A look at the nature of the UK economic recovery. Is the recovery sustainable? Who has benefited the most from recovery? Which groups of people have not benefited from the recovery?

In the past two years, the UK economy has posted relatively impressive growth figures.

The UK posted annual growth of 2.6% between Q3 2014 and Q3 2013. ONS

It is impressive compared to Europe, which is stuck in recession. However, the recovery is less impressive when compared to the lost output since the start of the recession and the long delay that occurred before the economy started to catch up the lost ground.

The recovery has led to a significant decline in unemployment, whilst at the same time leading to low inflation (CPI = 0.5%).

From one perspective this looks very good – the main three macro-economic objectives (growth, unemployment, inflation) are posting good statistics.

However, the UK recovery is still unbalanced and there are uncertainties about its sustainability. The main areas of concern about the UK economic recovery are:

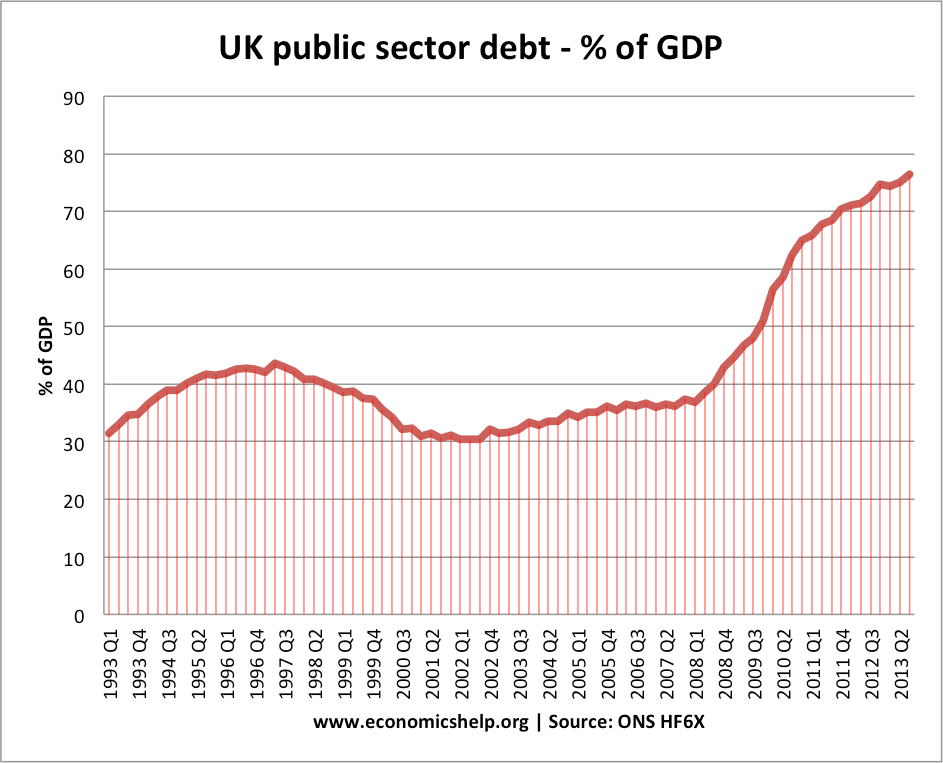

Readers Comment from UK debt under Labour. In 13 years from 1997/8 to 2009/10, the Labour Government increased debt by about £420 billion. In the 5 years from 2010/11 to 2014/2015, the Coalition Government will increase debt by about £600 billion. These are the facts.

Yes, though I’m always nervous about extracting facts like this.

It is true that under the Coalition government of 2010 onwards public sector debt has increased significantly. Debt to GDP has increased at a rapid rate. But, that doesn’t mean it is a reason to blame the coalition government for rising debt. Rising public sector debt was both inevitable and desirable given the poor global economic performance, shrinking tax base and expansionary fiscal policy of the previous government.

I would argue, that 2010-2014 – it’s a shame government borrowing didn’t increase a little more. In a recession, with a fall in private sector spending, and rapid rise in private sector saving – you want to see an increase in government borrowing to help maintain overall demand, especially with Q.E, low inflation and low interest rates,.

Comparing debt levels from 1997 to 2010 and comparing debt levels during the great recession is a very difficult comparison. The economic situation is so different, that the required response needed is also very different.

However, the point about UK debt under Labour. was to make the point that (contrary to many people’s opinion) UK government borrowing had fallen to a near record post-war low in the run up to the credit crunch. Excessive government borrowing was definitely not a cause of the crisis of 2008 onwards.

Economic growth

Another thing that can make me suspicious is when people point to very recent quarterly economic growth figures and claim that as vindication or otherwise of a particular economic policy.

The UK recovery paints an unusual situation. We have both positive economic growth and falling real wages. How can we have economic growth with falling real wages?

Real wages are not the only source of economic growth. We can see growth from other components of AD –

I (Investment), G (Government spending) plus net exports (X-M)

Also, it is possible for consumer spending to rise despite falling real wages (at least in the short term). For example, if spending is financed by borrowing or declining savings ratio. Consumer spending could also be financed through re mortgaging houses (equity withdrawal) against the backdrop of rising house prices.

Economic growth in the UK

Since 2013 Q1, we have seen a decent rate of economic recovery. In the past 12 months – between Q2 2013 and Q2 2014, GDP in volume terms increased by 3.2%

Real wages

Real wages have been falling since the start of the great recession in mid 2008. In a recessing falling real wages are to be expected, but since the recovery, we might have expected real wages to match the growth in real GDP.

Why are real wages falling despite economic growth?

1. Flexible labour markets creating low paid employment. In this recovery, unemployment has fallen more rapidly than previous recessions. Evidence suggests the economy has been successful in creating new employment (often temporary / part-time/ self-employment). These new jobs are not particularly well paid. The recovery is good for job-seekers, but less good for those already in work. The relatively elastic supply of labour willing to take low paid jobs is keeping any wage growth low.

Readers Question: What is the economic impact of proposed welfare benefit freezes proposed by Chancellor, Mr Osborne?

Mr Osborne has proposed a welfare freeze, worth £3 billion of savings over two years. This benefit freeze includes Jobseeker’s Allowance, Income Support, Child Tax Credit and Working Tax Credit, Child Benefit and Employment Support Allowance (paid to those judged capable of work). It does not include pensions, disability benefits and maternity pay.

The Treasury said that about 10 million households would be affected, roughly half of which are working.

The freeze will raise around £1.6bn in 2016/17, rising to around £3.2bn a year in 2017/18.

An argument for freezing welfare benefits is that it will help reduce the budget deficit and also – since 2007, average earnings (+17%) have been rising at a slower rate than working-age benefits (+22%.)

Economic effects

Aggregate Demand (AD) / economic growth. Welfare freezes will (ceteris paribus) reduce consumer spending, and lead to lower aggregate demand. It is an example of deflationary fiscal policy. It will be quite significant because people receiving welfare benefits have a high marginal propensity to consume because, on low incomes, they don’t have the luxury of saving – therefore, lower welfare benefits will directly lead to less spending in the economy. Welfare freezes will also contribute to a decline in consumer confidence because it will be a visible reminder of economic hardship. Combined with other spending cuts of up to £24bn, there is still scope for these planned spending cuts to derail the economic recovery and cause lower growth or even a future recession.

However, the strength of the recent recovery suggests the UK may be in a better position to absorb austerity than a few years ago. Also, the chancellor can rely on the Bank of England to maintain a very loose monetary policy, which will help to offset the impact of this deflationary fiscal policy.

However, we still don’t know the position of the economy in a couple of years. there is evidence that the recovery still is unbalanced with low productivity growth and low real wage growth making the economy still vulnerable. Continued recession in Europe could also act as a drag on the UK economy; it is possible that these commitments to spending cuts could hold back economic growth, that even monetary policy can’t overcome.

Deficit reduction. The spending cuts will contribute £3bn to saved spending, helping to reduce the budget deficit. However, it is still a small % of the current budget deficit (£93bn). Also, the reduction in deficit may be less than planned because it will cause a fall in tax revenues (e.g. less VAT receipts from lower spending) and also lower economic growth from the austerity measures.

Some economists argue that deficit reduction is essential and there is no alternative but to cut spending. They hope that cutting the deficit will reassure markets and business about the long-term strength of the economy. Other economists argue that recent evidence suggests people don’t gain confidence from austerity – but actually the opposite. (see: Confidence fairy)

If Scotland gains independence, the Yes campaign has argued that their preferred option is to keep the Pound Sterling and enter into a currency union with the rest of the UK.

This means sharing the same currency Pound Sterling, and having the same monetary policy. Monetary policy would continue to be set by the Bank of England. There would be no exchange rate between the two countries.

Currency Union with the rest of the UK

However, currency unions are problematic. The Eurozone has been a disaster for many European countries who have been saddled with high unemployment and stagnant economies. See all problems of Euro here.

A big problem with currency unions is that in the absence of a lender of last resort, you face pressure to limit budget deficits. Since the Euro was created, Southern Europe has been pushed into more austerity than is desirable. It has left their economies vulnerable and with limited options to deal with trade imbalances and economic downturns.

The Bank of England governor, Mark Carney insisted a currency union with a sovereign, independent Scotland was impossible. “You only have to look across the Continent to look at what happens… A currency union is incompatible with sovereignty.” (Guardian)

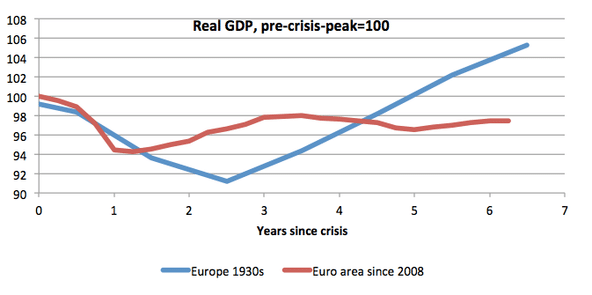

Paul Krugman has stated there are great risks of sharing a currency.

Economists (starting with my late colleague and friend Peter Kenen) have long argued that sharing a currency without fiscal integration is problematic; the creation of the euro put that theory to the test. And the results have been far worse than even the harshest critics of the euro imagined, with euro Europe doing worse at this point than Western Europe did in the 1930s:

Krugman goes on to argue that Scotland’s position could be worse than the Eurzone because there is no guarantee that the Bank of England will be interested in acting like Mario Draghi in his support for debtor countries.

An independent Scotland would be dependent on the kindness of the Bank of, um, England, with no say whatsoever in that bank’s policy. (Scotland and the Euro omen)

Currency unions also exacerbate political tensions. People in southern Europe feel let down by economic policy of the ECB and northern Europe. Germany on the other hand is not happy with the perceived need to bailout its profligate neighbours. Currency unions have not been an effective system for encouraging harmony amongst nations – in fact the opposite. There is a real fear that after independence – Scotland could feel exacerbated and frustrated at being at the mercy of English monetary policy.

But could a currency union between Scotland and the UK work?

Me underneath statue of Adam Smith in Edinburgh

There are some reasons to believe that a currency union between Scotland and the UK would work better than the Eurozone.

Firstly, there is much better labour mobility between Scotland and England than say between Greece and Germany. If the Scottish economy is relatively depressed, workers could move south and vice versa.

A big problem of the Eurozone was the divergence in wage costs and relative prices. This left southern Europe uncompetitive but without the option of devaluation to restore competitiveness. This is perhaps less likely to be a problem between Scotland and England. If there is a significant divergence in wage costs, readjustment is easier because of the greater capital and labour mobility.

Useful post from Paul Krugman about a comparison between the French and UK recoveries. It stems from comments by a Conservative cabinet minister that ‘the French economy is being run into the sand.’ For those who can’t get past the NY Times paywall, I’ll post the two graphs here. UK and France since 2010 The …

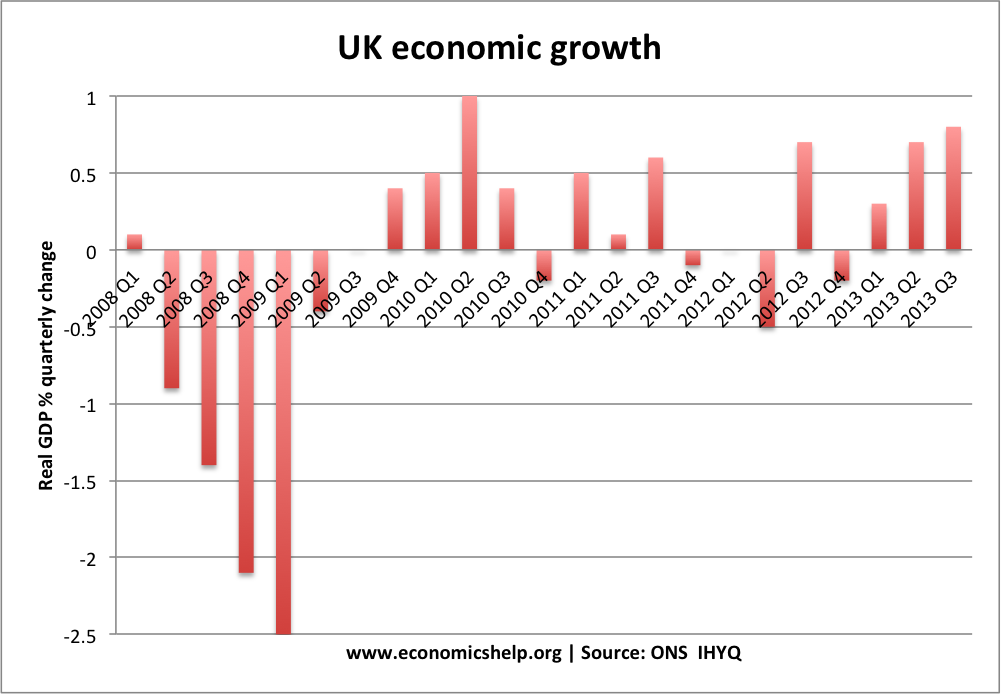

After faltering for several years, the UK economy shows signs of real recovery, with rising spending, investment, exports and even manufacturing growth. At the start of 2014, there seems to be a virtuous circle of falling unemployment, falling inflation, and rising GDP.

After one of the longest and deepest recessions on record, these signs of economic growth are definitely welcome, yet it is far from a return to normality. Real GDP is still 2% below its 2008 peak, and the economy is being propped up by zero interest rates, quantitative easing and a strong housing market. Stagnant wages and poor productivity growth have led to one of the most prolonged periods of declining living standards in memory. Although there is economic recovery, there is still a fear that the recovery is unbalanced, and that the UK economy could be derailed by problems in the Eurozone and future government austerity measures.

The ONS have recently revised annualised economic growth to indicate an annual growth rate of 1.9%. Still below trend rate, but welcome after the several years of falling GDP. For 2014, the OBR forecasts economic growth of 2.4% (BBC link)

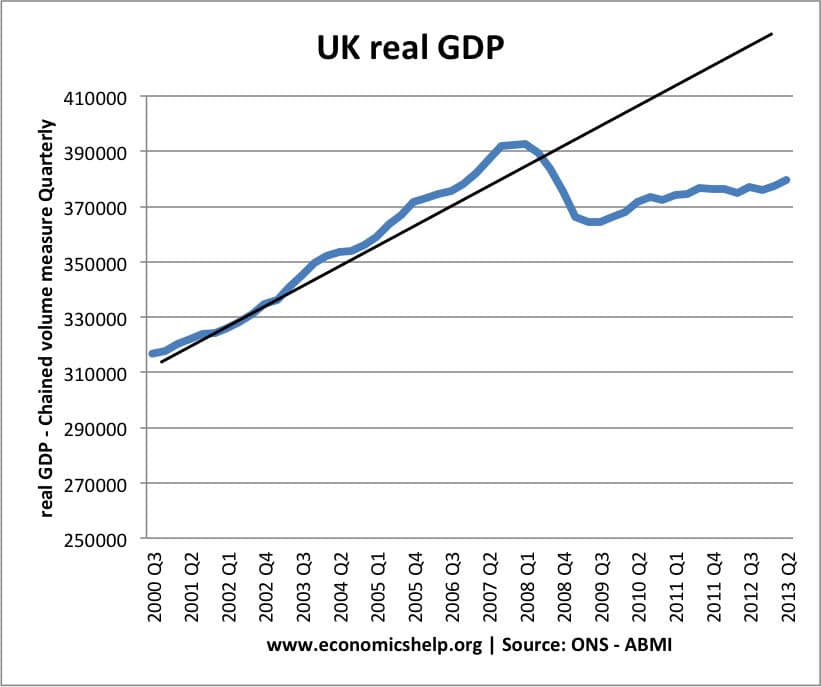

A difficult question is how much of an output gap the UK has. Since 2008, GDP has fallen away from the trend rate of growth. In theory, with output much lower than potential GDP, we would expect a rapid recovery to ‘catch up’ the lost GDP. However, we are unlikely to see this. The great recession has unfortunately led to a permanent loss in real GDP. Economists debate how much spare capacity the UK has. But, for the moment growth rates of 2.5% are unlikely to cause any significant inflationary pressure.

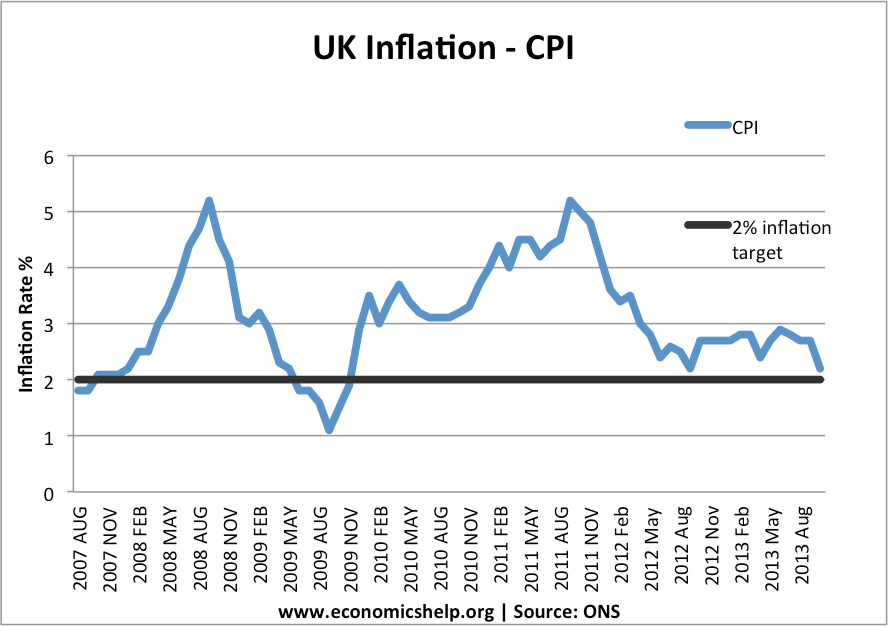

It is ironic that now we are experiencing economic recovery, headline inflation is finally falling closer to the government’s inflation target. of 2%. During the great recession, inflation was often above target due to cost push factors, such as depreciation, rising oil prices and higher taxes. But, now these cost push factors have evaporated, inflation has fallen to 2.1%. Given the nature of the economic recovery, inflation is likely to stay low in 2014, helped by low inflation expectations.

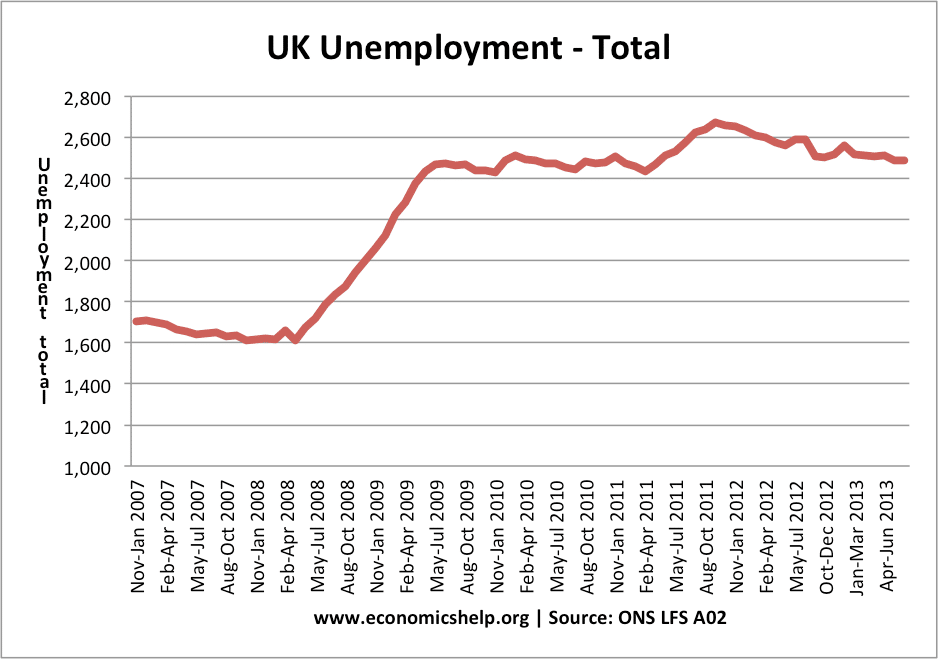

Compared with the rest of the Eurozone, UK unemployment could almost be considered a success story. Unemployment has fallen to 7.4% (2.39 million). There is a record number of people in employment (over 30 million for the first time)

However, whilst this unemployment rate is relatively low compared to Europe and also compared to previous recessions, there are other aspects which make less positive reading. Low unemployment has been helped by a rise in part-time employment, temporary contracts, greater job insecurity and falling productivity. (see UK Unemployment mystery) Also, there are pockets of high unemployment, especially in the north, inner cities and amongst the young. Unemployment of 2.39 million is still a serious social problem, and it will need a considerable period of economic expansion to help reduce to more manageable levels.

Nevertheless, temporary work is still better than no work. Flexible labour markets have many drawbacks, but it is quite interesting that during the shallower recessions of the 1980s and 90s, unemployment rose to a much higher level. There are also promising signs of firms hiring more workers in areas such as, marketing, sales and business development (FT link) which indicate sign of optimism.

Readers Question: Seeing the recent releases of positive UK data come through, I’ve been thinking whether these are signs of a recovery or it is too soon to say. To what extent is the recent run of positive data across sectors a sign of a balanced & sustained recovery in the UK? (question 7th. Nov)

It is a good question. If we look back to 2010, there were signs of economic recovery, but this was not sustained – with the economy going back into recession. In 2013, the evidence is mixed though a little more hopeful. In summary, the UK economy recovery is being primarily driven by consumer spending, the service sector and a vibrant housing market (especially in London). There is weaker growth in manufacturing, exports and investment. The economy is also being helped by ultra-loose monetary policy (Q.E. and zero interest rates). Fiscal policy is more neutral, though over the next few years, the government plans to restrict the growth in government spending so this is liable to be a drag on growth.

These blog posts are also relevant to this question:

A key feature in the nature of the recovery will be the health of the banking sector. The sharp fall in bank lending was a major factor behind the prolonged recession of 2008-12. Signs of improved bank lending will help the economy. However, although mortgage lending shows signs of growth, this is less helpful than bank lending to business. For sustained recovery, increased mortgage lending and squeezing house prices higher is not particularly helpful. Squeezing house prices higher through increased mortgage lending is not increasing productive capacity. If anything rising house prices in London are reducing geographical mobility and the cost of housing in London will adversely hurt the London labour market. Also, house price to income ratios (especially in the south) are close to historical highs; some fear house price growth is unsustainable. Any fall in house prices would knock consumer confidence and spending.

Real Wage growth

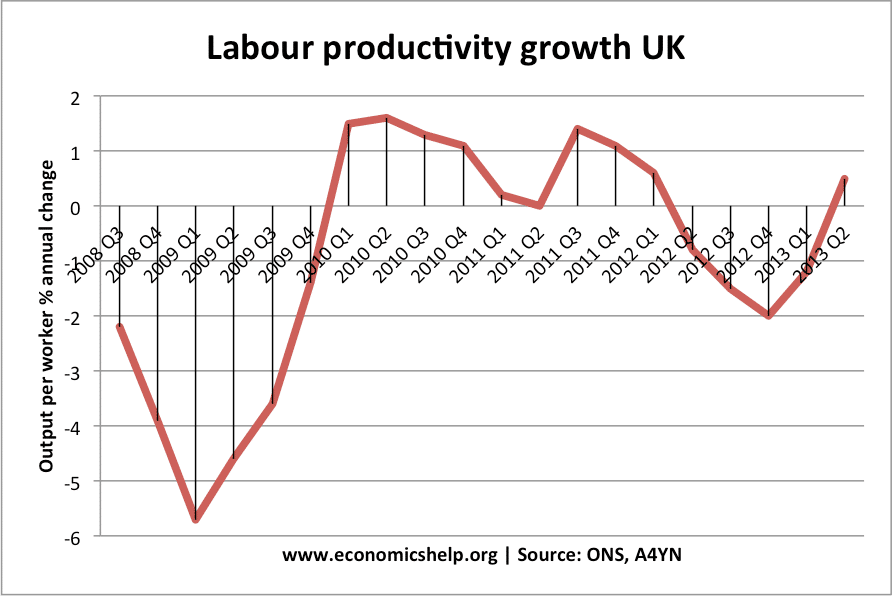

In 2013, there has been growth in consumer spending, but this has come despite slow growth in real wages. A feature of the prolonged recession has been very low / zero nominal wage growth. This means, combined with inflation above the government’s target, many consumers have seen a prolonged fall in real wages. With stagnant real wages, there is a limit to how much consumer spending can lift the UK economy. A sustained recovery will need a return to real wage growth. This may come if inflation falls and firms feel more profitable and able to increase wages. Real wage growth will also require a change in the UK’s very poor productivity growth rate over the past five years.

GDP statistics

Firstly, the latest GDP statistics (preliminary from Q3 2013) were promising:

In particular, data from Q3 suggested growth across the main industrial sectors of the economy.

In output Q3 compared to Q2, output increased by 1.4% in agriculture, 0.5% in production, 2.5% in construction, and 0.7% in services. This was a rare sign of a more balanced growth. Future growth figures are also looking more optimistic, with analysts predicting strong growth in the next quarter.

But, we always need to add a disclaimer to be wary of quarterly statistics. Firstly, we have to be careful about inferring too much from quarterly economic statistics (especially provisional figures which could be revised up or down later) If one swallow doesn’t make a summer, one or two positive quarterly growth figure don’t overcome a prolonged economic stagnation.

Growing current account deficit and weak exports

Ironically, one day after asking this question, data on exports and the current account deficit was disappointing – raising concerns that the UK recovery was still fragile and unbalanced.