher unemployment benefits). This caused government spending as % of GDP to rise to 47%.

Government spending as % of GDP is forecast to fall closer to 40% of GDP by 2016-17 (if growth targets are met)

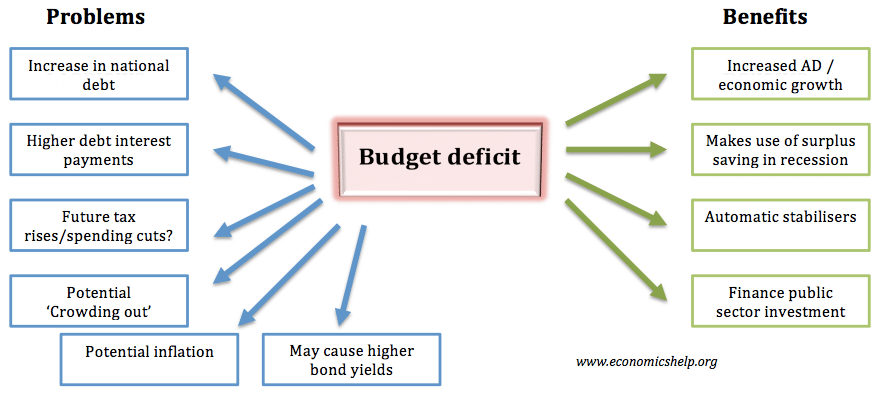

Readers Question: How important is the budget deficit?

The budget deficit is the annual amount the government borrow. The government usually financed the budget deficit by selling bonds to the private sector

To libertarian and free-market economists, budget deficits are liable to cause significant economic problems – crowding out of the private sector, higher interest rates, future tax rises and even potential for inflation. However, Keynesian economists are more sanguine arguing that in an economic downturn, a budget deficit plays an important role in stabilising economic growth and limiting the rise in unemployment.

Budget deficits have potential economic costs, but it depends on the economic climate, the exchange rate system, interest rates and the reason for government borrowing.

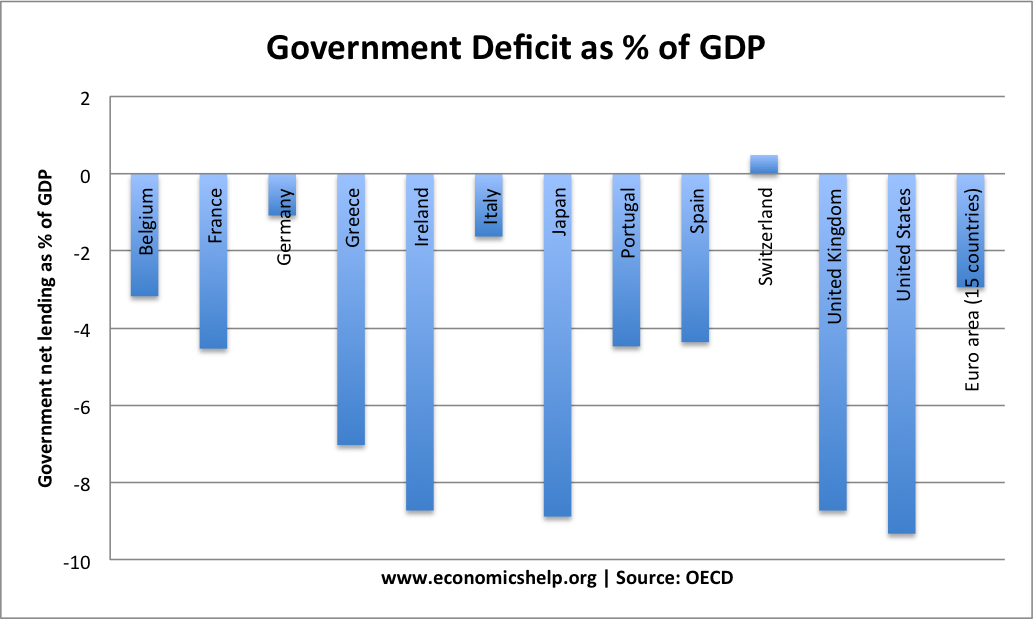

The most useful way of measuring the size of the budget deficit is as a % of GDP. The graph below shows that in 2012, there was a large variance in the size of budget deficits. The biggest deficits occurred in Ireland, Japan, UK, and US – with budget deficits of over 8% of GDP.

Potential benefits and costs of a budget deficit

Reasons to be concerned about a budget deficit

Need to cut spending in the future. Higher deficits are not sustainable forever. Reducing a budget deficit can be problematic. If a country has a deficit that increases too quickly, the government may be forced to adapt policies aimed at a sharp deficit reduction. These ‘austerity measures’ can cause a fall in aggregate demand. For example, during 2012-16, many countries in the Eurozone sought to reduce their budget deficit to comply with EU rules. This deficit reduction caused lower growth, recession and unemployment.

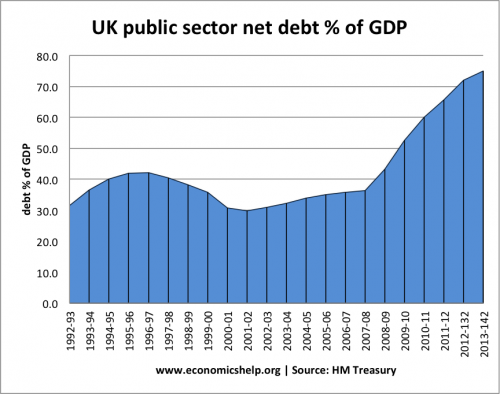

Increasing national debt. A budget deficit increases the level of public sector debt. Large deficits will cause national debt as a % of GDP to increase.

Opportunity cost of debt interest payments. A higher deficit will also lead to a higher % of national income being spent on debt interest payments.

Crowding out. One way of thinking about a budget deficit is that if the government is borrowing from the private sector, the private sector has lower funds to spend and invest. The government is, therefore ‘crowding out’ the private sector – and some economists will argue government spending is liable to be more inefficient than the private sector.

Potential rise in bond yields. Countries with large deficits may struggle to attract sufficient investors to buy bonds. If this happens, bond yields will rise causing the deficit to be more expensive to finance.

Potential inflation. There is a fear that budget deficits could be inflationary. For example, if a country like the UK was struggling to attract sufficient investors to buy UK bonds, the Central Bank could effectively print money and buy bonds. However, unless the economy is in a liquidity trap, printing money will cause inflation, and reduce the value of savings, including government bonds. It is worth pointing out, that in developed economies – inflation from printing money resulting from a budget deficit is quite rare.

Confidence effects. High levels of government borrowing may adversely affect confidence as consumers and firms fear future tax rises or higher interest rates.

Evaluation

There is no simple answer to whether a budget deficit is helpful or harmful because it depends on quite a few factors.

1. It depends on when the deficit occurs. Basic Keynesian analysis suggests that a rise in the budget deficit during a recession is a good thing. In a recession, private sector spending falls and saving rises – leading to unused resources. Government borrowing is a way of utilising these unused savings and ‘kickstarting’ the economy. The deficit spending can help promote higher growth, which will enable higher tax revenues and the deficit will fall over time. If you try to balance the budget in a recession, you can make the recession deeper. Austerity can be self-defeating.

Is there a link between government debt and the interest rate on government bonds? One argument we often hear is that if government borrowing increases – we can expect higher bond yields. Investors demand higher yields to compensate for the risk of government default. However, other economists argue this is misleading. If inflation is low, …

Government debt under Labour was a major factor in the elections of 2010 and 2015. But to what extent did the Labour government really plunge the economy into debt during 1997-2007?

Usually, when people say ‘it’s debt that got us into this mess’. They tend to view all types of debt as the same – equating government debt to financial debt incurred from selling sub-prime mortgages in the US. However, this is deeply misleading. The consequence of bad debt defaults in the financial system is very different to government debt financed through selling bonds.

Government debt

In 1997, public sector debt as % of GDP:

1997/98 – 40.4% of GDP

2007/08 – 36.4% of GDP

2010/11 – 60.0% of GDP.

May 2019 – 82.9% of GDP

At the start of the great recession in 2007, public sector debt had fallen from 40.4% of GDP to 36.4% of GDP. This was despite increased real government spending. After the start of the crisis, public sector debt almost doubled in the space of three years.

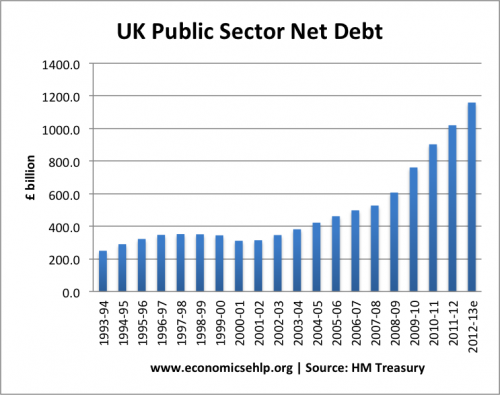

If we look at just actual government debt, there is a significant increase.

In 1997, the total public sector debt was:

1997/98 – £352 bn

2007/08 – £527 bn

2010/11 – £902 bn

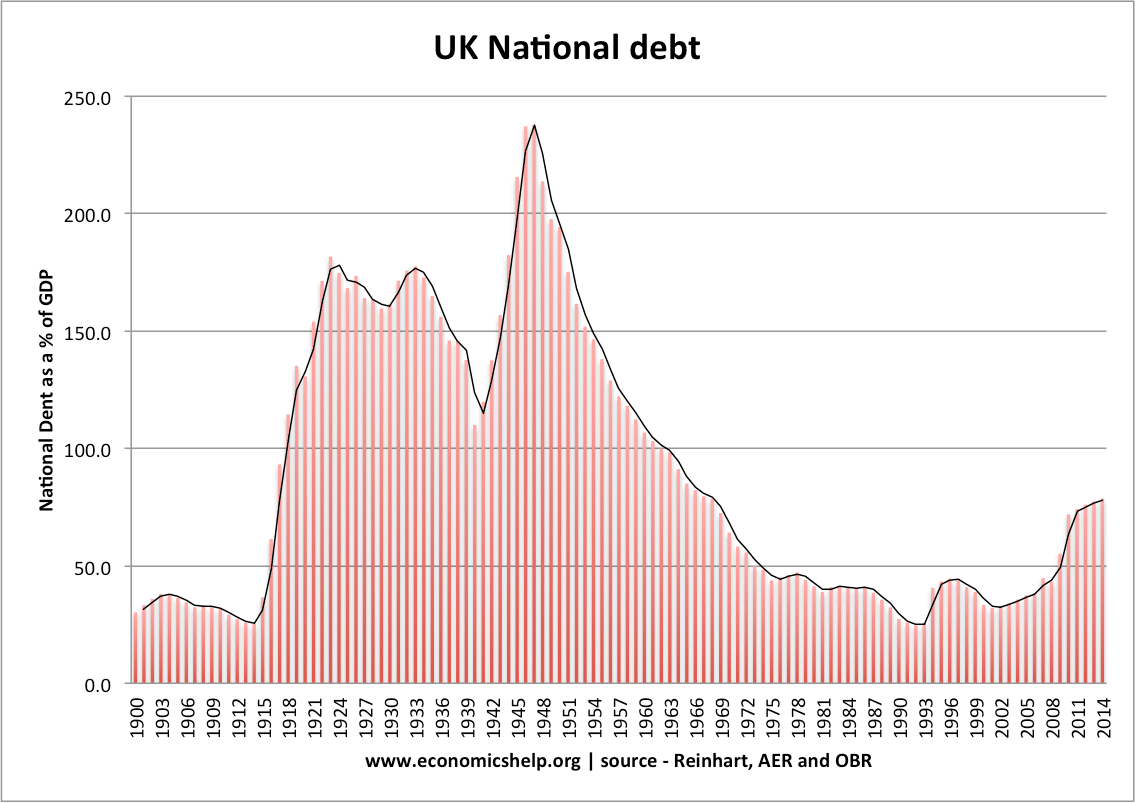

Debt to GDP statistics were helped by the period of strong economic growth – a reminder that economic growth is as important at debt levels. It is also worth bearing in mind UK public sector debt in comparison to the post-war period.

Readers Question. Can Labour be blamed for the economic crisis (i.e. did they really ‘overspend’)? My view is that the global economic crisis is to blame, and that Labour could have spent less but that this is easy to say with the benefit of hindsight. I don’t think there is any economist who would try …

Readers Question: Does Government debt matter? Do high fiscal deficits threaten economic stability?

Summary

Many worry that high levels of government debt could cause economic instability. In certain occasions, countries with high debt have seen investors lose confidence, leading to higher bond yields and putting pressure on the government to slash spending, for example, several countries in the Eurozone (2010-12). In rare cases, governments with high debt have responded by printing money – causing inflation to spiral out of control, for example, Germany in the 1920s. Another potential problem is when government debt is financed by overseas borrowing. If overseas investors lose confidence and sell their debt it can cause a loss of foreign exchange and a destabilising devaluation.

However, in many cases, high levels of government debt do not cause instability – but can actually prevent a deeper recession. The main argument for government borrowing is that in a recession, government borrowing and government spending can help prevent a collapse in demand and economic growth. In a recession, generally, people save more and so wish to buy government debt. This means governments can often borrow cheaply to finance public sector works.

In the 1950s, national debt in the UK reached 200% of GDP, but it did not compromise economic growth or inflation. The UK was able to reduce this debt burden over several decades of economic growth.

Does debt matter?

It depends on how it is financed – e.g. does it rely on overseas borrowing which can be riskier?

What are the prospects for economic growth? – With economic growth, the debt to GDP ratio is likely to fall. If you are stuck in recession, the debt to GDP ratio will likely rise.

Are domestic investors willing to buy government bonds? Japan has very large public sector debt, but it has a large pool of domestic savings so the government has been able to borrow cheaply.

Is the debt cyclical or structural? Debt is a bigger problem if the government is borrowing heavily during a period of growth and there is a structural deficit.

More detail on question

Economic stability would involve.

Low inflation

Positive, sustainable economic growth (e.g. close to long-run trend rate of growth)

Stable bond yields (i.e. avoid rapidly rising bond yields which could create difficulty in dealing with debt.)

Stable exchange rates

High fiscal deficits mean the government is forced to borrow a large sum – Annual government spending is greater than tax revenues.

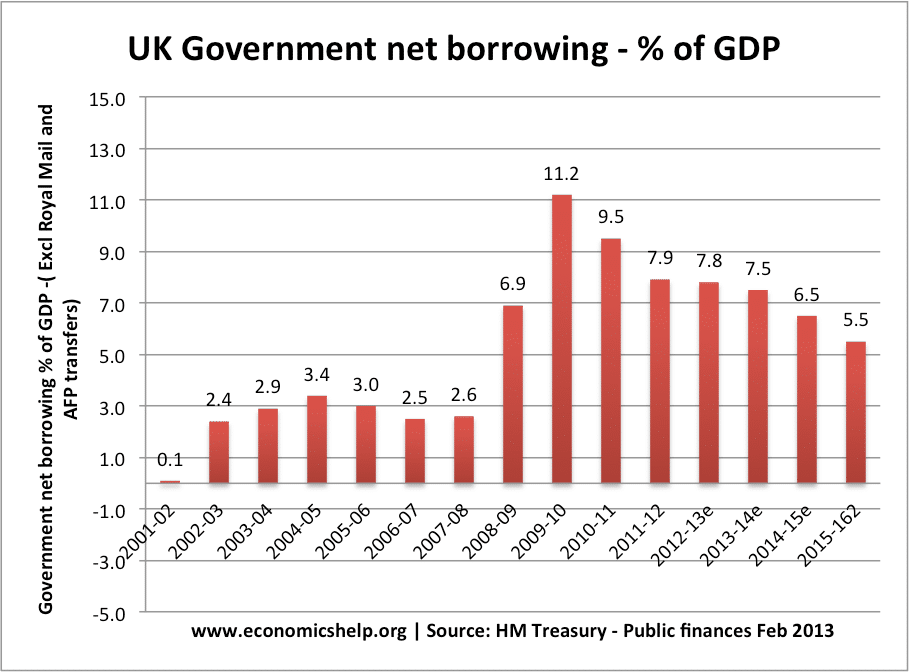

For example, in 2011/12 the UK government will have to borrow an estimated £125bn (just under 8% of GDP). Anything over 3% of GDP could be classed as a high fiscal deficit.

The economic cycle plays an important role in determining the level of government borrowing, especially in the short run. Essentially, higher economic growth leads to lower government borrowing, but a recession will increase government borrowing. Over the past few years (2008-12) – the idea that an economic downturn increases government borrowing is probably one of …